Sejal Glass: The Phoenix of Indian Architectural Glass

I. Introduction & The Mystery of the Phoenix

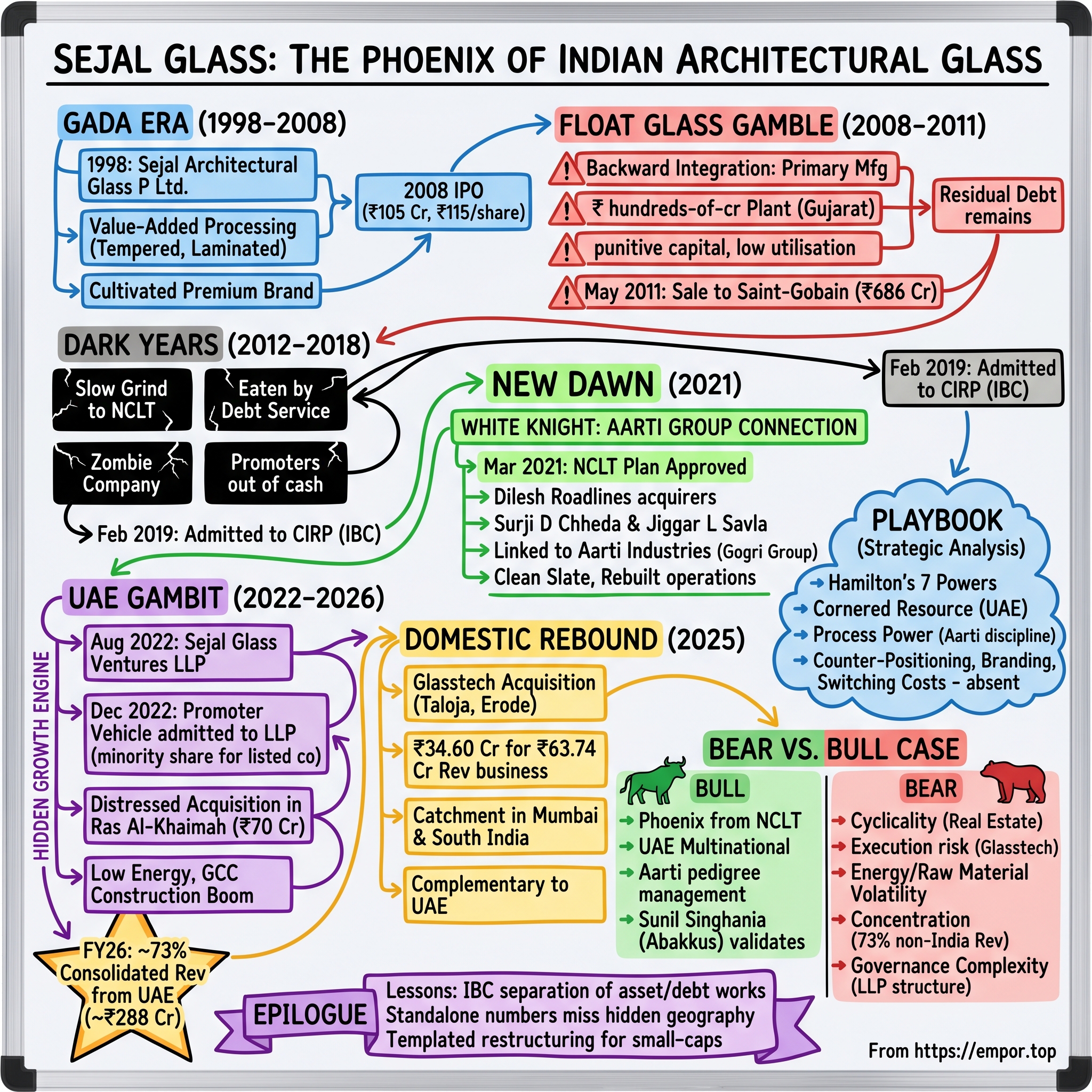

Walk into the lobby of any new Grade-A office tower in Mumbai or Bengaluru and look up. The shimmering double-glazed facade, the floor-to-ceiling tempered panels, the whisper-quiet acoustic interlayer separating you from the chaos outside — all of it is the work of an industry most public-market investors have never bothered to map. Architectural glass in India is a fragmented, capital-hungry, cyclical business dominated by a small handful of integrated giants and a long tail of family-run processors. It is not the kind of industry that produces multi-bagger turnaround stories.

And yet, on the screens of every momentum-watching trader on Dalal Street in early 2026, a small-cap with the ticker SEJALLTD.NS quietly told one of the most improbable comeback stories in recent Indian equity market history. A company that had been formally pronounced dead in a बंबई Mumbai courtroom in February 2019 — admitted to the Corporate Insolvency Resolution Process under the इन्सॉल्वेंसी एंड बैंकरप्सी कोड Insolvency and Bankruptcy Code, its old equity holders staring at a near-total wipeout — had somehow, by the spring of 2026, become a fast-growing multinational glass processor with a market value approaching ₹900 crore and a who's-who of Indian institutional investors clamouring for placement allocations.1

Stranger still: most of its revenue was no longer being earned in India at all.

The hook of this story is geographic misdirection. SEJALLTD is listed on the भारतीय राष्ट्रीय स्टॉक एक्सचेंज National Stock Exchange of India and disclosed in rupee terms, but by the end of FY26, roughly three-quarters of its consolidated top line was being generated out of a manufacturing campus in رأس الخيمة Ras Al-Khaimah, the second-smallest of the seven United Arab Emirates.2 The Indian listed parent had effectively become a holding-company wrapper around a UAE operating subsidiary — an inversion that almost no domestic small-cap analyst had on their bingo card going into 2024.

The second hook is genealogical. The promoter group that pulled this off is not a glass family at all. The capital and the strategic mind behind the rebuild trace back, through a sleepy logistics company called दिलेश रोड लाइन्स Dilesh Roadlines, to investors and operators with deep ties to the chemicals empire built around आरती इंडस्ट्रीज Aarti Industries — a name long associated with one of India's most disciplined, process-driven business families.3 The connection is not advertised on the company's homepage, but it is the single most important fact about how this Phoenix learned to fly.

This is the story of how a debt-laden, family-run float glass dreamer was pulled into bankruptcy court by a misadventure in primary manufacturing, scrapped down to its corporate shell, sold to a chemical-industry-backed roads-and-trucking holding company, and rebuilt — against every conventional small-cap intuition — as an export-oriented architectural glass processor with its centre of gravity sitting on the wrong side of the Arabian Sea. It is also a study in how the Indian Insolvency and Bankruptcy framework, often criticised for its slowness and haircuts, can in the right hands function as exactly what it was meant to be: a mechanism for moving distressed productive assets into better operators' hands.

To understand how Sejal got here, we have to begin where every Indian family-business saga begins — with four brothers, a small workshop, and an ambition that eventually outran the family balance sheet.

II. Foundations & The Gada Era

The Gada family did not start in glass. They started, like so many of गुजरात Gujarat's trading-caste entrepreneurs who made Mumbai their home in the second half of the twentieth century, in the messy adjacencies of the construction value chain — sourcing, distributing, and installing building materials for the developers reshaping the skyline of suburban Bombay. By the late 1990s, India's economic liberalisation had unleashed a new aesthetic in commercial real estate. The dull, punched-window concrete boxes of the licence-raj era were giving way to glass-clad facades borrowed from the towers of Singapore and Dubai. Somebody was going to have to learn to cut, temper, laminate, and install all of that glass at scale. The Gadas decided it would be them.

In 1998, A.S. Gada and his three brothers incorporated the company as Sejal Architectural Glass Private Limited.4 By 1999, it had been converted into a public limited entity, a typical structural step taken in anticipation of eventual capital raising. For the first decade of its life, Sejal occupied a thoroughly unglamorous slice of the value chain: it bought float glass — the raw, transparent ribbon produced by a handful of giant primary manufacturers globally — and processed it into the higher-value forms that architects, interior designers, and developers actually specified. Tempering for safety. Lamination for security and acoustic dampening. Insulating glass units for thermal performance. Decorative glass for the increasingly elaborate Indian wedding-and-mall economy.

This was, in industry terms, a "value-added" business, but the value-add was modest. The processor's margin sat on top of a commodity input price that he did not control, and he competed against a long tail of regional fabricators willing to underprice him on volume work. What set Sejal apart in the early 2000s was branding. The Gadas, particularly Amrut Gada, were unusually focused on positioning the company as a premium architectural partner rather than a commodity job-shop. The marketing positioned glass as a material of expression — "glass as art" — and Sejal cultivated relationships with some of the biggest names in Indian architecture and high-end residential development. For a brief moment in the mid-2000s, Sejal was the name a star architect would specify in a project brief without flinching.

Then came the IPO. The boom market of 2007–2008 was an irresistible window for any mid-sized family business with a credible growth story, and Sejal Architectural Glass walked through it. In June 2008, the company offered 91.94 lakh equity shares of ₹10 face value at an issue price of ₹115, raising approximately ₹105.73 crore.5 The shares listed on the BSE and NSE on July 1, 2008.5 In hindsight, the timing was both impeccable and catastrophic. Impeccable because the Gadas raised real money at a real valuation in the last quarter before the global financial crisis broke open. Catastrophic because the use of those proceeds — and a great deal more debt that followed them — was about to entomb the company.

The decision that defines this era was not the IPO itself. It was what the Gadas chose to do with the IPO proceeds and the bank lines that the listing made available to them. By late 2008 and into 2009, the family had committed to a strategic move that, on paper, looked like the most logical thing in the world for a successful glass processor to do: backward integrate into the manufacture of the raw float glass they had been buying from somebody else.

The logic was textbook. Float glass is the largest cost line in any architectural glass processor's bill of materials. If Sejal could make its own float, it would capture the primary manufacturer's margin in addition to the processor's margin, and it would never be at the mercy of a supplier raising prices in a tight market. The pitch deck practically wrote itself. What the deck did not say — what no Indian glass processor before or since has fully internalised in time — is that primary float glass is one of the most punishing capital-intensive businesses in the entire building products complex, and that the unit economics turn brutally against you the moment your utilisation drops below the high eighties.

The Gadas, in their conviction, were about to learn this in the worst possible way.

III. The Float Glass Gamble: A Near-Fatal Mistake

To understand why the float glass plant nearly killed Sejal, you have to understand how float glass is actually made. The process, invented by Sir Alastair Pilkington in the 1950s and now standardised globally, involves floating a continuous ribbon of molten glass over a bath of liquid tin in an oxygen-controlled chamber, drawing it out at a precise rate, annealing it slowly, and cutting it to size. The chamber must be heated to roughly 1,500°C, twenty-four hours a day, three hundred and sixty-five days a year. You cannot turn a float line off. If you do, the molten glass solidifies in the bath, the tin oxidises, and the chamber must be effectively rebuilt from scratch — a multi-month, hundreds-of-crores undertaking. The economics, therefore, are merciless: you must run the plant flat-out at all times, which means you must sell every tonne it produces at any price the market will give you, which means that float glass is the single most cyclically exposed segment in the entire flat-glass value chain.

The Sejal plant was sited in झगडिया Jhagadia, in Bharuch district of Gujarat — a sensible choice, near the ports, the gas grid, and the silica sand belts of the western coast. It was designed for an output of roughly 550 metric tonnes per day, putting Sejal squarely on the same competitive playing field as global majors like Saint-Gobain, Asahi, Guardian, and the Indian incumbent गुजरात गार्डियन Gujarat Guardian. The total project cost ran well into the high hundreds of crores, financed through a combination of IPO proceeds, internal accruals, and — fatally — a substantial term loan stack from a consortium of Indian banks.

The plant fired up just as the global building products complex was entering one of the worst stretches in its modern history. The 2008–2009 financial crisis hammered commercial construction worldwide. Chinese float glass producers, sitting on a wave of state-supported overcapacity, began dumping product into export markets including India. Domestic incumbents responded with predatory pricing to defend share. Sejal, the new entrant with the highest debt service burden per tonne in the market, found itself unable to either run the plant at the utilisation it needed or charge the price it had modelled. Cash from operations failed to cover interest. Interest got rolled into more debt. Within two years, the float glass venture had transformed Sejal from a profitable processing brand into a balance sheet emergency.

In May 2011, the Gadas pulled what looked at the time like the rip cord. They announced the sale of the entire float glass business — the Jhagadia unit, the brand-new technology, the workforce, and the supply contracts — to Saint-Gobain Glass India Ltd for a gross consideration of ₹686 crore.6 The buyer was the natural one: Saint-Gobain, the French building materials titan, was aggressively expanding its Indian float glass footprint and could absorb the asset into a network where high utilisation was guaranteed.7 As part of the transaction, Sejal and its principal promoters accepted non-compete obligations in Indian float glass for five years, with no separate non-compete fee paid out to the family.6

On the headline, ₹686 crore looked like a clean exit. In reality, it was a partial bandage on a wound that had already gone septic. The proceeds went substantially toward repaying the secured lenders who had financed the plant, but a significant slug of legacy debt remained on the rump entity, alongside the operating overheads of the smaller processing business that the family had retained. The processing business by itself was not generating enough cash to service the residual debt at the interest rates Indian banks were charging mid-cap industrial borrowers in the early 2010s. The float glass adventure had left Sejal walking with a structural limp.

What this episode reveals about strategy is something that recurs throughout Indian mid-cap industrial history. Backward integration is seductive precisely because it looks like vertical capture of the value chain — and on a healthy demand-supply environment with cheap capital, it can be. But in any cyclical primary manufacturing segment, the operator who funds the integration with debt rather than equity is taking on a hidden second bet: not just that the integration will work, but that the cycle will cooperate while the debt is being amortised. The Gadas lost that second bet, and the consequences would compound for the next eight years.

The slow march to NCLT had begun.

IV. The Dark Years & The Collapse

The years between 2012 and 2018 are the part of the Sejal story that nobody wants to dwell on, and that is exactly why they are the most instructive part of it. There was no single dramatic event in this stretch. There were no fraud allegations, no sudden customer losses, no factory fires. What there was, instead, was the slow, grinding, almost geological process of a company being eaten alive by the gap between its operating cash generation and its debt service obligations.

In the typical month of this era, Sejal's processing plants would run, ship product, collect receivables, and generate a small operating profit. That operating profit would be meaningful in absolute terms — these were not bad businesses, in isolation. But by the time the interest expense on the residual term loans and working capital lines was deducted, the bottom-line was either a small loss or a loss large enough to force another rollover negotiation with the lenders. The promoters infused capital, then infused more, then ran out of personal balance sheet to infuse. The lenders restructured, then restructured again, then ran out of regulatory cover to restructure further. Suppliers began demanding cash on delivery. Customers began routing orders to competitors who could guarantee delivery dates without payment-term gymnastics. The Sejal brand, so carefully cultivated through the 2000s, began to fade from the architects' specs.

This is what financial analysts mean when they use the word "zombie." A zombie company is one that is operationally alive — it has staff, plants, products, customers — but financially undead, generating just enough cash to keep the lights on and the interest accruing, but not enough to ever realistically retire principal. Zombies do not die quickly. They stagger forward for years, often for the better part of a decade, until some combination of regulatory change, lender exhaustion, or external shock topples them. For Sejal, the toppling agent was a piece of legislation that India had only recently enacted: the Insolvency and Bankruptcy Code, 2016.

The IBC, passed by Parliament in May 2016, fundamentally rewrote the rules of corporate distress in India. Before the IBC, defaulting borrowers could string lenders along almost indefinitely through writ petitions, debt recovery tribunals, and the structural inertia of the Indian judicial system. After the IBC, a single financial creditor with an undisputed claim above ₹1 crore could file an application before the National Company Law Tribunal, and if admitted, the existing management would lose control to a court-appointed Resolution Professional within weeks. The clock would start ticking on a bounded process — originally 180 days, extendable to 270, eventually expanded to longer windows in practice — at the end of which either a resolution plan would be approved or the company would head to liquidation.

For corporate India, the IBC was an existential cultural shock. For Sejal's lenders, it was the lever they had been waiting for. On February 12, 2019, the company was admitted by the Mumbai bench of the NCLT into the Corporate Insolvency Resolution Process under the IBC.8 An Interim Resolution Professional was appointed. The board of directors was suspended. Trading in the shares continued but under restrictions. The Gada family, after more than two decades at the helm of the business they had built from a small architectural glass workshop into a listed company with international ambition, no longer ran it.

Three things are worth pausing on about this moment. First, the CIRP did not happen because Sejal was a fraud, or because management was incompetent. It happened because management had made one bet too big — the float glass plant — at the wrong moment in the global cycle, and the leverage taken to fund that bet outlived the strategic logic that had justified it. Second, the IBC did not, as is sometimes alleged, "destroy" value at Sejal. The destruction had already happened in 2009–2011. The IBC merely formalised the recognition of it and created a mechanism for the residual productive assets to be transferred to a new owner. And third, the resolution process at Sejal would prove unusually consequential, because of who was about to walk into the courtroom with a plan.

V. Enter the White Knight: The Aarti Group Connection

Indian insolvency court hearings, for all their legal drama, are mostly tedious affairs conducted in fluorescent-lit rooms in dreary government office complexes. The procedural orders that emerge from them rarely make headlines outside of a small circle of insolvency lawyers and distressed-debt analysts. So it was with the Sejal CIRP. By March 26, 2021, two years and one month after the admission, the Mumbai bench of the NCLT approved a Resolution Plan submitted by the Successful Resolution Applicants — and with that order, all claims not forming part of the approved plan stood extinguished.8 The Gada chapter, formally, was over. The new chapter, less formally, had already begun.

The new promoter group did not fit any of the templates that distressed-asset watchers might have predicted. They were not a strategic competitor in glass. They were not a turnaround-focused private equity fund. They were a name almost nobody outside of a specific corner of Mumbai's industrial finance world had heard of: दिलेश रोड लाइन्स Dilesh Roadlines Pvt. Ltd., a privately held company whose stated business activity was, of all things, road transportation.

Why a road transportation company would acquire control of a distressed listed glass processor is a question that makes sense only when you look past the corporate registry filing and into the personal networks of the people behind it. The principal architect on the new promoter side was सुरजी दामजी छेड़ा Surji Damji Chheda, a financial professional with what the company's own director profile describes as more than four decades of experience in direct taxes, audit, investments, and financial consultancy.9 His co-promoter and operating partner was जिग्गर लक्ष्मीचंद सावला Jiggar Lakshmichand Savla, an MBA in Marketing who simultaneously served as a director of Delicare Lifesciences Private Limited, a company in which he handled finance and operations.9

What made these names significant was the company they kept. Public profiling of the post-resolution shareholding pattern of Sejal Glass linked the Chheda promoter group to Mr. चंद्रकांत गोगरी Chandrakant V. Gogri, the co-founder of आरती इंडस्ट्रीज Aarti Industries — one of India's largest specialty chemicals platforms by market capitalisation and a textbook example of disciplined, decades-long compounding under family-promoter control.10 This was not a one-line passing connection. The reporting framed the new majority of Sejal Glass as effectively held jointly by the Aarti-linked Gogri group and the Chheda group, with the public float reduced to a minority slice.10

For investors who know how to read the signals, this was a thunderclap. Aarti Industries is a name associated with a very specific style of Indian industrial value creation: long-cycle, capital-allocation-disciplined, process-engineering-led, with a famously conservative attitude to debt and a famously patient attitude to compounding. The fact that capital and reputation associated with that ecosystem was now sitting on the cap table of a tiny, distressed glass processor implied a thesis that the new owners themselves had not bothered to explain in detail in any single filing — but that, when you assembled the pieces, became unmistakable.

The thesis was that architectural glass processing was a structurally attractive end-market — riding India's commercial real estate revival, the GCC's permanent construction boom, and the global retrofit cycle for energy-efficient facades — but that the industry in India was operationally fragmented, family-run, sub-scale, and consistently under-managed. A team that brought disciplined capital allocation, financial rigour, and a willingness to execute distressed-asset roll-ups could, over a five to ten year horizon, build a meaningful regional player out of the wreckage of less disciplined predecessors. Sejal, with its existing brand recognition, listed-company status, and clean post-CIRP balance sheet, was the perfect chassis for that thesis.

What the Resolution Plan did, mechanically, was almost surgical. The pre-existing equity was substantially restructured to reflect the value-extinguishment that had already occurred. Fresh capital was infused at the new promoter level. The debt stack was either paid down per the approved plan terms or extinguished as part of the resolution. The company emerged from CIRP on a clean slate — small, but clean — and ready to be rebuilt.

For the next eighteen months, very little happened in public. The new owners did not make grand strategic announcements. They did not do roadshows. They quietly stabilised the operations, rebuilt customer relationships, and — most importantly — began scouting for the asset that would become the centrepiece of the rebuild. That asset was not in India.

VI. The UAE Gambit: The "Hidden" Growth Engine

Ras Al-Khaimah is not the part of the United Arab Emirates that makes Western magazine covers. The headlines belong to دبي Dubai, with its towers and tourism, and to أبو ظبي Abu Dhabi, with its sovereign wealth and oil revenues. Ras Al-Khaimah, the northernmost of the seven emirates, has built a quieter identity as a cost-competitive industrial base — fast-track licensing, free zones designed for export manufacturers, low energy and labour costs by GCC standards, and a logistics setup that makes shipping into the wider Middle East and North Africa a matter of trucking rather than international freight forwarding. For a heavy, fragile, high-volume commodity like processed architectural glass, those characteristics are not nice-to-have. They are deal-breakers.

In August 2022, the new Sejal management took the first formal step. The listed entity incorporated a Limited Liability Partnership called Sejal Glass Ventures LLP, in which it held a 99.99% economic interest.8 Four months later, on December 5, 2022, M/s Dilesh Roadlines Pvt. Ltd. — the promoter vehicle itself — was admitted as a partner in the LLP, reducing the listed company's share to 44.99% and converting the LLP into an associate rather than a subsidiary.8 On November 15, 2022, Sejal Glass Ventures LLP formed a wholly owned subsidiary in the UAE: Sejal Glass and Glass Manufacturing Products LLC, registered in Ras Al-Khaimah.8

The structural significance of these steps is easy to miss. By moving the UAE acquisition vehicle into a partnership structure where the listed entity was a minority partner and the promoter holding company was the majority partner, the new owners took a meaningful slice of the UAE upside onto their own balance sheets rather than channelling all of it through the listed company. This was, in capital allocation terms, a perfectly defensible move — the promoters were committing their own balance sheet to an unproven cross-border bet — but it was also a structural feature that minority shareholders of the listed entity would later need to factor into their assessment of how upside was being distributed.

Then came the deal itself. The UAE subsidiary acquired the assets of a distressed architectural glass manufacturer operating in Dubai and Ras Al-Khaimah for an estimated UAE Dirham 30 million, equivalent to approximately ₹70 crore, with additional working capital exposure on top.11 The acquired plant came with installed capacity, an existing customer book, and — crucially — the operational permits and supply relationships that would have taken years to build from a greenfield site. Management's stated estimate was that, at optimum capacity utilisation, the unit could produce a turnover of around AED 110 million, equivalent to roughly ₹250 crore.11 At the time of announcement, the unit already had an order book of around AED 35 million, or approximately ₹80 crore.11

This was the inflection point that turned Sejal from a small Indian processor into something else entirely. By the end of FY26, consolidated revenue from outside India had reached approximately ₹288 crore, against domestic revenue of approximately ₹108 crore — meaning the UAE subsidiary, between the date of the acquisition and the close of FY26, had grown to contribute the substantial majority of the consolidated top line.12 The roughly ₹70 crore of acquisition consideration had been put to work in a market where it was generating multiples of itself in annual revenue.

The strategic logic, in retrospect, looks almost too clean. Energy is the largest cost in a glass plant after raw float, and energy in the UAE is a fraction of the cost in industrial India. The GCC construction cycle, supercharged by Saudi Arabia's giga-projects and the perpetual commercial development engine in the UAE, generates demand for processed architectural glass at a scale and pace that India's stop-start commercial real estate market has historically struggled to match. Logistics from Ras Al-Khaimah into Saudi Arabia, Oman, Qatar, and East Africa are short and predictable. And the Indian listed-company structure provided the new owners with a low-cost, regulated capital pool — accessed through preferential allotments at progressively higher prices as the market caught on to the story — to fund expansion that, in a privately-held UAE LLC, would have required either expensive bank debt or a much earlier dilution.

If the Aarti-linked owners had simply restored a sub-scale Indian processor to break-even, they would have created a small, dull, slowly compounding niche company. By placing the centre of gravity of the operating business in the UAE, they created something with a fundamentally different ceiling. The "hidden" part of the growth engine was, in a literal sense, hidden — sitting outside India, denominated in dirhams, invisible to anyone reading only the Indian standalone numbers.

But a UAE-only growth story would have left the Indian business as a withering legacy operation. Management was not willing to accept that, and the next move would address it directly.

VII. The Domestic Rebound: The Glasstech Acquisition

By early 2025, the playbook was no longer a secret. Brokerage analysts who covered nano-cap and small-cap industrials had begun to map the Sejal story onto the standard Indian distressed-asset roll-up template: clean balance sheet, professional management with an established industrial pedigree, a high-margin export geography, and access to public-market capital at increasingly attractive prices. The question for management was not whether to expand the Indian business, but how. The two paths were the familiar ones — greenfield (build new capacity from scratch) or brownfield (buy somebody else's plant). For a management team whose own corporate origin was a court-supervised acquisition of a distressed asset, the choice was straightforward.

The target was glasstech Industries (India) Pvt. Ltd., a Maharashtra-headquartered processor whose architectural glass business operated out of two facilities — one at तलोजा Taloja, in the industrial belt outside Mumbai, and one at Erode in Tamil Nadu. On April 8, 2025, Sejal Glass's board approved a Business Transfer Agreement to acquire the architectural glass business of Glasstech via a slump sale, for a total cash consideration of ₹34.60 crore.13 The Business Transfer Agreement was executed on April 10, 2025, with the acquisition expected to close before the end of May 2025.13

The numbers tell the strategic story more eloquently than any press release. The acquired business had operating revenue of ₹63.74 crore in FY 2023-24.13 Sejal was therefore paying roughly half of one year's revenue, in cash, for a fully operational two-plant footprint that included not just the physical assets but also the technical know-how, brand, customer relationships, vendor relationships, and the operational employees needed to run it. In an industry where greenfielding equivalent capacity would have required significantly more capital and at least two years of construction and commissioning lead time, this was the textbook brownfield transaction.

The geographic logic of the two plants was equally pointed. Taloja sits inside the catchment area of the Mumbai Metropolitan Region, which by 2025 was experiencing one of its most aggressive commercial and high-end residential construction cycles in a decade. Erode, in the southern industrial belt of Tamil Nadu, gave Sejal a serviceable footprint in the entirely separate South Indian commercial construction market. From two factories, the company could now address most of urban India that mattered for premium architectural glass demand, without the cost or operational complexity of running a national-scale primary manufacturing operation.

What made the Glasstech acquisition particularly elegant was the way it complemented, rather than competed with, the UAE business. The UAE plant's primary export markets are the GCC and East Africa. The Indian plants' primary markets are domestic. There is essentially no overlap. The two operations share back-office functions, treasury, capital allocation discipline, and a procurement playbook on raw float glass — but they sell into completely different demand pools, which means cyclical downturns in one geography do not automatically infect the other. For a building-materials processor whose end-markets are notoriously cyclical, that diversification has real economic value.

The capacity roadmap that management had begun to articulate around the Glasstech transaction targeted consolidated revenue of roughly ₹400 crore in FY26.14 Given that the nine-month consolidated revenue for FY26 had already reached ₹284.51 crore against ₹177.05 crore in the prior period, the trajectory was on track to deliver, with full-year consolidated revenue ultimately landing in the vicinity of ₹400 crore on the back of continued execution at both UAE and Indian facilities.1415

This was, in capital-efficiency terms, an extraordinary outcome. A company that had been declared insolvent six years earlier had, on a fraction of the capital its predecessors had set on fire chasing float glass, rebuilt itself into a multi-geography processor with revenue approaching ₹400 crore — and it had done it largely by buying somebody else's distressed assets cheaply rather than by building its own from scratch. The pattern was the pattern. The new management knew how to buy distress, because they had been built out of distress themselves.

But who, exactly, was running this company day to day, and how were their incentives aligned with the people buying the shares?

VIII. Current Management & Incentive Structure

The board of directors of Sejal Glass, in its post-resolution configuration, is small, unflashy, and structured around two principals. The first is Surji Damji Chheda, who serves as Chairman.9 His public profile emphasises his four-decade career in direct taxation, audit, investments, and financial consultancy — not, notably, in glass manufacturing or in operating an industrial business at all.9 What he brings is something more strategically valuable to a roll-up of this kind: capital allocation discipline, financial structuring expertise, and access to the network of investors and lenders who back Aarti-adjacent ventures. He is the architect, not the foreman.

The second is Jiggar Lakshmichand Savla, who serves as Whole-time Director and is in practical terms the operational lead.9 His MBA in Marketing and his parallel executive role at Delicare Lifesciences Private Limited paint a picture of an operator who has been running businesses, including outside the glass industry, for years.9 In the day-to-day, it is Savla who fronts the earnings calls, talks to the brokerages, and interacts with customers and plant managers. The division of labour between Chheda's strategic-financial role and Savla's executive role is the kind of pairing that small-cap promoter teams either get exactly right or fatally wrong, and the operating results since 2022 suggest that this one is functioning.

The broader promoter group, as disclosed in the post-CIRP shareholding pattern, includes Ashwin S Shetty (also serving as Vice President & Company Secretary), Amruta Patanka, Surji D. Chheda, Jiggar L. Savla, Chirag H. Doshi, Neha Gada, and Vijay Mamania, with the substantive economic majority understood to sit between the Chheda group and the Aarti-linked Gogri group, holding a meaningful supermajority of the equity.1610

Skin-in-the-game is the structural feature that matters most here. In a small-cap industrial roll-up where the operational risk is real and the capital-allocation decisions compound for years, the question that every investor should ask first is: how much of their own personal net worth do the people running this company have at stake in the outcome? In Sejal's case, the answer is "most of it" — the promoter holding is substantial, and the entry into the company was made through fresh capital infusions at the new-resolution price, not at depressed legacy values. When this management makes a capital allocation decision, they are spending their own money first, and the decisions look that way.

The validation of that thesis from the broader Indian institutional ecosystem arrived in a series of capital raises through 2025 and into 2026. The company executed preferential allotments to selected investors — the structure most commonly used by Indian listed companies to raise growth capital from sophisticated investors who are willing to lock up shares for the regulatory minimum holding period — at progressively higher prices as the operating story validated. One key tranche allotted 13,00,000 equity shares at ₹555 per share, raising ₹72.15 crore.17 Across multiple preferential rounds in April 2025 and September 2025, the company raised in excess of ₹166 crore in fresh equity to fund the next leg of expansion, including the Glasstech acquisition and UAE capacity additions.17

The single most important name to surface on the post-allotment shareholding pattern was अबक्कस Abakkus Asset Manager, the firm founded and led by सुनील सिंघानिया Sunil Singhania — formerly the global head of equities at Reliance Mutual Fund and one of the most-followed value-oriented investors in the Indian market. Reporting tied to Singhania's Q4 disclosures indicated that Abakkus Growth Fund-2 had picked up 5,00,000 equity shares of Sejal Glass, equivalent to approximately 4.39% of the post-allotment capital, in the March 2026 quarter — a position valued at approximately ₹38.41 crore on a recent close.18

The presence of Singhania on a small-cap shareholder register is, for many domestic retail investors, a powerful validation signal. Whether or not one agrees that any single investor's presence should drive a fundamental decision, the institutional reality is that an Abakkus position acts as both a vote of conviction and a quasi-anchor that tends to attract subsequent allocations from other institutional pools. For Sejal, it crystallised a transition from "obscure post-CIRP small-cap" to "known small-cap with serious institutional backing," and the implications for cost of equity going forward are non-trivial.

With management and capital structure now intelligible, the question becomes whether the underlying business actually has durable competitive advantages — or whether this is a well-marketed cyclical without an economic moat.

IX. Playbook: Analysis & Hamilton's 7 Powers

To assess whether Sejal has built anything more than a temporarily fortunate cyclical position, it is worth running the business through a proper strategic framework rather than relying on the loose language of "moats" that pervades small-cap commentary. हैमिल्टन हेल्मर Hamilton Helmer's 7 Powers framework — Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power — is a useful diagnostic precisely because it forces specificity. Most companies that claim a moat have, on examination, none of the seven. Sejal probably has elements of two or three, depending on how strictly you draw the lines.

The clearest candidate is Cornered Resource. The Ras Al-Khaimah manufacturing campus, sitting inside a free-zone regulatory regime with subsidised energy, low corporate tax, and direct logistics access into the Saudi and broader GCC construction cycle, is not a structurally replicable position for an Indian competitor without a multi-year, hundreds-of-crores commitment of capital. Sejal got there first, at the bottom of the asset's distressed valuation, with a promoter group willing to underwrite the cross-border execution risk personally. A would-be Indian competitor today would be entering at higher land cost, higher entry-level dirham capex, and without the in-place customer relationships and operating permits that Sejal acquired with the asset. That is a cornered resource in the practical, operational sense — not a permanent moat, but a meaningful head start.

The second candidate is Process Power, in the disciplined-capital-allocation sense that the Aarti-linked promoters have brought into a fragmented, family-run industry. The Indian architectural glass processing industry is overwhelmingly populated by sub-scale, owner-operated workshops with limited financial discipline, opaque accounting, and chronic working-capital constraints. A processor that runs with the financial discipline of a publicly listed specialty chemicals company — tight DSO management, conservative leverage, capital allocated only to assets with clear unit-economics, brownfield expansion preferred over greenfield — competes against the long tail of regional fabricators with a structural cost-of-capital and reliability advantage. This is exactly the cultural transplant that makes the Aarti connection more than just a name on the cap table.

Scale Economies in the classical Helmer sense — where the largest player benefits from cost advantages that smaller competitors cannot match — apply only weakly at Sejal's current size. The company is regionally relevant in the UAE and is becoming relevant in two Indian metros, but it is not anywhere close to being the largest processor in either geography. The scale advantages it does enjoy are more modest: procurement leverage on raw float glass, the ability to spread fixed corporate overheads across a larger base, and a credit standing with banks that smaller competitors cannot match.

The other four Powers — Network Economies, Counter-Positioning, Switching Costs, and Branding — are essentially absent at the relevant scale. Glass processing has no network effects; nothing about being a Sejal customer makes you more likely to attract another Sejal customer. There is no Counter-Positioning move that an incumbent cannot replicate (Saint-Gobain, in particular, could in principle replicate any product positioning Sejal adopts). Switching costs for an architect or developer to swap one processor for another are low, particularly on price-sensitive volume work. And while the legacy "Sejal" brand carries some residual recognition among older Indian architects, it does not command a meaningful price premium over equivalent products from other processors.

Layering on Michael Porter's classic Five Forces gives a more complete picture. The Bargaining Power of Suppliers — primarily the float glass primary manufacturers — is meaningful but not crippling, because float glass is a globally traded commodity with multiple supply origins. The Bargaining Power of Buyers varies sharply by segment: low for high-end, specification-driven architectural projects where the architect chooses Sejal because of the quality and service profile, but materially higher for commodity volume work where developers will switch for a small price advantage. The Threat of New Entrants is moderate — the capital required to set up a meaningful processing operation is real but not prohibitive, particularly given the existence of distressed assets that can be bought cheaply, as Sejal itself demonstrated. The Threat of Substitutes for architectural glass in modern building facades is genuinely low — glass remains the dominant material for fenestration and curtain walls in Grade A construction worldwide, with no credible substitute on the horizon. Industry Rivalry, finally, is the single biggest risk factor — fragmented, cyclical, with periodic episodes of brutal price competition during downturns.

The honest synthesis, then, is that Sejal is a cyclical processor with two genuine but limited Powers (Cornered Resource in the UAE, Process Power from the Aarti-style discipline) operating in an industry whose secular tailwind is real but whose competitive intensity is also real. The question for any long-term holder is whether the management team can compound those two limited Powers into something more durable through continued execution — and that is, ultimately, an empirical question that the next three to five years of operating results will answer.

X. Bear vs. Bull Case

The bull case for Sejal Glass writes itself almost too easily, which is itself a warning sign. The narrative beats are perfect: a phoenix story emerging from the ashes of NCLT, a hidden multinational operating subsidiary that domestic small-cap screeners did not initially pick up, a management team with industrial pedigree that traces back to one of India's most respected business families, and a tier-one institutional investor crystallising on the cap table to validate the thesis. Add in the structural deleveraging from the post-CIRP balance sheet reset, the operating leverage that comes from running newly acquired plants through their utilisation curve, and the secular tailwind of GCC and Indian commercial construction, and you have a story that is genuinely difficult to argue against on a five-year horizon.

The bear case is more textured and worth taking seriously. The single biggest risk is cyclicality. Architectural glass is a derivative of commercial real estate development cycles, and commercial real estate development cycles in both India and the GCC are notoriously prone to sharp downturns triggered by interest rate shocks, oil price collapses, or geopolitical disruption. In a material downturn, the operating leverage that works for Sejal on the way up will work just as relentlessly against it on the way down. A processor running its plants at 90% utilisation generates excellent margins; the same processor running at 60% utilisation can rapidly slide into operating losses, particularly in a price-cutting environment.

The second risk is execution at the new Indian plants. Buying distressed brownfield assets cheaply is the easy part. Integrating them, running them at the utilisation needed to justify the acquisition multiple, retaining the customer book through the ownership transition, and executing the synergies with the existing operations is the hard part. Indian industrial M&A is full of acquisitions that looked elegant on the term sheet and disappointing on the integration. Sejal's management appears competent, but the Glasstech integration is, as of mid-2026, an unproven execution outcome.

The third risk is energy and raw material price volatility. Float glass is one of the most natural-gas-intensive industrial inputs in the building products complex, and raw float prices globally have a strong correlation to natural gas prices. A spike in either input — driven by Middle East geopolitics, a surge in Chinese construction activity, or a tightening of LNG markets — can compress processor margins meaningfully before the processor has time to pass the cost increase through to customers. Sejal has limited natural hedge against this risk.

The fourth risk is concentration. The fact that approximately 73% of consolidated revenue in FY26 came from outside India is an opportunity, but it is also a concentration in a single foreign market and political jurisdiction.12 A material change in UAE labour policy, a slowdown in Saudi giga-project execution, or a regional security event could affect the UAE subsidiary's revenue trajectory in ways that the listed entity in Mumbai cannot easily compensate for.

The fifth risk is governance complexity. The structural feature of housing the UAE operation through a partnership in which the listed company holds 44.99% rather than 100% is a structure that minority shareholders need to keep an eye on. It is not, on its face, abusive — the promoter group put its own balance sheet at risk first to acquire the UAE asset, and the listed company is the substantive economic beneficiary. But it is the kind of structural feature that requires ongoing attention as the UAE business compounds, because the value-distribution between the listed entity and the promoter holding company is not as straightforward as a 100% subsidiary structure would be.

The KPIs that matter for tracking ongoing performance are narrow and specific. The first is consolidated revenue trajectory and its geographic mix — whether the UAE business continues to grow as a proportion of consolidated revenue or whether the Indian business begins to catch up, both of which would tell different stories about strategic execution. The second is consolidated EBITDA margin — particularly whether the company can sustain mid-teens operating margins as scale grows, or whether competitive pressure compresses them back toward single digits. And the third is the net debt to EBITDA ratio — the single best summary statistic for whether management has stayed disciplined on the leverage that destroyed the previous incarnation of the company. Two of those three metrics are easily computed from quarterly disclosures, and one — geographic mix — typically requires reading the segment reporting in the annual report, which makes it the metric most likely to be missed by passive screeners.

Comparing Sejal to its industry peers is almost an exercise in genre confusion. The closest large-cap analogues — सेंट-गोबेन Saint-Gobain India, asahi इंडिया Asahi India Glass — are integrated giants with float glass primary manufacturing, automotive glass exposure, and distribution networks of a different order of magnitude. Sejal does not compete with them at scale; it competes with the long tail of regional processors in India and the equivalent fragmented competitive set in the UAE. The right peer comparison is not "is Sejal cheaper than Asahi," but "is Sejal building a structurally better mid-market processor than the dozens of family-run shops it competes against day-to-day." The early evidence suggests yes, but the verdict will take years.

The myth versus reality test on this story, finally, is worth running. The consensus narrative — that Sejal is a clean phoenix, professionally rebuilt, with predictable upside — is essentially correct on the facts but understates how cyclical the underlying industry is and how much execution risk remains in the Indian rebuild. The deeper reality is that this is a highly capable management team executing competently in a structurally tough industry, having taken advantage of two specific dislocations (the IBC restructuring and a UAE distressed sale) to assemble an unusually attractive cost basis. Whether the next ten years compound that initial advantage into something durable is the real question, and the answer will depend less on the macro tailwind than on the operational discipline of the people who showed up in that NCLT courtroom in 2021 with a plan.

XI. Epilogue & Lessons

The most enduring lesson from the Sejal Glass story is not actually about glass. It is about the architecture of how productive industrial assets get reallocated across owners in an economy that has finally built a working insolvency mechanism. For most of independent India's history, the only outcomes for a company in the position that Sejal occupied in 2018 were prolonged zombification under the old debt-recovery regime, or eventual fire-sale liquidation that destroyed both the operating asset and most of the surrounding employment. The IBC, for all its imperfections and the haircuts it has imposed on lenders, has changed that. It has created a path under which a productive operating asset can be cleanly separated from an unmanageable debt stack, transferred to a competent new operator, and given a second life under disciplined ownership.

Sejal is, in microcosm, what that mechanism is supposed to deliver. The original promoter group built something real, made one decision too many, and lost control of it. The new promoter group bought the residual chassis at a price that reflected the distress, brought capital and management discipline that the old owners had run out of, and executed a strategy — UAE pivot first, then Indian brownfield consolidation — that was fundamentally unavailable to the previous custodians. The system worked the way it was designed to work. That is rarer in Indian corporate history than it should be.

The second lesson is about hidden geography. Indian small-cap investors are conditioned to look at standalone Indian numbers, because for most of the universe that is where the substance of the business lives. A company whose centre of operating gravity sits in another jurisdiction altogether, accessed through a partnership structure and reported in consolidated dirham-converted figures, is the kind of structural fact that the standard small-cap screener will miss until the market has already partially repriced the story. The Sejal repricing, accelerating through 2025 and into 2026, was substantially the market belatedly noticing what the consolidated segment data had been saying for two years — that this is not really an Indian processor anymore.

The third lesson is the one most likely to get repeated in coming years across other small-cap Indian industrial restructurings. The combination of (a) clean post-CIRP balance sheet, (b) capable promoter ecosystem with industrial pedigree, (c) low-cost cross-border manufacturing access, and (d) Indian listed-company status providing repeated access to public-market growth capital is a structurally powerful template. Sejal will not be the last small-cap Indian industrial to execute on that template. It is, at the moment of writing, one of the most fully-formed examples of it.

What ultimately distinguishes the Chheda-Savla era from the Gada era is not access to capital, or access to markets, or access to technology. The Gadas had all of those things in 2008 — they raised IPO money, they had customer relationships, and they bought best-in-class float glass technology from international vendors. What they did not have was a disciplined framework for distinguishing between bets they could afford to lose and bets they could not. The float glass plant was the latter, and they took it anyway. The current management's decisions have, so far, been characterised by a different temperament — the willingness to buy distressed brownfield rather than build expensive greenfield, the willingness to put promoter balance sheet at risk first before listed-company balance sheet, and the willingness to compound slowly rather than swing for the fences.

In a small-cap universe full of stories with bigger headline TAMs and louder press releases, that temperament may turn out to be the most undervalued thing about Sejal Glass. The phoenix, after all, did not rise because it was reborn. It rose because somebody, this time, knew not to fly too close to the sun.

References

References

-

SEJALLTD Share Price Live: Sejal Glass NSE Today — Tickertape ↩

-

Sejal Glass Limited Reports Strong Financial Performance for FY26 with 62.73% Revenue Growth — IndiaIPO/ScanX ↩

-

SEJAL GLASS LIMITED Brief Profile of Directors — Sejal Glass ↩

-

Sejal Architectural Glass IPO Date, Price, GMP, Details — Chittorgarh ↩↩

-

Saint-Gobain announces the acquisition of Sezal Glass Ltd's float glass business in India — Saint-Gobain, 2011-05 ↩↩

-

Saint-Gobain Glass: Best Glass Manufacturing Company in India — Saint-Gobain India ↩

-

SEJAL GLASS LIMITED Brief Profile of Directors — Sejal Glass ↩↩↩↩↩↩

-

Who are in the management team of Sejal Glass? — MarketsMojo ↩↩↩

-

Sejal Glass announces Overseas Acquisition — EquityBulls / Sejal Glass press release ↩↩↩

-

Sejal Glass FY26: ₹29 Cr Profit Despite Standalone Business Loss — Whalesbook Corporate News ↩↩

-

Sejal Glass to Acquire Glasstech India's Architectural Glass Business — Bullu, 2025-04-08 ↩↩↩

-

Sejal Glass Targets ₹400 Cr FY26 Revenue; New Products Drive Growth — Whalesbook ↩↩

-

Sejal Glass Limited Hosts Q3 FY26 Earnings Conference Call, Reports Nine Months Revenue of INR 284.51 Crores — ScanX ↩

-

Sejal Glass Secures NSE, BSE Trading Nod for Preferential Share Allotment — TipRanks ↩↩

-

Sunil Singhania picked up 6 new stocks in the March 2026 quarter — Business Today, 2026-04-26 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube