Associated British Foods plc: The Ultimate Conglomerate Pivot

I. Introduction & Episode Roadmap

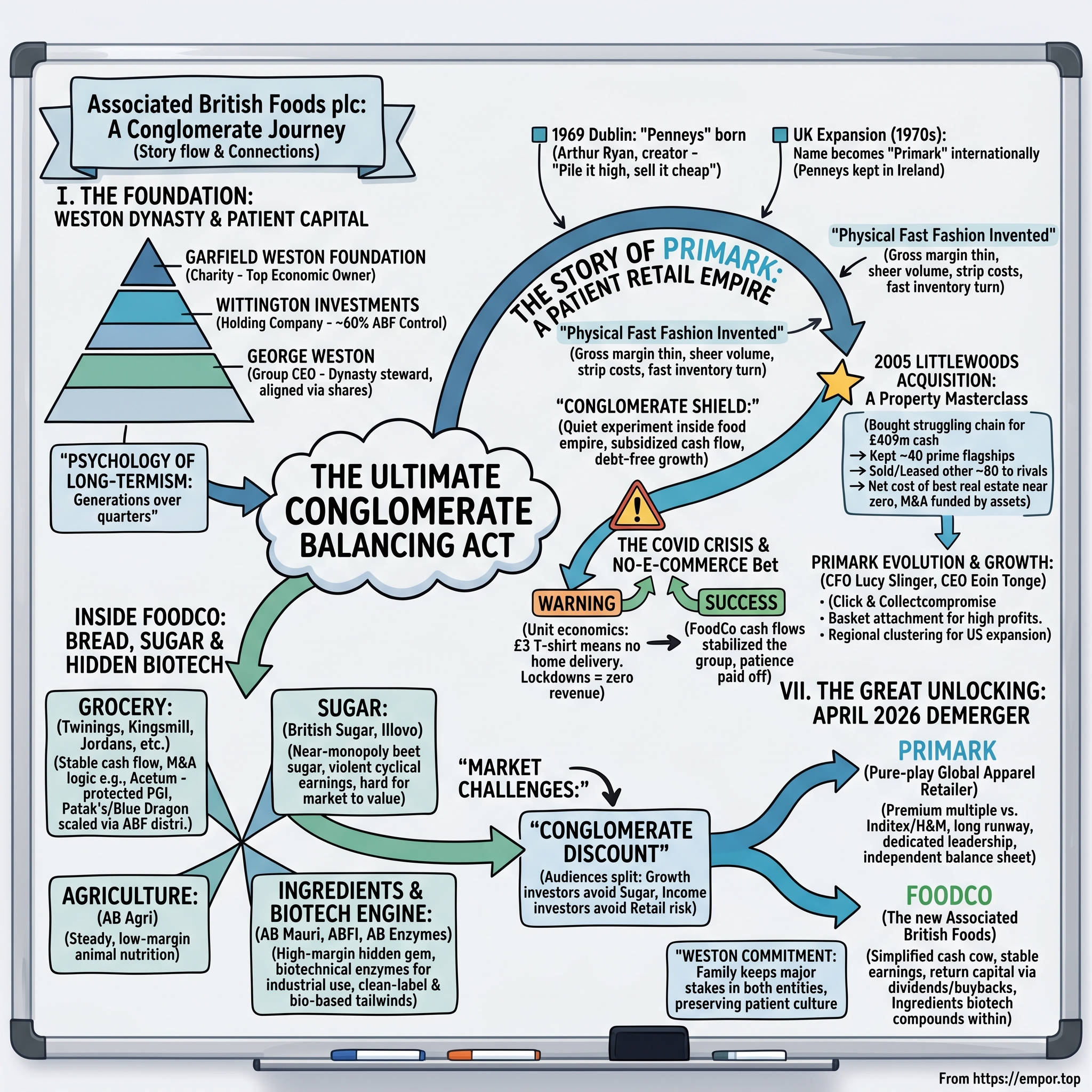

On April 21, 2026, a company that had spent the better part of a century refusing to behave the way the stock market wanted it to finally blinked. Associated British Foods — the sprawling, deliberately unfashionable conglomerate behind your morning loaf of Kingsmill, the sugar in your tea, the actual tea in your tea, and, improbably, one of the most ferocious discount-clothing empires on the planet — announced that it would split itself in two.1

The mechanism was a tax-free dividend demerger of Primark, its fast-fashion juggernaut, from everything else. By the end of 2027, the plan goes, there will be two separate companies listed on the London Stock Exchange, each large enough to sit comfortably in the FTSE 100: one a pure-play global apparel retailer, the other a diversified food, sugar, and industrial-ingredients group that keeps the historic Associated British Foods name.12

To understand why this is genuinely surprising, you have to appreciate what ABF had been for nearly ninety years. This was a company famous — even mocked — for its low profile. A bread-and-sugar dynasty run by an Anglo-Canadian family that almost never gave interviews, almost never chased acquisitions for headlines, and almost never did what bankers told it to. And yet, tucked inside that boring milling-and-baking machine, it had quietly built and financed a physical-only retail phenomenon that today rivals Inditex's Zara and H&M for the affection of value-hungry shoppers across Europe and, increasingly, the United States.

That is the paradox at the center of this story. How did a conservative, charity-controlled food conglomerate become the patient capital behind one of the most aggressive, debt-light, store-only fashion empires in history? And having pulled that off, why break it apart now?

Here is the roadmap. We will start with the Weston family and the extraordinary ownership structure that made all of this possible — a charitable foundation sitting atop a holding company sitting atop a FTSE 100 giant, an arrangement engineered to ignore the tyranny of the quarterly earnings call. We will tell the origin story of Primark, born as "Penneys" in 1969 Dublin under a retail savant named Arthur Ryan. We will dissect the single greatest piece of real-estate financial engineering in modern British retail — the 2005 Littlewoods acquisition. We will confront the company's most counterintuitive bet: its near-total refusal to sell clothes online, a stance that nearly killed it during the pandemic and yet remains central to its economics. We will go inside "FoodCo" — the grocery brands, the cyclical sugar operation, and the genuinely fascinating high-margin biotechnology business hiding in the ingredients division. And finally, we will analyze the demerger itself: the conglomerate discount, the valuation unlock, and what investors should actually watch from here.

Let's begin where every ABF story has to begin — with the family that has never let go.

II. The Weston Dynasty, Wittington, and Modern Management

Picture a corporate org chart drawn upside down. At the very top, where you would normally expect to find restless institutional shareholders demanding buybacks, sits instead a grant-giving charity that hands money to hospices, schools, and community projects across Britain. That charity is the Garfield Weston Foundation, and it is the quiet, patient gravity well around which the entire ABF universe orbits.

The structure works like this. A private holding company called Wittington Investments Limited controls 60.19% of Associated British Foods.2 Wittington itself is 79.2% owned by the Garfield Weston Foundation and 20.8% owned by members of the Weston family.2 So the dominant economic owner of one of the FTSE 100's largest companies is, in effect, a charitable foundation — and the family's role is partly to steward that charity's endowment.

Stop and consider what this does to the psychology of the business. A normal public company lives and dies by the next set of quarterly numbers; a disappointing three months can torch a CEO's tenure. ABF's controlling owner, by contrast, has a time horizon measured in generations and a mandate to fund good works in perpetuity. That removes an enormous amount of short-term pressure. It is precisely the kind of ownership that allows management to spend two or three decades patiently scaling a retail concept that is barely profitable at first — because nobody at the top is panicking about this year's earnings per share. Patience, here, is not a personality trait. It is a structural feature, baked into the cap table.

The man running the whole thing is George Weston, Group Chief Executive since April 2005.3 He is, by the standards of celebrity retail bosses, almost aggressively unglamorous — low-key, financially disciplined, allergic to hype. He is a fourth-generation member of the dynasty, and he treats the company less like a personal trophy than like a family trust he is obligated not to break.

And his alignment with shareholders is not theoretical. George Weston directly owns 3.95 million ABF shares, around 0.56% of the company — a stake worth on the order of £100 million.2 On top of that, he is a beneficiary of the G H Weston 1964 Settlement, a family trust that holds a further 15.57 million shares, roughly 2.22% of ABF.2 Add it up and the man's personal and family economic interest in the company runs toward half a billion pounds. When George Weston makes a capital-allocation decision, he is, in a very literal sense, deciding what happens to a meaningful slice of his own family's wealth.

The formal governance reinforces this. ABF requires its CEO to hold shares worth at least 300% of base salary — a "skin in the game" rule that, for Weston, is almost comically redundant given he clears it by orders of magnitude.2 His pay is heavily performance-linked rather than guaranteed: for FY24/25 his total remuneration came to £6.05 million.2 The structure underneath that number tells you what the company actually cares about. The Short-Term Incentive Plan can pay up to 200% of base salary, but half of any bonus is deferred into shares for three years.2 The Restricted Share Plan can grant up to another 200% of salary in shares, with a three-year performance window followed by a further two-year holding period — and crucially, it is tied to Return on Capital Employed and adjusted earnings-per-share growth.2 In other words, the people running ABF get paid for deploying capital well and growing real profits, not for chasing revenue or goosing the share price for a quarter.

That philosophy now has to survive a once-in-a-generation reorganization, and a new bench of executives has been assembled to deliver it. Joana Edwards was appointed permanent Group CFO of ABF in March 2026, having served a year as interim CFO after stepping up from Group Financial Controller.4 She is a L'Oréal veteran, and she brings exactly the kind of institutional financial rigor a cash-rich food business heading into a complex split will need.4

On the retail side, Eoin Tonge — a former ABF Finance Director — took over as interim Primark CEO in March 2025 and was confirmed as permanent CEO in March 2026, anchoring the business that is about to be spun out.[^5] And in June 2026, Primark hired Lucy Slinger as its standalone CFO, poaching her from IKEA's parent, the Ingka Group.[^6] Her job is to give Primark its own financial spine — the systems, controls, and treasury function a newly independent global retailer requires — and to help shepherd it through both the demerger and its international expansion.[^6]

The throughline across all of these appointments is continuity of philosophy. The names are changing; the patient, capital-disciplined, family-anchored operating culture is not. To understand why that culture matters so much, we have to go back to a discount shop in Dublin and a man who arguably invented the entire category.

III. The Story of Primark: Arthur Ryan and the Penneys Experiment

Dublin, 1969. The Irish economy is modest, incomes are tight, and the idea of disposable, of-the-moment fashion for ordinary people barely exists. Into this setting steps Arthur Ryan, hired by Galen Weston — George's father — to open a discount apparel shop. The store opens under the name Penneys, and it will, over the next half-century, rewrite the rules of how clothing is sold.5

Ryan is the kind of figure business history loves: the operator-genius who builds something enormous while remaining almost completely unknown to the public. He is frequently described as the man who invented physical fast fashion, and the model he developed was startlingly simple to state and brutally hard to execute. Pile it high, sell it cheap. Run on gross margins so thin they would terrify a conventional retailer, and make the money back on sheer volume. Strip out everything that adds cost without adding sales — fancy fixtures, attentive in-store service, elaborate marketing. Turn inventory over fast enough that the shelves always feel fresh and the cash keeps cycling.

The genius of the format was that it inverted the usual luxury logic of retail. Most fashion businesses try to make you feel special so they can charge you more. Penneys made you feel like you were getting away with something — racks of genuinely cheap, genuinely current clothes you could buy on impulse without guilt. The store did not need to persuade you to spend a lot; it needed to persuade enormous numbers of people to spend a little, very often. That is a volume game, and volume games are won on operational discipline, not glamour.

There was an early hiccup that turned out to be a permanent feature. When the chain began expanding to the UK mainland in the early-to-mid 1970s, it ran into the American retail giant J.C. Penney, which blocked the use of the "Penneys" name outside Ireland. Ryan simply rebranded the international stores as Primark, while keeping the beloved Penneys banner exclusive to the Republic of Ireland — where, to this day, the same shops trade under the old name. It is a small detail, but a revealing one: the company was willing to carry two brand names for the same business rather than fight an expensive trademark war or abandon a name customers loved.

Here is the part that is easy to miss. For roughly the first three decades of its life, Primark was not a headline business. It was a quiet, cash-generating experiment tucked inside ABF's vast and unglamorous empire of flour mills, bakeries, and sugar plants. The steady, defensive cash flows of the food operations effectively subsidized Primark's slow, methodical, debt-free expansion of its physical store estate. While other retailers borrowed heavily or sold equity to grow, Primark could grow on the food group's reliable internal cash — opening stores when the locations were right, not when a financing window happened to be open.

That conglomerate shield is the unglamorous secret behind Primark's eventual dominance. A standalone fast-fashion start-up would have faced relentless pressure to either turn a quick profit or raise outside money on dilutive terms. Primark faced neither. It got to compound patiently, under cover, for thirty years. And when it finally stepped into the open, it did so with a balance sheet and an operating model that competitors funded by impatient capital simply could not match. The moment it truly announced itself came in 2005, with a deal that retail strategists still study — and it is where we turn next.

IV. The Property Masterclass: The Littlewoods Acquisition and European Scaling

In the summer of 2005, the British high street was littered with the wreckage of failing department stores — tired chains sitting on irreplaceable real estate they no longer knew how to use. The most valuable thing in retail is not a brand or an inventory system. It is location: the corner of Oxford Street, the dominant unit on a regional high street, the spot that thousands of people walk past every single day. And in 2005, ABF made a move to acquire a great deal of it at once.

In July 2005, ABF bought the struggling Littlewoods retail chain for £409 million in cash.6 On its face, this looked like a food-and-sugar conglomerate inexplicably wading into a dying department-store business. In reality, it was one of the most elegant pieces of corporate real-estate arbitrage in retail history.

The key insight is that Primark did not want Littlewoods. It did not want the brand, the catalog operation, or the inventory. It wanted the buildings. The Littlewoods estate included a portfolio of prime, high-footfall locations — exactly the kind of large-format, prominent sites a high-volume discount retailer needs and can almost never assemble quickly on the open market because they so rarely come up for sale.

So ABF performed a kind of surgical strip-down. Primark kept only the cream — roughly 40 of the most prominent, prime-location stores, including flagship sites such as London's Oxford Street — to convert into giant Primark outlets. The remaining roughly 80 locations it did not want were aggressively sold or leased out to competitors who were themselves desperate for retail footprint — buyers and tenants including BHS, Next, and Marks & Spencer.

Now do the math, because the math is the whole point. By offloading those 80 surplus leases and sites to rivals hungry for space, ABF recouped a very large portion of its £409 million outlay. The net effect was that the prime flagship stores Primark actually kept came at an effective cost driven down toward zero — and by some readings, given the value extracted, close to negative. ABF had, in essence, gotten the best retail real estate in Britain for almost nothing, with competitors footing much of the bill by paying up for the leftovers.

Contrast this with how the rest of the industry was behaving. Through the same era, peers like Marks & Spencer and the Arcadia Group were taking on expensive long-term leases or overpaying outright for acquisitions to chase the same scarce footprint. ABF did the opposite: it used a disciplined, property-backed, asset-stripping approach to M&A in which the assets themselves financed the deal. The result was that Primark's UK market share and earnings were supercharged almost overnight — it suddenly had the locations to put its high-volume model in front of millions more shoppers, without the balance-sheet damage that would have crippled a less disciplined buyer.

This is the Weston capital-allocation philosophy in its purest form: buy where there is an asset backstop, let the unwanted pieces pay down the purchase price, and keep only the crown jewels at a net cost that flatters returns for decades. It is the same instinct — discipline, downside protection, patience — that runs through every good decision in this story.

Armed with the proven flagship-store playbook, Primark turned to the Continent. It opened in Spain in 2006 and then rolled methodically across Europe — the Netherlands, Germany, France, and Italy followed. The format evolved as it went. Rather than small shops, Primark built enormous "experience" stores, cathedral-sized spaces that turned the act of cheap shopping into a high-density, high-energy destination — drawing both locals and tourists, and generating the foot traffic and sales-per-square-foot the volume model depends on.

But this entire strategy rested on one radical, almost heretical premise: that Primark would sell its clothes only in physical stores, and essentially refuse to ship them to your door. In the 2010s, as the rest of retail stampeded online, that looked increasingly like a fatal flaw. Then came a global pandemic that tested the thesis to absolute destruction.

V. The No-E-commerce Paradox: Covid Lockdowns, Click & Collect, and US Expansion

Start with a question that sounds like a riddle. Why would a major global fashion retailer, in the age of Amazon, deliberately refuse to let you buy its clothes online and have them delivered to your home? The answer is hidden inside the price of a £3 t-shirt.

When a retailer ships a low-priced item to a customer's house, a chain of costs kicks in: picking the item from a warehouse, packing it, paying for delivery, and — most painfully in fashion — processing the returns when it doesn't fit or doesn't suit. For a premium garment with a fat margin, those costs are an annoyance the price can absorb. For a £3 t-shirt sold on razor-thin margins, those same costs simply eat the entire profit and then some. Ship that t-shirt and you lose money on the transaction. Primark's whole model is built on selling enormous volumes of very cheap goods, and home-delivery economics are fundamentally incompatible with very cheap goods. So Primark didn't do it. The "missing" e-commerce business wasn't an oversight or a failure of nerve — it was a clear-eyed reading of unit economics.

Then 2020 arrived and turned that principled stance into a near-death experience. The COVID-19 pandemic and the lockdowns that followed did something to Primark that they did to almost no other major retailer. With every store physically closed and no online storefront to fall back on, Primark's sales did not merely fall — they went to zero. Monthly revenues that had been running at well over £650 million dropped to literally nothing during the worst of the closures. There was no digital channel to catch the demand. The stores were the entire business, and the stores were shut.

This is the precise moment the conglomerate structure earned its keep — the payoff for all those decades of the food business quietly subsidizing the retailer. While Primark was burning cash with no revenue at all, ABF's Grocery, Sugar, and Ingredients divisions were having a banner period. With the world locked indoors and eating at home, demand for staple foods, baking ingredients, and grocery brands surged. Those divisions threw off the cash that stabilized the entire group and carried Primark through a stretch that would have bankrupted a standalone, debt-financed fast-fashion company. The much-derided diversification — the bread-and-sugar ballast that pure-play investors complained about for years — was the only reason Primark could afford to have no online sales during a year when stores were illegal to open.

The crisis did, however, force a rethink — not an abandonment of the model, but a clever compromise with it. Under Eoin Tonge's leadership, Primark designed a digital channel that preserved its core economics instead of destroying them. Trialed in late 2022 and scaled through 2024 to 2026, the answer was Click & Collect. Customers can browse and order a defined range online — initially children's clothing and home goods — but they cannot have it delivered. They must physically come into the store to pick it up.

At first glance this seems almost stubborn — why make customers do the work? The genius is in what Primark's data revealed about behavior. The "secret sauce" is basket attachment: when click-and-collect customers walk into the store to grab their pre-ordered items, they keep shopping. They pass the racks, they pick up extras, they leave with more than they came for. The online order becomes a foot-traffic generator rather than a margin destroyer. Primark gets the convenience and discovery benefits of digital while keeping the highly profitable physical-basket economics fully intact. It is the e-commerce of a company that understands exactly why it never wanted conventional e-commerce in the first place.

The other great growth frontier is the United States, and here too the approach has been characteristically patient. Primark entered the US in Boston in 2015. Rather than splashing out on expensive national advertising to announce itself coast to coast — the obvious but capital-burning move — it chose to grow organically in regional clusters, concentrated in the Northeast and Mid-Atlantic, and to build localized supply hubs to serve those clusters efficiently. The logic is density: cluster stores tightly enough and you get supply-chain efficiency, brand awareness through sheer physical presence, and word-of-mouth without paying for prime-time TV. The target has been to build past 60 stores, and after years of careful seeding, the US has finally become a material, profitable, and genuinely scalable growth vector for the business — the engine that a standalone Primark will be expected to run hard.

For all the drama of Primark, though, the other half of ABF is a quietly remarkable collection of businesses in its own right — and one of them is a hidden high-margin compounder that almost nobody talks about. To value the demerger, you have to understand FoodCo.

VI. Inside FoodCo: Grocery, Sugar, Agriculture, and the Ingredients Biotech Engine

Walk through a British supermarket and you are, without realizing it, walking through ABF. The Twinings tea, the Ovaltine, the Patak's curry paste, the Blue Dragon stir-fry sauce, the Jordans and Dorset Cereals, the Ryvita crispbread, the Kingsmill bread from Allied Bakeries — all of it sits under the food half of the company.7 Collectively, the food operations represent something on the order of £10 billion in revenue and a base of stable operating cash flow. But that headline lumps together four very different businesses, and the differences are what matter.

Start with Grocery, the largest contributor to segmented food profit at roughly a quarter of the total. This is a portfolio of high-moat, leading consumer brands — names that have earned shelf space and customer loyalty over decades.7 What makes the grocery story interesting for our purposes is not the brands themselves but how ABF has acquired and managed them, because the M&A philosophy here is the same disciplined instinct we saw with Littlewoods, just applied to food.

Consider the 2017 acquisition of Acetum, the leading producer of certified Balsamic Vinegar of Modena PGI. ABF paid €300 million, which worked out to roughly 15 times EBITDA on around €103 million of net sales.[^10] On the surface, 15x EBITDA does not sound cheap. But in premium-food M&A, where defensible branded assets routinely fetched 18 to 20 times EBITDA, paying 15x was actually disciplined — and what ABF bought for that multiple was extraordinary. "Balsamic Vinegar of Modena" is a Protected Geographical Indication: by law, authentic product can only be made in Modena, Italy.[^10] That is a geographical monopoly enforced by regulation — a moat that no competitor can dig around by building a cheaper factory elsewhere. ABF paid a below-market multiple for a business with above-market protection. That is the whole game.

The same playbook appears in the 2007 purchase of Patak's, the Indian-food brand, for an estimated £100 million to £125 million on around £66 million of revenue.[^11] ABF folded Patak's together with Blue Dragon to create AB World Foods, then used its enormous global retail distribution muscle to scale the brand into markets it could never have reached on its own.[^11] The pattern is consistent: buy a strong brand at a sensible price, then pour it through the distribution pipes ABF already owns. Acquisitions as leverage on existing infrastructure, not as standalone bets.

Then there is Sugar, and Sugar is a different animal entirely — the cyclical, commodity-exposed part of the empire. British Sugar holds a near-monopoly on UK beet sugar production, complemented by Illovo Sugar's operations across Africa. The problem is that sugar earnings swing violently with crop yields and commodity prices. The segment contributed £199 million in profit in FY24 — and then fell into an operating loss in FY25 as European beet sugar prices collapsed.72 That kind of whiplash, from a healthy nine-figure profit to a loss in a single year, is exactly the sort of thing public-market investors hate. It also helps explain the conglomerate discount we will come to shortly: a stable retailer bolted to a volatile commodity producer is genuinely hard to value as one number.

Agriculture is the smallest piece, at around 2% of profits. AB Agri is a low-margin but steady animal-nutrition and feed business — unglamorous, reliable, and not where the value story lives.

Which brings us to the hidden gem, the part of this company that genuinely deserves more attention than it gets: Ingredients, at roughly 12% of profits. This division has two halves. One is AB Mauri, the world's largest yeast producer — itself a formidable, globally scaled business. The other is ABF Ingredients (ABFI), and inside ABFI sits the most interesting technology story in the entire company: AB Enzymes.8

Let's slow down and explain what this actually is, because "industrial enzymes" sounds like something you can safely skim past, and you shouldn't. Enzymes are biological catalysts — molecular machines that speed up chemical reactions. AB Enzymes manufactures them at industrial scale for uses across biorefining, baking, and animal feed.[^13] Think of an enzyme as a tiny, reusable tool that makes an industrial process more efficient: an enzyme added to animal feed helps livestock extract more nutrition from the same grain; an enzyme in baking improves dough handling and shelf life; an enzyme in biorefining helps convert raw plant material into fuels or chemicals. These are high-value, highly technical products, sold to industrial customers who depend on them and don't switch suppliers casually. It is, in plain terms, a biotechnology business hiding inside an agricultural conglomerate.

And it performs like one. The specialty ingredients division generated £257 million in profit in FY25 at a 12.6% operating margin — a markedly higher margin than bread or sugar will ever produce, and the kind of figure that signals real pricing power and technical differentiation.2 Better still, it sits in front of powerful secular tailwinds: the clean-label movement in food, the shift toward bio-based alternatives to petrochemicals, and pharmaceutical applications through businesses like SPI Pharma and Ohly, which supply excipients and specialty ingredients to drugmakers.8 Quietly, this is a high-margin compounding machine — real optionality and a premium asset that the market has long struggled to see, because it has been buried beneath a legacy footprint of flour and beet. When investors size up the future "FoodCo," this is the piece most likely to be undervalued by habit.

So now we have the full picture: a patient family owner, a retail jewel, a property masterstroke, a contrarian no-e-commerce model, and a food business that ranges from cyclical sugar to a hidden biotech compounder. The obvious question is the one the market kept asking for years — why hold all of this together at all? In April 2026, ABF finally answered.

VII. The Great Unlocking: The April 2026 Demerger and Strategic Rationale

For decades, George Weston and the ABF board did something that took real conviction: they defended the conglomerate model against a steady drumbeat of skepticism. The bread-and-sugar ballast had saved Primark in 2020. The diversified cash flows funded patient expansion. Why on earth would you break up a structure that worked?

And then, on April 21, 2026, they announced they would do exactly that.1 To understand the reversal, you have to understand the specific market pathology the structure had created — the conglomerate discount.

The conglomerate discount is what happens when the stock market values a collection of businesses for less than those businesses would be worth apart. ABF was a textbook case, and the reason was a mismatch of investor audiences. The kind of investor who wanted to own a high-growth global fashion retailer — someone happy to pay a premium multiple for Primark's expansion runway — did not want to also own exposure to volatile European beet-sugar prices and slow-growing bread mills. Conversely, the conservative income investor who loved the idea of a defensive, dividend-paying staple-food giant did not want the fashion-trend risk and execution intensity of a massive global apparel chain bolted onto it. Each investor was being asked to swallow something they didn't want in order to own the part they did. So both groups discounted the whole. Neither pure-play crowd would pay full price, and the combined entity traded below the sum of its parts.

The demerger is the surgical fix for that mismatch. The mechanics are deliberately clean. The transaction will be structured as a tax-free dividend demerger, expected to complete by late 2027.12 Existing ABF shareholders will not have to do anything or sell anything; they will simply receive shares in both resulting companies, holding the same underlying assets but now in two separately listed packages.1

The two companies are designed to appeal to those two different audiences directly. FoodCo will keep the Associated British Foods plc name and retain the stable, cash-generative Grocery, Sugar, and Ingredients businesses.1 Its job is to be a cash cow — simplifying its story, returning capital to shareholders through high dividends and buybacks, and letting that high-margin ingredients biotech division compound quietly within a clearer structure. It is built for the income-and-quality investor.

Primark, meanwhile, will list as a pure-play, high-growth global apparel retailer.1 Freed from the conglomerate, the theory goes, it can finally be valued the way the market values its closest comparables — the likes of Inditex's Zara and H&M — and command the premium multiple appropriate to a focused retailer with a long expansion runway in the US and Europe. It also gets its own balance sheet and its own dedicated leadership and finance function — recall Eoin Tonge and Lucy Slinger — to pursue that growth without competing for capital against sugar factories.

There is one more feature that is essential to the whole design, and it is pure Weston. Wittington Investments — the family's holding vehicle — has committed to keeping its roughly 60% majority stake in both resulting companies.1 This is the backstop that should reassure long-term shareholders. The split is not the family cashing out or losing interest; it is a structural reorganization that leaves the same patient, disciplined, multi-decade ownership in control of both entities. The governance culture that built Primark inside a food conglomerate will continue to govern Primark outside of it — and FoodCo too.

So the demerger is, in a sense, the Weston philosophy applied to itself: a disciplined, downside-protected restructuring designed to unlock value that the market structure had been hiding, without surrendering control. Whether it works depends on the underlying competitive strength of each business — which is exactly what a strategic framework can help us pressure-test.

VIII. Strategic Analysis: Hamilton's 7 Powers and Porter's Five Forces

If you want to know whether Primark can thrive as a standalone company, the question is really about durable competitive advantage — the structural reasons it can keep earning attractive returns even as rivals attack. Two frameworks help organize the answer: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Let's war-game Primark through both.

Start with the 7 Powers, which catalog the specific, persistent advantages a business can hold. Primark's strongest is Scale Economies, and it is genuinely formidable. Because Primark sells such immense physical volume, it can buy fabric and commission garment manufacturing in quantities that smaller and mid-tier rivals simply cannot match. Bulk purchasing on that scale drives per-unit costs down to a level competitors can't reach — and because the entire business model is "sell cheap in huge volume," that cost advantage flows straight into the value proposition customers feel at the till. Low prices attract volume; volume drives down costs; lower costs fund even lower prices. It is a flywheel, and it spins faster the bigger Primark gets.

Next is Process Power — the hard-won operational know-how accumulated over decades of running no-frills stores. This is the Arthur Ryan inheritance, refined for fifty years. Simple, low-cost store fit-outs. Extraordinary stock density per square foot. A near-total absence of expensive national television or print advertising, with marketing instead riding on social media and organic word-of-mouth. None of these is a single trick a rival can copy overnight; collectively they represent an embedded operating system that is genuinely hard to replicate, because it lives in thousands of small routines and decisions rather than in any one patentable thing.

Third, and most subtle, is Counter-Positioning — and this is where the no-e-commerce stance earns its strategic stripes. By refusing home-delivery e-commerce, Primark deliberately avoids the fulfillment and returns costs that erode competitors' margins on low-priced goods. The clever part is that incumbents who have built their identity and infrastructure around online delivery cannot easily abandon it to match Primark; their business model and customer expectations are already committed in the other direction. Meanwhile, online-only players cannot beat Primark's in-store prices on basics, because they carry the very fulfillment costs Primark refuses to bear. Primark has positioned itself precisely where its rivals' strengths become liabilities. It is moderate-to-strong as a power — not absolute, because shopping habits shift — but real.

Now flip to Porter's Five Forces, which assesses the structural attractiveness of Primark's competitive environment.

Begin with the Threat of New Entrants, which is genuinely two-sided. Digitally, the threat is high: ultra-fast-fashion disruptors like 希音 Shein and Temu have shown that you can build a vast clothing business with no stores at all, attacking from a direction Primark deliberately doesn't defend. But on the physical side, the threat is much lower. Assembling a global network of enormous, prime-location physical stores is staggeringly expensive and slow — exactly the barrier the Littlewoods playbook was built to overcome. Nobody is going to replicate Primark's store estate from a standing start; the real-estate moat is decades deep.

Consider the Bargaining Power of Suppliers, which for Primark is low — and that's good for Primark. Its sheer scale makes it a must-have customer for global textile factories. When you represent a huge share of a manufacturer's order book, you hold the leverage on price and terms. Suppliers need Primark more than Primark needs any single supplier, which keeps input costs in check.

Finally, the Intensity of Competitive Rivalry, which is unambiguously high. The global apparel market is brutal and crowded. Primark must contend with Inditex's legendary speed-to-market, H&M's vast global footprint, and the digital ultra-fast-fashion insurgents capturing younger shoppers' attention and wallets. This is not a sleepy category where a strong player can coast. Primark's powers are real, but they are deployed in a knife-fight of a market — which is precisely why the demerger's promise of a focused, well-capitalized, independently run Primark matters. Focus is a weapon in a fight this intense.

Frameworks tell you where the advantages and the threats sit. The harder question for an investor is how to weigh them — and what, concretely, to watch.

IX. The Playbook: Investing Lessons, KPIs, and the Bull vs. Bear Case

Step back from the details and the ABF story yields a couple of investing lessons that travel well beyond bread and discount jeans.

The first is patience as a structural moat. The single most underappreciated reason Primark exists is that its owner never needed it to prove itself on a quarterly schedule. The charitable-foundation-and-family ownership structure shielded the company from the short-term market hysteria that forces most managements to abandon long-gestating bets before they pay off. ABF could scale Primark for decades, through periods when it was barely profitable, because nobody at the top was being judged on this year's number. The lesson is not "be patient" as a platitude; it is that ownership structure can be a competitive advantage in its own right, because it changes what management is allowed to do.

The second is the discipline of the asset-backed acquisition — the Littlewoods principle. When you buy, look for a deal where real estate or other hard assets can be sold or recycled to recoup much of your purchase price, leaving you holding the genuinely strategic pieces at a net cost near zero. The same instinct shows up in paying 15x for a regulatory monopoly in balsamic vinegar rather than 20x for an unprotected brand. Across retail and food alike, ABF's edge was rarely about being clever on growth and almost always about being disciplined on price and downside.

So what should an investor actually track from here? Resist the temptation to monitor everything; zero in on the few metrics that genuinely reveal whether the thesis is working. Three stand out.

First, Like-for-Like sales growth at Primark. This strips out the effect of simply opening new stores and tells you whether existing stores are pulling more customers and spend over time. It is the truest test of whether the physical-only model still has pull — and it matters most in the US, where the expansion thesis lives or dies on whether new-market stores mature into productive, busy ones rather than quiet ones.

Second, Primark's retail operating margin, with a sensible reference range of roughly 10–12%. Because the entire model runs on thin margins and high volume, profitability is acutely sensitive to input-cost inflation, labor costs, and how aggressively the business has to mark down unsold stock. Watching the margin tells you whether Primark is holding its cost discipline as it grows, or whether growth is coming at the expense of the economics that make it work.

Third, Return on Capital Employed at FoodCo. ROCE is the cleanest measure of whether George Weston's successors are still allocating capital well — whether reinvestment into high-barrier food brands and the high-margin ingredients biotech business keeps generating double-digit returns, or whether the standalone food company drifts into mediocre, value-destroying spending. ROCE is, after all, the metric the company chose to tie its own executives' pay to; investors might as well watch the same scoreboard.

Now the balanced cases — because a thoughtful investor holds both in mind at once.

The bull case runs like this. The demerger does exactly what it is designed to do: it unlocks a premium valuation for Primark by letting it be priced as the focused global retailer it actually is, alongside Inditex and H&M, rather than as an awkward appendage to a sugar business. Freed from conglomerate drag and equipped with its own balance sheet and dedicated leadership, Primark scales aggressively across the US and Europe, with Like-for-Like growth and margins both holding up. Meanwhile, FoodCo simplifies into a highly profitable, cash-generative staple-food giant that returns large amounts of capital to shareholders through dividends and buybacks, while the high-margin ABF Ingredients division compounds quietly with its clean-label, bio-alternative, and pharmaceutical tailwinds. Two clean stories, two appropriate valuations, the same disciplined family at the helm of both.

The bear case is the mirror image, and it is not trivial. Without the cash-flow buffer of the food divisions, a standalone Primark is fully exposed to the consumer-retail cycle — the very exposure that took its revenue to zero in 2020, now with no diversified parent to absorb the shock. Rising geopolitical tensions could disrupt the Asian supply chains the low-cost model depends on, squeezing the margins that are already thin by design. And the digital ultra-fast-fashion players — Shein, Temu, and whatever comes next — could continue capturing younger demographics, slowly eroding the customer base of a store-only retailer that has chosen, deliberately, not to fight on their turf. On the other side, FoodCo, stripped of its glamorous growth engine, could be left as a slow-growth entity at the mercy of volatile agricultural commodities and the kind of European sugar-price collapse that turned a £199 million profit into a loss in a single year.27

Both cases are live. The demerger does not resolve the tension between them; it simply lets the market price each business on its own terms, for better and worse. Which is, in the end, the entire point.

X. Epilogue

The story of Associated British Foods is, at its core, a study in the power of doing things slowly and deliberately in a world that rewards speed and noise. A family that controlled a charitable foundation that controlled a holding company that controlled a FTSE 100 giant — and used that insulation not for comfort but for conviction. Decentralized management that let a discount-clothing genius in Dublin build something extraordinary inside a flour-and-sugar empire. Capital allocation so disciplined that the company's defining retail expansion was financed in part by selling unwanted real estate back to its own competitors.

For nearly ninety years, ABF defied the conventional wisdom that conglomerates are messy and that physical retail is dying and that you cannot run a serious fashion business without selling online. It was right often enough, and for long enough, to become one of the most singular companies on the London Stock Exchange.

Now that long, unusual run as a hybrid is ending. As ABF embarks on its historic demerger, it closes one of the LSE's most distinctive conglomerate chapters and opens two new ones: a focused global retailer finally free to be valued on its own merits, and a streamlined food-and-ingredients group with a hidden biotech compounder at its heart. The family that never let go is, characteristically, holding on to both. What changes is that the market will finally get to see each business clearly — and decide for itself what patience was worth.

References

-

Demerger of Primark — LSE Regulatory News Service / Associated British Foods, 2026-04-21 ↩↩↩↩↩↩↩↩

-

Annual Report and Accounts 2025 — Associated British Foods plc ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Appointment of Joana Edwards as Group CFO — LSE Regulatory News Service / Associated British Foods, 2026 ↩↩

-

ABF to Demerge Primark after Decades of Conglomerate Structure — Bloomberg, 2026-04-21 ↩

-

ABF buys Littlewoods stores for £409m — The Irish Times, 2005 ↩

-

Annual Report and Accounts 2024 — Associated British Foods plc ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube