Amrutanjan Health Care: The Yellow Balm's Second Act

I. Introduction & The "Yellow Jar" Icon

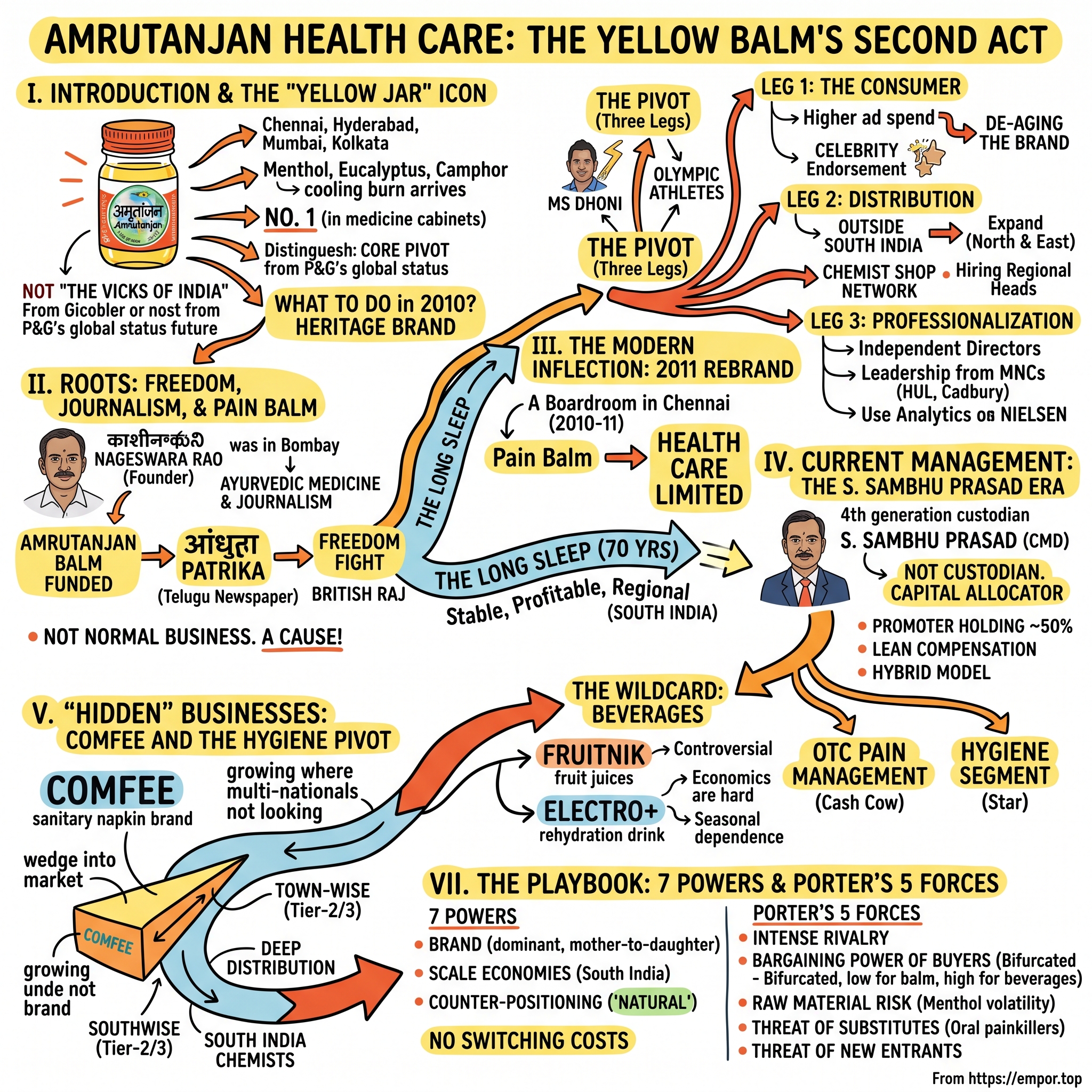

Open any medicine cabinet in any Indian household — Chennai, Hyderabad, Mumbai, Kolkata — and there is roughly a one-in-three chance you will find it. A small, rounded glass bottle. A label the colour of turmeric, bordered in red. A paste the consistency of stiff ointment, smelling powerfully of menthol, eucalyptus, and camphor. Pop the cap, dab a fingertip's worth onto a temple, and within seconds the cooling burn arrives — that strange, almost confusingly satisfying sensation of pain being chased out by a stronger, friendlier intruder.

This is अमृतांजन Amrutanjan. Literally, "the nectar that anoints." In market parlance, the Yellow Balm. And it has been in those medicine cabinets, in some recognisable form, for one hundred and thirty-three years.[^4]

The lazy framing, the one used by half the financial press, is "the Vicks of India." It is technically accurate and almost completely useless. Vicks VapoRub is owned by प्रॉक्टर एंड गैम्बल Procter & Gamble — a hundred-and-eighty-billion-dollar consumer goods leviathan for which India is one market among many. Amrutanjan is a single-listed Chennai-based company with a market capitalisation that, on most days, fits comfortably inside the rounding error of P&G's quarterly cash flow statement. To compare them as products is fair. To compare them as businesses is to miss the entire story.

Because the actual story of Amrutanjan Health Care Limited is not really a story about pain balm. The pain balm is the thing the company is famous for. The pain balm is also, increasingly, the boring part. The interesting part is what a 130-year-old single-product heritage brand chose to do when it looked in the mirror around 2010 and realised that the world it was built for — the world of dusty wholesale markets, regional loyalties, and trade-push economics — was being quietly dismantled around it by Hindustan Unilever, ITC, and Dabur.

The interesting part is the pivot.

The pivot has three legs. First, in 2011, the company surgically removed the words "Pain Balm" from its corporate name and re-baptised itself "Amrutanjan Health Care Limited" — a small change in stationery, a colossal change in self-conception.[^6] Second, beginning quietly that same decade, it walked into one of the most fortified citadels in Indian FMCG — the women's sanitary napkin market, dominated by Johnson & Johnson's Stayfree and Procter & Gamble's Whisper — under a brand called Comfee, and started taking share where the multinationals were not looking.2 Third, it bet on beverages, launching Fruitnik fruit juices and, later, the Electro+ rehydration line — a category adjacency that is either visionary or a mild act of corporate self-harm, and which we will spend some time on.7

Stitching all of this together is a man most equity investors outside India have never heard of: एस. శంభు प्रसाद S. Sambhu Prasad — chairman, managing director, fourth-generation custodian of the family business, and the architect of what is best described not as a turnaround (the company was never broken) but as a re-staging. Taking a profitable, sleepy, regionally-loved cash cow and turning it into something that, on its better days, looks like a modern, multi-category Indian FMCG platform.

This episode walks through that re-staging. We start in 1893 in Bombay, with a Telugu newspaper editor and freedom fighter who sold balm partly to fund the printing presses that fought the British Raj. We move through nearly a century of comfortable regional dominance — Amrutanjan's "sleeping giant" era, when the brand sold itself and management's job was, charitably, custodianship. We arrive at the 2011 inflection point, walk through the Comfee insurgency, the Fruitnik experiment, the capital allocation philosophy, and the unit economics. And we end where every Acquired episode ends — bull case, bear case, the powers framework, and a sober look at what an investor actually owns when they own a slice of a yellow jar that has outlived three currencies, two world wars, one independence movement, and the entire arc of modern Indian capitalism.

Let us begin where the bottle began.

II. Roots: Freedom, Journalism, and Pain Balm

In the late nineteenth century, Bombay was the closest thing British India had to a global city — a port stitched to the world by cotton, opium, and the steamships of the Peninsular and Oriental line. It was also, less obviously, the place where a generation of Indian intellectuals first came face to face with the idea that the Raj might not last forever. Among them was a young Telugu man, born in 1867 in the village of Elakurru in coastal Andhra, who had come to Bombay to make a living in the only profession that would have him: Ayurvedic medicine and journalism.

His name was కాశీనాథుని నాగేశ్వరరావు Kasinathuni Nageswara Rao. To Telugu readers of a certain age, he is "Desoddharaka" — uplifter of the nation — a title bestowed not by the British but by his own people for what he did with the next four decades of his life.[^4] To students of Indian business history, he is something rarer: a founder whose commercial enterprise and political conviction were not adjacent activities but the same activity, funded by the same balm.

The balm came first, narrowly. In 1893, working out of a small premises in Bombay, Nageswara Rao formulated and began selling a topical analgesic compounded from menthol, camphor, eucalyptus oil, and a handful of other aromatic ingredients — a recipe that drew on the ఆయుర్వేదం Ayurveda tradition he had grown up around but presented in the modern, branded, glass-bottled format that the British and American patent medicines were popularising across the empire.[^4] He called it Amrutanjan — from अमृत amrita, the Sanskrit word for the nectar of immortality, and अंजन anjana, the kohl-like paste applied to the eyes in classical medicine. The name was unsubtle. It promised divinity in a jar.

What it actually delivered was effective relief from the headaches, body aches, and respiratory congestion that, in the absence of accessible modern pharmaceuticals, were the dominant forms of suffering in Indian households. The product worked, the price was reasonable, and the branding — that distinctive yellow label — became, over the course of two decades, recognisable from Karachi to Madras.6

Here is where the story diverges from the standard "founder builds business" narrative. Because Nageswara Rao did not, in any meaningful sense, want to be a balm magnate. He wanted to be a journalist and a freedom fighter, and the balm was the thing that paid for both. In 1908, he founded the Telugu-language weekly ఆంధ్ర పత్రిక Andhra Patrika — which would later become a daily — and within a few years had moved its operations and his own residence to Madras (today's Chennai). The newspaper became one of the most influential vernacular publications of the independence era, serving as a platform for the Indian National Congress, for figures like Bal Gangadhar Tilak and Mahatma Gandhi, and for the broader भारतीय स्वतंत्रता आंदोलन Indian Independence Movement.[^4]

The balm funded the paper. The paper made the founder a public figure. The public figure became, in 1924, the elected president of the All India Congress Committee — a position that placed him at the centre of the freedom struggle alongside Gandhi himself. He also founded literary journals, established publishing houses for Telugu literature, and — this is the part that matters for the company's modern self-conception — donated significant portions of his personal wealth to nationalist causes, educational institutions, and famine relief.[^4]

In other words, Amrutanjan is not, in its origin, a normal business. It is a business attached to a cause. Within India, this is part of why the brand commands the loyalty it does — a loyalty that the McKinsey consultants who occasionally circle Indian FMCG cannot fully decode in their PowerPoint decks. When a Tamil or Telugu grandmother reaches for the yellow bottle, she is not just reaching for a balm. She is reaching, sometimes consciously, for a piece of the freedom struggle.

Nageswara Rao died in 1938 — nine years before the country he had spent his life agitating for actually became independent. The balm business passed, in the way of Indian family enterprises, to his successors. And here the company entered what we might charitably call the long sleep.

For nearly seventy years — from independence through the licence raj, through the green revolution, through the early reforms of 1991, and well into the 2000s — Amrutanjan operated as a profitable, stable, regionally-concentrated single-product company. The Yellow Balm was the product. South India was the market. The economics were excellent: a high-margin, low-capex, repeat-purchase consumer good with the kind of brand equity that only compound-interest-on-trust can create. The strategy was, essentially, to not screw it up.6

For a long time, this was a perfectly good strategy. India in the 1970s and 1980s did not reward ambition. The licensing regime, the foreign exchange controls, the limited media reach, and the small organised-retail footprint all conspired to make scale-based aggression unprofitable. A regional cash cow was not a bad thing to be. A regional cash cow was, frankly, the optimal thing to be.

The trouble was that the world that rewarded this strategy began, around the turn of the millennium, to disappear. Cable television, then satellite television, then mobile phones flattened regional information markets. Modern retail — Future Group's Big Bazaar, then DMart, then organised pharmacy chains like Apollo and Medplus — created shelves where national brands could reach Bangalore and Chennai as easily as Delhi. Multinationals like P&G poured marketing dollars into Vicks. And the freedom-struggle aura that had carried Amrutanjan through three generations was, for the urbanising twenty-something with a job in IT services and a Big Bazaar membership, a story their grandmother told.

By the late 2000s, the question facing the company was no longer "how do we protect what we have." It was "if we do nothing, what do we have in twenty years?"

The answer, they realised, was less than they thought. Which is what brought them to 2011.

III. The Modern Inflection: The 2011 Rebrand and Professionalization

Picture the scene. A boardroom in Chennai, sometime in 2010 or early 2011. The man at the head of the table is S. Sambhu Prasad — at the time still consolidating his authority as the operational head of the company that bore his great-grandfather's product. The slide on the screen is unremarkable: a revenue breakdown by geography. North India, single digits. East India, single digits. West India, in the teens. South India, somewhere north of seventy percent.[^6]

Anyone who has ever sat through a strategy review at an Indian consumer company knows the shape of the conversation that follows. The seventy percent number is, at first glance, a triumph — proof of dominance in the home market. On the second glance, it is a warning. Because the demographic and economic gravity of India was shifting, in the 2010s, decisively northward. The fastest-growing consumer markets were Uttar Pradesh, Bihar, Madhya Pradesh, Maharashtra. The fastest-growing modern retail footprints were in Delhi-NCR and the Mumbai metropolitan region. The fastest-growing salaries — and therefore the fastest-growing FMCG wallets — were in cities where Amrutanjan was, candidly, not on the shelf.

The company was a regional brand pretending to be a national one, and the gap between the pretence and the reality was widening every year.

The first move was symbolic. In 2011, Amrutanjan Limited was formally renamed Amrutanjan Health Care Limited.[^6] Three words added, one removed — "Pain Balm" was quietly stripped from the corporate identity. To the casual observer, this was a stationery exercise. To anyone reading it carefully, it was a manifesto. The company was telling its shareholders, its employees, its distributors, and itself: we are no longer in the business of one product. We are in the business of health.

This is the kind of thing that sounds obvious in retrospect and was extraordinarily difficult at the time. Indian family-owned businesses do not lightly walk away from the brand language that built them. The founder's product had been the corporate identity for one hundred and eighteen years. To recede that product into being one product among several required a leadership team willing to bet that the future cash flows of categories that did not yet exist for the company would exceed the symbolic value of what had always existed.

Sambhu Prasad and his team made that bet. And they made it on three fronts simultaneously.

The first front was the consumer. For most of its life, Amrutanjan had been a wholesale-push business — manufacture the product, ship it to a network of distributors, let the distributors push it into the trade, and rely on the brand's recognition to pull it off the shelf. Marketing, where it existed at all, had been generic — small-budget print and radio campaigns, the occasional regional television spot, no celebrity endorsements to speak of. The product, the company believed, sold itself.

The product, the company concluded, no longer entirely did. The 2010s rebrand brought with it a deliberate shift to consumer-pull marketing — significantly higher advertising spend, professional creative agencies, and a campaign of celebrity endorsements that included the Indian cricket captain महेंद्र सिंह धोनी M.S. Dhoni and a series of Olympic athletes whose narratives of physical exertion mapped naturally onto the balm's positioning.3 The strategic intent was straightforward. Generic advertising told existing consumers that Amrutanjan still existed. Celebrity advertising told twenty-five-year-olds, who had never reached for the yellow bottle in their lives, that this was a brand for them too. It was de-aging by association.

The second front was distribution. Breaking out of the South India trap was not a marketing problem; it was a logistics and trade-relations problem. Amrutanjan had, over a century, built dense, deep, loyal distribution networks in Tamil Nadu, Andhra Pradesh, Telangana, Karnataka, and Kerala. In Maharashtra and Gujarat, the network was thinner. In the Hindi-speaking belt — the largest consumer market in the country — it was, in places, almost theoretical.

Building it out required hiring regional sales heads who actually understood the trade dynamics in places like Lucknow and Kanpur, restructuring the depot footprint, expanding the number of direct retail outlets covered (a metric the company began, around this period, to disclose more rigorously to investors), and crucially, not under-spending on trade margins relative to the entrenched local players.1 The work was unglamorous and slow. National distribution in India is built one wholesaler relationship at a time, and the established players — Dabur, Emami, Himalaya — had decades of head start. The company has been at this expansion for over a decade and is still at it. South India remains a disproportionate share of revenue. But the share is no longer seventy. By more recent disclosures, it has come down meaningfully, with North and East India contributing materially in a way they did not in 2010.[^2]

The third front, and the one most relevant for an investor trying to understand the modern company, was professionalization. For most of its history, Amrutanjan had been run as a family enterprise in the strict sense — promoter family at the top, family appointees in key roles, decision-making informed by tradition, intuition, and personal relationships. The 2010s brought in something new: independent directors with consumer goods backgrounds, a leadership team augmented by hires from MNCs like Hindustan Unilever and Cadbury, a more formal management cadence, and the importation of the analytical machinery — Nielsen retail audits, brand health tracking, IRI-style category analytics — that large FMCG companies use to run themselves.[^15]

This is the move that quietly distinguishes Amrutanjan from a lot of its mid-cap Indian peers. The Emami of the 2000s, the Dabur of the 1990s, the Marico of the 2000s — all of these companies went through a similar professionalization arc, and the ones that did it well materially re-rated their valuations and growth trajectories. The bet here is the same: take a family business that operates on instinct and graft onto it the operating discipline of a professional FMCG, while preserving the long-term, capital-cycle-spanning judgment that family ownership uniquely provides.

The benchmarks the company watched, and to some extent still watches, were instructive. The closest Indian peer is एमामी Emami, owner of Zandu Balm — a brand acquired in 2008 that gave Emami a direct entry into the topical pain category. Emami in many ways set the playbook for what an aggressive, marketing-heavy, M&A-driven heritage brand company could look like. Then there is P&G's Vicks — the multinational benchmark, with deeper marketing pockets and a more global supply chain. And then, increasingly, the Patanjali phenomenon, which from 2014 onward proved that the Indian consumer's appetite for "Ayurvedic" positioning was elastic enough to support a brand-new entrant doing tens of thousands of crores of revenue in under a decade.

Amrutanjan's position in this competitive set is genuinely unusual. Smaller than all of them. Older than most of them. Margin-rich. Cash-generative. And, after 2011, finally awake. Which is what created the conditions for what came next: the Comfee insurgency. But before we walk into the women's hygiene aisle, it is worth pausing on the man who set all of this in motion.

IV. Current Management: The S. Sambhu Prasad Era

If you had to identify the single decision that defines the modern Amrutanjan, it is not the 2011 rebrand and it is not the Comfee launch. It is the moment, somewhere in the middle of the previous decade, when S. Sambhu Prasad concluded that his job was no longer to be a custodian and started behaving like a capital allocator.

The distinction matters. A custodian's job is preservation — keep the product faithful, keep the family at the helm, keep the dividends flowing, do not break what works. A capital allocator's job is to take the cash thrown off by the existing business and ask, ruthlessly, where in the world it should be deployed to compound at the highest risk-adjusted rate. These are different jobs. They attract different temperaments. And the Indian family business landscape is littered with companies whose chairmen never made the transition.

Sambhu Prasad belongs to the fourth generation of the founding family. The lineage runs from the founder Kasinathuni Nageswara Rao through his son-in-law and successor Sambasiva Rao, through subsequent generations of Rajagopals and Sambhus, to the current chairman.[^4] He took on the role of managing director in the 2000s and has, since then, been the operational and intellectual centre of gravity for the company's transformation.

His public profile is deliberately low. Unlike the more visible Indian FMCG patriarchs — the Burmans of Dabur, the Mariwalas of Marico, the Agarwals of Emami — Sambhu Prasad does not court business television. His interviews are sparse, technical, and tend to focus on the operating questions rather than the personal narrative. The 2011 Economic Times piece announcing the rebrand is one of the more substantive he has given on the strategic logic, and even there the tone is matter-of-fact: the company needed to expand its category footprint, the corporate name was constraining the perception of what the company could be, the change was made.[^6]

This understated style has practical consequences. It means the company does not have, and has never sought, the celebrity-CEO premium that some of its peers enjoy. It also means that what gets discussed in earnings calls and annual reports is mostly what is actually happening in the business, rather than what the chairman wants the market to believe is happening — a meaningful distinction in Indian small and mid-cap land.

The shareholding structure tells you most of what you need to know about how the company is actually governed. Promoter holding sits in the neighbourhood of fifty percent — substantial enough to give the family unambiguous control, low enough that minority shareholders are a real constituency rather than a rounding error.4 There has been no meaningful pledging of promoter shares against margin loans, which in the Indian mid-cap context is itself a positive signal — the family is not personally levered against the equity of the listed entity. Institutional ownership, both domestic and foreign, has grown over the past several years as the company's transformation story has attracted attention from mid-cap-focused mutual funds.

The compensation structure is, by Indian standards, lean. The promoter-chairman's remuneration, on a standalone basis, is materially lower than what comparable MNC subsidiaries pay their imported CEOs.[^2] This is both a feature and, depending on how you look at it, a constraint. The feature is that corporate overhead does not eat into operating margin in the way it does at some peer companies — the value created accrues to all shareholders rather than being siphoned by a small executive cadre. The constraint is that attracting top-tier external talent for senior operating roles has, historically, required some creativity in the absence of MNC-scale compensation packages. The company has navigated this by offering the rarer commodity of long-term tenure and meaningful operating ownership of categories.

The cultural shift that Sambhu Prasad has overseen is more subtle than the strategic one. Family businesses run on relationships and intuition. Professional FMCG companies run on Nielsen scans, brand health trackers, retail-audit-driven SKU rationalisation, and zero-based budgeting cycles. Translating between these two operating paradigms — keeping the long-term brand stewardship that family ownership provides while importing the analytical rigour that professional management requires — is the actual day job of a chairman like Sambhu Prasad. From the outside, it is invisible. From the inside, it is the work.

The board composition reflects this hybrid model. Independent directors with consumer goods, finance, and governance backgrounds sit alongside family members and senior management.[^2] Audit committee, nomination and remuneration committee, stakeholder relationship committee — the standard governance scaffolding required of a listed company is in place, and on the disclosure dimensions that retail investors actually read (related party transactions, segment reporting, capital expenditure rationale), the company sits in the upper half of its mid-cap peer group.

The succession question, which haunts every Indian family business, is one the company has so far handled by not making it a headline. There are next-generation family members involved in the business, the management bench includes professionals who have been with the company for many years, and the transition — when it eventually happens — appears designed to be evolutionary rather than dramatic. This is, again, a more difficult thing to do well than to describe. The graveyard of Indian family businesses is full of companies that mishandled the third-to-fourth-generation transition.

The investor takeaway from the management chapter is roughly this. Amrutanjan today is run by a family that has skin in the game, by a chairman with a clear strategic worldview, by a board with adequate independent representation, and by an operating team with a meaningful blend of family loyalty and professional discipline. None of this is sufficient to guarantee outperformance. But it is the necessary condition for the second-act story — the one we are about to walk into — to even be plausible.

That second act, the one that has changed the shape of the company more than the rebrand and more than the celebrity advertising, is in the unlikeliest place. Not in pain balm. Not in beverages. In the women's hygiene aisle.

V. "Hidden" Businesses: Comfee and the Hygiene Pivot

Walk into a chemist shop in Coimbatore or Trichy or Madurai. Look for the sanitary napkin section. You will see the brands you expect — Stayfree (Johnson & Johnson), Whisper (Procter & Gamble), Sofy (Unicharm), Carefree (J&J again). You will also see, often at a slightly lower price point, often positioned next to the Stayfree pack, a brand called Comfee. Comfee is owned by Amrutanjan Health Care.

If your immediate reaction is "wait, the pain balm company makes sanitary pads?" — congratulations, you have just experienced the entire strategic point of the Comfee brand. It is a category extension that, by design, hides in plain sight. The brand does not aggressively trade on the Amrutanjan parentage. The packaging is its own. The positioning is its own. The retail buyer dealing with the Stayfree salesperson and then the Comfee salesperson does not, in many cases, immediately register that the second salesperson is calling on the same wholesaler that sells the yellow balm.2

This is deliberate, and it is the single most important strategic move the company has made in the post-rebrand era.

Here is the logic. The Indian सैनिटरी नैपकिन sanitary napkin market in 2010 was already large and growing fast. By the early 2020s it had become one of the most attractive feminine hygiene markets in the world — single-digit billion dollars in size, growing in the high single to low double digits annually, with penetration rates that still left enormous runway against the developed-market benchmarks.[^13] The category was, structurally, an FMCG dream: high-frequency, brand-loyal, price-elastic at the margin but loyalty-elastic at the centre, and benefiting from the demographic tailwinds of urbanisation, female labour force participation, and the reduction of the cultural taboo around discussing menstrual hygiene.

The category was also, by the end of the 2010s, dominated by two multinationals — Stayfree and Whisper — that between them controlled a material majority of organised market share. New entrants had tried. Most had failed. The two reasons were straightforward: the multinationals had decades of brand investment behind them, and they had distribution muscle that could lock up shelf space and trade margins faster than any insurgent could match.

Amrutanjan's bet, around the early 2010s, was that a particular wedge into this market existed. Not a frontal assault — that was unwinnable. But a flank manoeuvre, exploiting two weaknesses of the multinational position. First, the multinationals' distribution was strongest in modern trade and in the larger general trade outlets in tier-one cities. Smaller chemist shops in tier-two and tier-three towns, especially in South India, were less aggressively serviced. Second, the multinationals priced for a particular consumer segment — broadly, the urban middle class. The mass-market segment, especially in the South, was somewhat under-served at the lower price points.

Amrutanjan had, sitting on its balance sheet, exactly the asset that mapped onto these gaps: the deepest chemist-shop distribution network in South India, accumulated over a century of pushing yellow balm. The salesperson who walked into that chemist every fortnight to take the balm reorder could, with marginal incremental cost, also drop a Comfee carton on the same shelf.2 The infrastructure was already paid for. The relationships were already there. The only thing missing was the product.

The Comfee launch was deliberately quiet. The brand did not chase the same television-led, mass-market positioning the multinationals used. It built distribution first, awareness second, and let the product speak through trial. The pricing was set below the multinational benchmarks but not so aggressively low as to position the brand as a discount product. The product specifications — gel core, breathable cover, range of sizes — were competitive on a feature-by-feature basis. And the rollout happened, broadly, from South to North, leveraging the existing distribution strength.

The growth has been the story of the past decade for the company. Where the core pain management business has been a single-digit-to-low-double-digit grower over the medium term — appropriate for a mature category in which Amrutanjan already has high share in its core geographies — the hygiene segment has been compounding at materially higher rates, with management commentary across recent earnings calls suggesting compound annual growth comfortably in the twenties.5 Comfee has gone, in roughly a decade, from a small project inside a balm company to a meaningful contributor to consolidated revenue.

Segment-wise, the modern revenue split looks something like this. The OTC pain management franchise — the Yellow Balm, Amrutanjan Strong Pain Balm, the various sub-variants — accounts for the dominant majority of revenue and an even larger share of profit. It is the cash cow. It grows, in normal years, in the low-to-mid single digits with occasional double-digit prints in good monsoon and cold-and-flu seasons.[^2] The hygiene segment — Comfee — is the star: smaller in absolute revenue, but growing much faster, and crucially earning its way into a more meaningful share of the pie each year. The beverages segment — Fruitnik fruit drinks, the Electro+ rehydration line — is the wildcard.

Beverages deserve their own paragraph because they are the most controversial allocation of capital the company has made. The Fruitnik launch came in 2014, originally with a fruit juice positioning aimed at the health-conscious consumer.7 The strategic rationale was that the beverage category was large, growing, and increasingly health-skewing — the moves by competitors like Dabur (Real, Réal Activ), PepsiCo (Tropicana), and Coca-Cola (Minute Maid) had created a category framework into which a "wellness-positioned" entrant could slot. Amrutanjan added, over time, the Electro+ rehydration variant — an electrolyte drink positioned for active consumers, with a clear pivot from the original fruit juice framing.

Beverages, as a category, has objectively been the most difficult of the company's three pillars. The economics are harder. The cold chain requirements are different from the dry-goods distribution Amrutanjan was historically built for. The competitive set is brutal — multinational beverage companies treat India as a strategic market and will not let mid-sized local players take share without a fight. And the seasonal dependence is more pronounced than in the company's other segments.

The bull view on beverages is that the Electro+ pivot — leaning into the rehydration and active-lifestyle angle rather than the more commoditised fruit juice space — is a genuine product-market fit search that is still in progress, and that the eventual category prize is large enough to justify the experimentation cost. The bear view is that the company's beverage business is sub-scale, under-distributed, and is competing in a category where its core brand equity does not transfer naturally. Both views have merit. The financial reality so far is that beverages have absorbed capital without yet contributing materially to consolidated profit at scale.

The analytical question for any investor looking at Amrutanjan's segment mix is, essentially, the option-value question. The pain management business is what they own. The hygiene business is what is changing the shape of the company. The beverage business is, in the most charitable framing, optionality — a call option on a much larger market that may or may not pay off, but whose downside is bounded by the relatively modest capital allocated to it. How an investor weights these three streams determines, almost entirely, what they think the company is worth.

Which brings us, naturally, to the question of how the company has chosen to deploy capital across all of this — and what that choice tells us about how it has been run.

VI. M&A, Capital Deployment, and Benchmarking

There is a particular kind of Indian FMCG company that grows by acquisition. Emami bought Zandu in 2008. Dabur has acquired across geographies and categories for decades. Marico has done deals in personal care and South Asia. The acquisition route, at its best, telescopes years of organic distribution-building into a single transaction and gives the acquiring company immediate scale in a new category. At its worst, it loads the balance sheet with goodwill, distracts management, and dilutes culture.

Amrutanjan, conspicuously, has not gone down this road. Its expansion into hygiene was organic — own brand, own product development, own distribution build-out. Its expansion into beverages was organic. Its various sub-brand extensions within the pain management franchise have been organic. The company has, over its modern history, been a deeply unaggressive acquirer of other people's businesses.[^2]

This is a strategic choice, and it reflects two beliefs that run through the Sambhu Prasad-era management. The first is that the price of acquisitions in Indian FMCG, in the post-2014 era, has been structurally too high for a disciplined buyer to deploy capital comfortably. Multiples of fifteen, twenty, occasionally twenty-five times EBITDA have been routine for any reasonable consumer asset, and at those prices the cost of capital math becomes very difficult to justify unless the acquirer has unusually high confidence in synergy realisation. The second is that the company's existing distribution infrastructure — the chemist-shop relationships, the depot footprint, the regional sales force — is itself a productive asset that can support multiple product lines at relatively low marginal cost. If you already have the distribution, the cheaper way to grow is to put more product through it, not to buy another distribution network you would have to integrate.

This philosophy has consequences that show up in the financial statements. The most important of these is the asset-light nature of the business. Amrutanjan does not run extraordinarily heavy fixed assets relative to its revenue.[^2] Manufacturing for the core balm and hygiene categories is concentrated in a small number of plants, with sufficient capacity for medium-term growth. Working capital intensity is moderate by FMCG standards — inventory days and receivable days have been manageable, with periodic improvement as the company has tightened its supply chain operations.

The combination of asset-light operations and disciplined capital deployment translates into the metric that long-term equity investors actually care about: the return on capital employed. Amrutanjan has, over an extended period, generated returns on capital that compare favourably to its size-adjusted peer group, even though its absolute scale and growth do not match the larger Indian FMCG platforms.[^2] Return on equity has tracked similarly. These are not metrics that, in isolation, justify a particular valuation multiple — that depends on growth, optionality, and a dozen other things — but they are the metrics that confirm the underlying business model has been working as designed.

Inventory and receivables are less glamorous than ROCE but, for an investor trying to assess the operational quality of an Indian mid-cap, often more revealing. The boring efficiency gains of the past decade — cycle time reduction in inventory, faster collections from the distribution network, more disciplined stock-and-sale management — are visible in the working capital metrics if you know where to look.[^2] The improvements have been incremental rather than dramatic, which is the right kind of improvement for a company of this stage. Dramatic working capital improvement usually signals either a crisis being fixed or an accounting choice being changed; incremental improvement signals a management team that is actually doing the work.

Capital allocation during the 2020-2022 pandemic period is an instructive case study. When COVID hit in early 2020, Amrutanjan, like every consumer goods company in India, faced a mix of demand shocks (lockdowns, channel disruptions) and demand windfalls (categories like rehydration and immunity-related products saw spikes). The company's response was disciplined. It did not rush into acquisitions at a moment of widespread asset distress. It did not load up on inventory in anticipation of a demand surge that might or might not come. It did, however, accelerate the launch of the Electro+ rehydration line — a product whose positioning aligned with the pandemic-era surge in hydration, electrolyte, and active-lifestyle awareness, and which gave the beverages segment a clearer reason to exist.5

Dividend policy has been steady through this period — the company has been a consistent dividend payer, with payout ratios calibrated to leave sufficient cash on the balance sheet for the ongoing growth investments in hygiene and beverages without starving shareholders.[^2] The balance sheet itself is, by Indian listed-company standards, conservatively run. Net cash or near-net-cash for extended periods. Modest debt at most. No exotic financial instruments. The financial conservatism is the natural counterpart to the operational ambition — when you are placing bets in two new categories simultaneously, the last thing you want is a fragile capital structure forcing decisions.

Benchmarking against the peer set, the Amrutanjan profile is distinctive. Compared to Emami, the company is smaller, less acquisition-dependent, and more concentrated in fewer categories. Compared to Dabur, it is materially smaller, less geographically diversified, and less integrated into the Ayurvedic primary care space. Compared to Procter & Gamble Hygiene & Health Care (the listed Indian arm), it is less profitable in absolute rupees but, on a returns basis, surprisingly close — a function of the asset-light model and the dominant share in its niche.

The investor question that emerges from the capital allocation chapter is whether this conservative, organic, low-leverage approach is a strength or a constraint. The bull view is that it is precisely what has allowed the company to enter difficult new categories without blowing up the balance sheet, and that the optionality being built quietly in hygiene and beverages will, over time, look obvious in retrospect. The bear view is that conservative capital allocation in a market full of growth opportunities can be a form of risk aversion that costs shareholders the returns that more aggressive players are capturing.

Both views are reasonable. The empirical answer, which is the one that matters, is: ask again in five years.

Now we come to the part where any self-respecting Acquired episode reaches for the analytical frameworks. Hamilton Helmer's 7 Powers. Michael Porter's 5 Forces. The standard scaffolding for thinking about why a business is what it is, and what could change that.

VII. The Playbook: 7 Powers and Porter's 5 Forces

Take the Yellow Balm in your hand. What, in Hamilton Helmer's vocabulary, is the source of its persistent profitability? Why has this product, from this company, in this packaging, made money for one hundred and thirty-three years? Why have hundreds of attempted competitors come and gone while it remains?

The dominant power, by some distance, is brand. In Helmer's framework, brand is a power when it allows a firm to charge a higher price (or capture more volume at the same price) for a functionally similar product, and when that price/volume premium is durable against competitor attack. Amrutanjan's balm, by any objective laboratory standard, is not meaningfully different from the half-dozen other menthol-camphor-eucalyptus topical analgesics on the Indian market. The active ingredients are well-known, off-patent, and replicable in a competent contract manufacturing facility for a fraction of Amrutanjan's price.

What Amrutanjan has that no competitor can replicate is one hundred and thirty years of mother-to-daughter, grandmother-to-grandchild, household-to-household trust. This is the kind of brand asset that Helmer specifically highlights as a "cornered resource" when paired with the difficult-to-overstate truth that you cannot, at any price, manufacture a hundred years of memory. A new entrant could outspend Amrutanjan ten-to-one on advertising for a decade and still not buy back the loyalty that comes from the product being the one your mother used when you were five.3

The second power, more modest in scale, is scale economies — but only within geography. The distribution network that Amrutanjan built across South India, particularly its dense penetration into independent chemist shops and small general trade outlets, is itself a scale asset. It allows incremental product launches (Comfee being the obvious example) to be rolled out at a marginal cost-of-distribution that a sub-scale competitor cannot match. Outside South India, this advantage diminishes — the company is a smaller player in the North, and the scale economy works against it rather than for it.

The third power — and this is where the modern strategy gets interesting — is counter-positioning. Helmer's classic example of counter-positioning is when an incumbent's strengths become liabilities against an entrant whose business model the incumbent cannot copy without cannibalising itself. Amrutanjan's "natural Ayurvedic heritage" positioning sits in productive counter-position to the multinational competitors whose entire identity is built around a Western, chemical, science-led framing. P&G cannot suddenly position Vicks as Ayurvedic without creating profound brand-architecture problems for itself globally. This asymmetry has, particularly in the post-2014 wave of consumer interest in "natural" products, given Indian heritage brands a real wedge.

The fourth and fifth Helmer powers — switching costs and network effects — are largely absent in this category. Topical analgesic consumers can switch costlessly. There are no multi-sided dynamics. Process power, the sixth, is modest — there is some process know-how in formulation and quality control, but it is not a dominant moat. Cornered resources, the seventh, comes back to the brand — and in a sense, also to the deep distribution relationships that have been built over generations.

Now flip the framework. Michael Porter's Five Forces, applied honestly to Amrutanjan's competitive landscape, paints a more sobering picture.

Rivalry is intense. The pain balm category alone hosts Zandu, Vicks (Procter & Gamble), Iodex (GlaxoSmithKline), Tiger Balm (Haw Par Corporation), Volini (Sun Pharma), Moov (Reckitt), and dozens of regional players. The hygiene category hosts Stayfree, Whisper, Sofy, Carefree, and a wave of D2C entrants. The beverage category hosts the entire global beverage industry.

Bargaining power of buyers is bifurcated and worth thinking about carefully. For the balm, buyer power is low. Consumers do not negotiate on a thirty-rupee balm purchase. Habit formation, low ticket size, and strong brand loyalty mean Amrutanjan can pass through cost increases with relatively limited demand impact. For the beverage category, buyer power is much higher. Consumers shop on price, promotion, and shelf placement, and the loyalty that defines the balm purchase does not transfer to a fruit juice purchase.

Bargaining power of suppliers is mixed. The key raw materials are menthol, camphor, eucalyptus oil, and various excipients — agricultural commodities subject to global price cycles. Menthol in particular has been periodically volatile, with prices moving meaningfully on the back of crop conditions in major producing regions. The company has, like all balm manufacturers, had to manage through periodic raw material spikes by adjusting product pricing, packaging, and gross margin sequencing. This is not a unique disadvantage relative to peers but it is a real input-cost risk.

Threat of substitutes is, candidly, the most under-appreciated risk. Topical balms compete, at the margin, with oral painkillers (paracetamol, ibuprofen) which have become increasingly cheap, accessible, and routinely used for the same headaches and body aches that the balm category was historically reached for. As Indian consumers have become more comfortable with oral OTC pharmaceuticals, the share of mind for a topical analgesic has, in some segments, shifted. The company's response has been to lean into the "natural" and "topical" positioning that oral painkillers cannot match — but the substitution pressure is real and worth tracking.

Threat of new entrants varies by sub-category. In the core pain management franchise, the brand moat described above makes new entry difficult — a credible challenger needs to either spend enormous sums on advertising or come in with a genuine product innovation. In hygiene, new entrants have been arriving steadily, particularly through D2C channels. In beverages, the market is wide open and well-capitalised challengers can launch products quickly.

The pattern that emerges from running both frameworks is, broadly, this. Amrutanjan has a deep, durable, hard-to-replicate moat in its core pain management franchise, particularly in South India. It has built a credible and growing position in hygiene, where its moat is shallower but its strategic flank attack on the multinational incumbents has worked because the competitive set was not paying close attention. It has a much weaker competitive position in beverages, where it is one of many entrants in a category dominated by global giants.

This is not a uniformly defensible business. It is a business with one fortress, one expanding fortification, and one outpost. Whether the outpost ever becomes a fortification, or remains a useful but sub-scale presence, is the open question.

Which is the natural setup for the part of every Acquired episode where we earn our keep by laying out the bull and bear cases.

VIII. Bear vs. Bull Case

The bear case starts with geography. Amrutanjan, despite a decade of explicit work on national distribution expansion, remains a meaningfully South-skewed company. The Hindi-speaking belt is the largest consumer goods market in India by population, by household formation, and increasingly by per-capita income. It is also a market in which Amrutanjan is, candidly, a smaller player than the Vicks-Iodex-Volini incumbents and, more recently, than Patanjali. Building genuine national distribution parity with these competitors is a multi-decade exercise, and the bear case argues that the company's progress has been respectable but not transformational. If the North never becomes a profit centre comparable to the South, the company's growth ceiling is structurally lower than the bulls assume.

The bear case continues with beverages. The Fruitnik and Electro+ businesses have absorbed management attention and capital for over a decade and have not, by most readings of the segmental disclosures, achieved scale that justifies the strategic real estate they occupy.5 In a charitable framing, this is investment-period optionality. In an uncharitable framing, it is what the bears like to call "diworsification" — a category venture into adjacent territory that does not leverage the core brand equity, that competes against larger and better-funded incumbents, and that distracts the leadership team from where the real opportunity lies. The bear concern is that beverages are, in operational metaphor, the company's Tata Nano — a product the management is too institutionally invested in to kill, even when the market signals indicate it is not working.

Raw material risk is a third bear pillar. Menthol prices are subject to crop cycles, geopolitical disruptions, and currency volatility. The company has, over the years, managed these with some skill, but there are quarters and even multi-quarter periods in which gross margins have been visibly compressed by input cost spikes.[^2] An asset-light business with limited backward integration is structurally exposed to this dynamic. The bear case argues that the gross margin profile of the next decade may be less stable than the historical average.

Substitution risk to oral painkillers, discussed above, is a slow-moving but persistent bear factor. So is the increased ease with which D2C brands can launch in the hygiene category, supported by venture capital, online distribution, and influencer marketing — a competitive vector that did not meaningfully exist when Amrutanjan first launched Comfee.

The bear summary is something like this: a high-quality regional cash cow, professionalised competently, that may not be able to translate its South India strength into national leadership, whose adjacency bets are mixed at best, and whose valuation does not always reflect the structural ceilings that the operating reality imposes.

The bull case starts in exactly the opposite place. The bulls argue that the Comfee business is the most under-appreciated asset on the company's balance sheet. If Comfee continues to compound at its current trajectory, even partially, the share of the company's revenue and profit attributable to feminine hygiene will rise materially over the next several years. And the moment that share crosses some psychological threshold — bulls argue forty percent or so — the market's valuation framework for the business will be forced to re-rate.

The re-rating logic is mechanical. Today, the equity market values Amrutanjan as a regional pain balm company with adjacency bets. The valuation multiple — pick your preferred earnings or sales metric — sits in the range typical for that descriptor. If Comfee becomes large enough that the company is genuinely a multi-category modern FMCG, the appropriate comparable set shifts from regional balm peers to platform consumer companies — Marico, Dabur, even the listed P&G hygiene entity. The multiples in that comparable set are materially higher.[^13] The "multiple re-rating on category mix shift" is the central bull thesis.

The bull case also leans on the optionality of beverages. The bear views Fruitnik and Electro+ as a sunk cost. The bull views them as a pre-paid call option on a category that, if even one product finds genuine fit, could surprise. The Indian beverage market is gigantic and growing. The cost of maintaining the optionality, given the company's overall financial conservatism, is bounded.

The bull cites the brand. One hundred and thirty years is not a number that can be dismissed. Brand assets of this duration, in this geography, with this level of household-level recognition, are vanishingly rare globally. The bull does not argue that the brand alone justifies any particular valuation — it argues that the brand is a genuine compounding asset whose value is under-counted in standard discounted cash flow exercises that weight near-term cash heavily and distant cash lightly.

The bull cites the management. Skin in the game, demonstrated discipline through cycles, no leveraged accidents, no governance scandals, no related-party gymnastics, lean overhead, capable transition to professional management — the qualitative governance scorecard is, by Indian mid-cap standards, well above average.

The bull cites the asset-light, return-on-capital-strong, low-leverage profile of the business — the kind of business profile that generates compounding returns through cycles, that does not blow up in downturns, and that offers attractive margin of safety for long-horizon investors.

So which is right? In the spirit of an episode that does not give a target price or a buy-sell — and that is the rule we honour here — the more useful synthesis is to identify the variables that an investor needs to track to know which case is winning over time.

The first key performance indicator is the segment revenue mix between OTC pain management and hygiene. If hygiene's share of revenue continues to rise meaningfully over multi-year windows, the bull case is on track. If it stalls, the bear case strengthens.

The second is the company's gross margin profile, particularly through periods of menthol price volatility. The ability to defend and grow gross margins through input cost cycles is a direct test of the brand's pricing power and the operating team's discipline.

The third is non-South geographic revenue contribution. The bear's central claim is that the company cannot break out of the South. The bull's defence requires that this break-out is, slowly, happening. The disclosed regional revenue split — to the extent it is disclosed — is the empirical scoreboard.

These three KPIs — hygiene revenue share, gross margin, and non-South geographic share — are the most useful instruments for an outside investor to monitor whether the second-act story is on track. Everything else is commentary.

The Acquired-style framework, when applied honestly, suggests that Amrutanjan today is neither a clear compounder nor a clear value trap. It is an option on a transition. The transition is real, the management executing it is competent, the cash cow funding it is productive, and the bets being placed are, by the standards of Indian mid-cap FMCG, intelligently sized. Whether the transition arrives at its destination — a multi-category modern Indian FMCG with national scale — is a question that the next five to ten years will answer.

Which brings us, as every Acquired episode must end, to the lessons.

IX. Epilogue and Lessons

There is a particular quality to Indian businesses that have survived a hundred years. They are not, on average, the businesses you would expect. They are not the technologically dazzling. They are not the strategically aggressive. They are not the marketing-genius cases. They are, more often, the businesses that did one thing well, did it consistently, did it cheaply enough that they could weather every macro shock the subcontinent could throw at them, and inherited — almost by accident — a level of trust that no marketing budget could ever buy.

Amrutanjan is one of these. The Yellow Balm was not a strategic masterstroke when it was launched in 1893. It was a product. A good product, well-formulated, decently packaged, sold at a price the market could bear. The freedom-fighter aura around the founder gave it a soft power that proved to be enormously valuable, but it was not the product's reason for being. The product's reason for being was that it worked, it was affordable, and the people who bought it kept buying it.

For most of the twentieth century, the company did not need a strategy. It needed not to make mistakes. The Yellow Balm sold itself, the cash cow generated cash, the family stewarded the asset, and the business compounded slowly, steadily, unspectacularly.

What changed in the 2010s, and what makes the company an interesting case study now rather than a curiosity, is that the leadership recognised — earlier than it had to, which is the harder thing — that the world the cash cow had been built for was no longer the world the cash cow was operating in. Modern retail, multinational marketing, demographic shifts, urbanisation, the rise of D2C, the broadening of consumer categories — all of these were eating, slowly, into the conditions that had made the single-product strategy optimal.

The lesson, for any founder or operator looking at a cash-rich legacy business, is the lesson Sambhu Prasad and his team appear to have absorbed. Use the cash cow to fund the optionality. Do not rely on the cash cow being eternal. Place bets in adjacent categories where the existing distribution and brand assets give you a disproportionate launch advantage. Place those bets while the cash cow is still healthy enough to fund them, because the alternative — placing them when the cow is sick — is much harder. And do not let the symbolic weight of the legacy product foreclose the strategic question of whether the company should still be defined by that product in twenty years.

The second lesson, for investors trying to evaluate companies in this stage of the lifecycle, is that the qualitative judgements matter as much as the quantitative ones. Does the management actually have skin in the game, or just nominal equity? Is the family allocating capital like an owner or extracting it like a custodian? Are the adjacency bets sized intelligently — large enough to matter if they work, small enough not to break the company if they fail? Is the corporate governance hygienic, or are there warning signs in related-party transactions, board composition, or executive compensation? These questions, asked rigorously, will tell an investor more about long-term outcomes than any spreadsheet model will.

The third lesson is about brands themselves. Brand equity is, in the standard finance textbook, an intangible asset that is hard to value and harder to depreciate. In practice, it is one of the most durable economic moats that exists. A brand that has been in households for one hundred and thirty years is not just an asset; it is an inheritance. It cannot be created by any amount of marketing spend. It can be destroyed, however, by inattention, by quality lapses, by category irrelevance, or by management hubris. The job of the steward of such a brand is, in the most literal sense, to pass it on intact. The job of the modern steward is to do that while also ensuring the company remains relevant to the next generation of consumers, who do not remember what their grandmothers used.

Amrutanjan's story, told honestly, is the story of a company learning — slowly, deliberately, with appropriate humility — how to do both. Whether it succeeds is not yet clear. What is clear is that the attempt is genuine, the framework for the attempt is sound, and the assets being deployed in the attempt are real.

For anyone watching the slow, unglamorous work of category extension in Indian FMCG, this is a company worth paying attention to. The yellow bottle, with the red border, that has lived in the medicine cabinet for one hundred and thirty-three years, is not done with its story yet.

References

References

-

Amrutanjan: The balm brand is now soothing other pains — Forbes India, 2021-06-15 ↩↩↩

-

How Amrutanjan is keeping its 128-year-old legacy alive — Afaqs!, 2022-02-10 ↩↩

-

Amrutanjan Health Care Quarterly Earnings — Moneycontrol ↩↩↩

-

Amrutanjan: A Century of Healing — Business Standard, 2015-05-30 ↩↩

-

Amrutanjan to focus on beverages, pain management — Financial Express, 2019-03-24 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube