Adobe: The Creative Cloud's Reign and the Battle for Design's Future

I. Introduction & Episode Setup

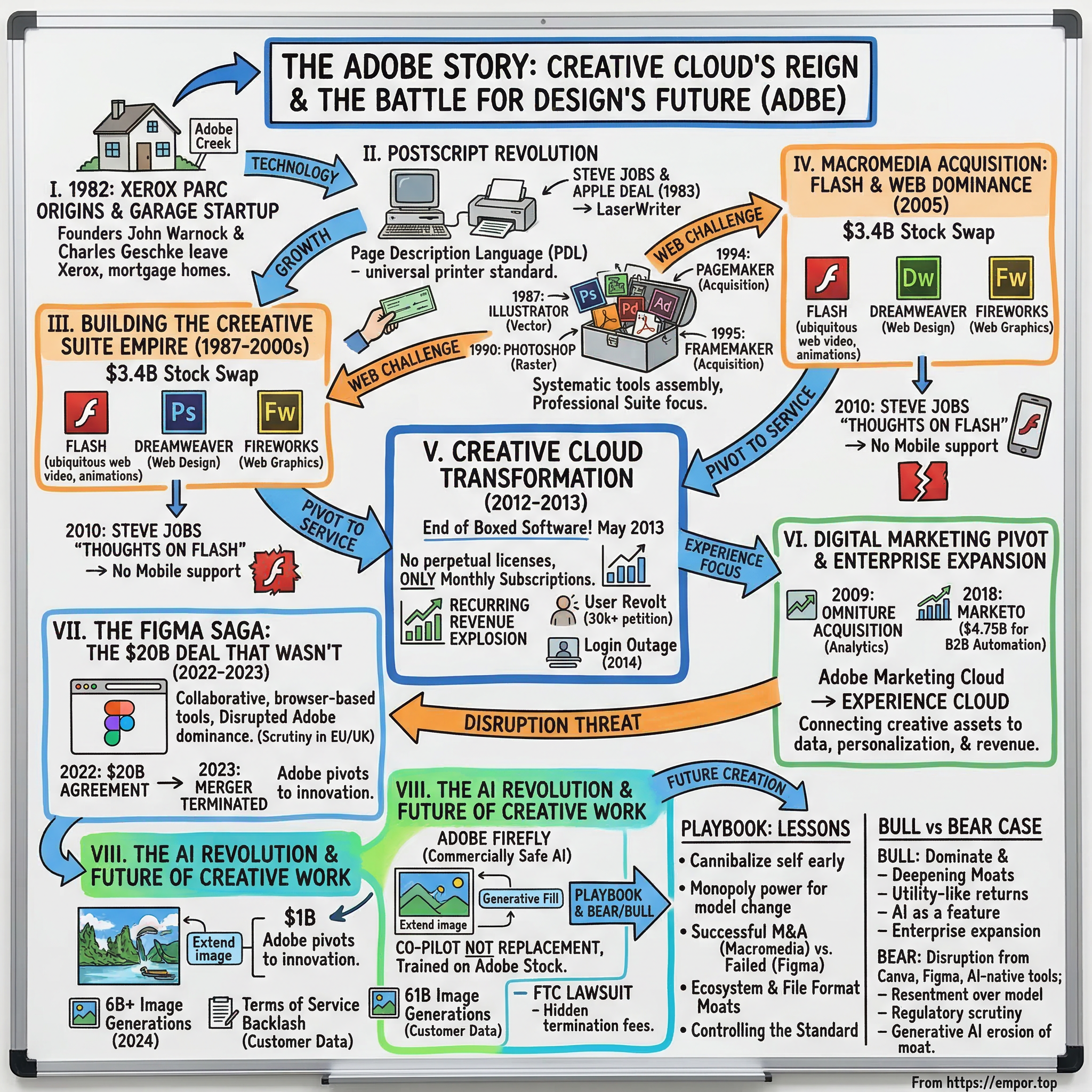

Picture this: December 1982, a modest garage in Los Altos, California. Two middle-aged engineers, John Warnock and Charles Geschke, are hunched over computers, having just walked away from the prestigious Xerox PARC—the birthplace of the graphical user interface, Ethernet, and laser printing. They've mortgaged their homes, convinced their wives to support one more startup dream, and named their company after the creek that ran behind Warnock's house: Adobe Creek.

What they're building seems almost absurdly technical—a page description language called PostScript that tells printers how to render fonts and graphics. Yet within months, a young Steve Jobs will show up at their door with a $2.5 million check, desperate to license their technology. Within five years, they'll have revolutionized publishing. Within forty, they'll control the creative software that powers nearly every image, video, and design you encounter daily.

How did two Xerox engineers build the company that would define creative software for four decades? How did Adobe survive the death of print, the rise of the web, the mobile revolution, and now position itself for the AI era? And what can we learn from their transformation from a printer language company to a $200+ billion creative cloud empire?

This is the story of technical excellence meeting artistic expression, of platform transitions executed flawlessly and others bungled spectacularly. It's about the audacity to tell millions of creative professionals in 2013 that they could no longer buy software—only rent it—and somehow making it work. It's about a $20 billion acquisition that collapsed under regulatory scrutiny and what that means for the future of creative tools.

We'll explore the PostScript revolution that created desktop publishing, the building of the Creative Suite empire that conquered professional design, the controversial shift to Creative Cloud that transformed Adobe's business model, and the ongoing battle for the future of creative work in an AI-powered, collaboration-first world. Along the way, we'll unpack the business lessons: how to navigate platform shifts, when acquisitions work (Macromedia) versus when they don't (Figma), and what Adobe's journey teaches us about building enduring software franchises.

II. The Xerox PARC Origins & PostScript Revolution

The fluorescent lights of Xerox PARC hummed overhead as John Warnock stared at his computer screen in frustration. It was 1978, and he'd just spent months developing Interpress, a revolutionary language that could describe complex page layouts to any printer. The technology was groundbreaking—it could render fonts at any size without pixelation, handle complex graphics, and work across different devices. But Xerox executives in Connecticut saw it differently. "Too complicated," they said. "Our customers just want to make copies."

Warnock and his colleague Charles Geschke had both come to PARC with impressive credentials. Warnock held a PhD in computer science from the University of Utah, where he'd studied under graphics pioneer Ivan Sutherland. Geschke had earned his doctorate from Carnegie Mellon, specializing in compiler design. At PARC, they'd witnessed the future—graphical interfaces, laser printers, networked computers—but watched helplessly as Xerox failed to commercialize nearly every breakthrough.

The breaking point came in 1982. After Xerox killed yet another attempt to bring their page description technology to market, Warnock and Geschke made a decision that would reshape the technology industry. At ages 41 and 43 respectively—ancient by Silicon Valley startup standards—they quit their secure jobs to start Adobe Systems. The name came from Adobe Creek, which ran behind Warnock's Los Altos home, but the ambition was anything but provincial.

Their timing seemed terrible. The early 1980s personal computer market was fragmented chaos—Apple IIs, IBM PCs, dozens of incompatible systems, each with different printers that couldn't talk to each other. But where others saw confusion, Warnock and Geschke saw opportunity. They refined their page description language into PostScript, a universal translator that could describe any page layout in mathematical terms that any PostScript-enabled printer could understand.

The technical elegance was beautiful—PostScript was a full programming language, Turing-complete, stack-based, inspired by Forth. But selling it proved challenging. Printer manufacturers balked at the licensing fees. Computer makers didn't see the point. Adobe burned through cash, and by late 1983, they were running on fumes.

Then Steve Jobs walked through the door.

Fresh off the Macintosh project, Jobs was obsessed with typography and publishing. He'd famously audited calligraphy classes at Reed College and built multiple fonts into the Mac. But the Mac's dot-matrix ImageWriter printer produced output that looked, frankly, terrible. When Jobs saw PostScript render smooth, professional-quality type on a laser printer, he immediately grasped its potential. The real story was even more dramatic than the simplified version. Jobs initially offered $5 million to buy Adobe outright in 1982, but Warnock and Geschke refused. The founders' investors at Hambrecht & Quist were furious—here was the hottest entrepreneur in Silicon Valley wanting to acquire their startup, and the founders were saying no?

But Warnock and Geschke held firm. They believed PostScript could be bigger than just an Apple technology. After intense negotiations, they reached a compromise that would prove brilliant for both sides: Adobe agreed to sell Jobs shares worth 19 percent of the company, with Jobs paying a five-times multiple of their company's valuation at the time, plus a five-year license fee for PostScript, in advance.

The deal terms were extraordinary. Apple invested $2.5 million in Adobe for a 15% stake in the company, plus the prepaid licensing fees. For Adobe, this meant instant profitability—they became the first company in Silicon Valley history to be profitable in their first year of operations. For Apple, it meant exclusive access to the technology that would enable the LaserWriter.

In 1985, Apple Computer licensed PostScript for use in its LaserWriter printers, which helped spark the desktop publishing revolution. The LaserWriter, priced at $6,995, was expensive but revolutionary. Combined with Aldus PageMaker software and the Macintosh's graphical interface, it created an entirely new industry: desktop publishing. Suddenly, small businesses, newspapers, and design firms could produce professional-quality documents in-house. The printing industry, unchanged for centuries, transformed overnight.

By 1987, PostScript had become the industry-standard printer language with more than 400 third-party software programs and licensing agreements with 19 printer companies. Adobe's gamble on mathematical elegance over proprietary lock-in had paid off spectacularly. They'd created not just a product but a platform, a standard that competitors had to adopt or die.

The relationship between Adobe and Apple would prove complex over the decades—sometimes partners, sometimes rivals, always intertwined. But in that moment in 1983, when Jobs walked into Adobe's offices with his reality distortion field at full power, the founders' decision to maintain independence while partnering strategically set the template for Adobe's next four decades: technical excellence, strategic partnerships, and always, always, control of their own destiny.

III. Building the Creative Suite Empire (1987–2000s)

The conference room at Adobe headquarters fell silent as John Warnock unveiled a demo that would change graphic design forever. It was 1987, and he was showing Adobe Illustrator—software that could draw smooth Bézier curves that scaled infinitely without pixelation. An artist in the audience actually gasped. For the first time, designers could create logos and illustrations on a computer that matched the precision of hand-drawn technical illustrations.

Adobe entered the consumer software market in the mid-1980s with Adobe Illustrator, a vector-based drawing program for the Apple Macintosh that grew out of the firm's in-house font-development software and helped popularize PostScript-enabled laser printers. The timing was perfect—the desktop publishing revolution Adobe had helped create was hungry for professional design tools.

But Illustrator was just the opening act. The real revolution came three years later when Adobe made a acquisition that would define its future. Brothers Thomas and John Knoll had developed a program called Display to showcase grayscale images on a black-and-white monitor. Thomas, a PhD student at the University of Michigan, kept adding features—color editing, file format conversions, image filters. His brother John, working at Industrial Light & Magic, saw the potential immediately. In September 1988, Adobe decided to purchase the license to distribute Photoshop. In September 1988 Adobe decided to purchase the license to distribute. The initial acquisition was modest—Adobe acquired the software from the Knoll brothers for an estimated $300,000. But Adobe's timing was perfect. The list price of Photoshop 1.0 for Macintosh in 1990 was $895, positioning it as professional software accessible to serious enthusiasts.

Photoshop 1.0 was released in February 1990, and it transformed creative work overnight. When Photoshop 1.0 was released, digital retouching on dedicated high-end systems (such as the Scitex) cost around $300 an hour for basic photo retouching. Suddenly, that same work could be done on a Macintosh for less than a thousand dollars.

The real genius of Adobe's approach was understanding that creative professionals didn't just need one tool—they needed a suite. As Photoshop gained traction, Adobe systematically built and acquired complementary products. In 1993, they introduced the Portable Document Format (PDF) and Adobe Acrobat, with Warnock originally developing PDF under the code name "The Camelot Project. "The strategic acquisitions began accelerating. In September 1994, Adobe purchased Aldus for $446 million. The acquisition brought Adobe PageMaker, the software that had literally created desktop publishing alongside the Mac and LaserWriter. But PageMaker was already losing ground to QuarkXPress, and Adobe knew it. They got something more valuable: a foothold in professional publishing and a team that understood print workflows intimately.

In October 1995, Adobe acquired the desktop publishing software company Frame Technology for US$566 million, adding FrameMaker for technical documentation. These weren't random shopping sprees—Adobe was systematically assembling the tools that creative professionals needed for their entire workflow.

The real turning point came with Adobe's initial public offering in 1986. Adobe entered the NASDAQ Composite index in August 1986. By 1990, revenues had grown to $168.7 million, but success brought challenges. Apple, Adobe's most important partner, began to chafe at PostScript licensing fees. In 1989, Apple announced plans to sell its Adobe stock, collaborate with Microsoft on a PostScript clone, and introduce its own font technology called TrueType.

The "font wars" that followed could have destroyed Adobe. Microsoft and Apple, the two titans of personal computing, were essentially declaring war on Adobe's core business. But Adobe responded with technical brilliance and strategic patience. They developed their own TrueType competitor and weathered the storm. By 1991, Apple and Adobe reached a détente, with both companies realizing they needed each other more than they needed to fight.

Then came a moment that showed how personal the tech industry could be. In June 1992, Adobe President and CEO Charles Geschke was kidnapped at gunpoint from the Adobe parking lot. For five days, the tech world held its breath as the FBI worked to secure his release. When Geschke was finally freed unharmed, Adobe employees wept with relief. The incident reminded everyone that behind the software and stock prices were real people building something they believed in.

Meanwhile, John Warnock was cooking up something revolutionary in his lab. Under the code name "The Camelot Project," he was developing a way to capture documents electronically—preserving fonts, images, and layout exactly as intended, viewable on any computer. In 1993, Adobe introduced the Portable Document Format, commonly shortened to the initialism PDF, and its Adobe Acrobat and Reader software.

PDF seemed like a small innovation at first—just another file format in a world drowning in incompatible standards. But Warnock had a vision: "Imagine being able to send full text and graphics documents (newspapers, magazine articles, technical manuals etc.) over electronic mail distribution networks. These documents could be viewed on any machine and any selected document could be printed locally. This capability would truly change the way information is managed."

He was right, of course. PDF would become as fundamental to digital documents as PostScript had been to printing. But that success was still years away. For now, Adobe was building its empire one creative tool at a time, transforming from a printer language company into the creative professional's Swiss Army knife.

On March 31, 1995, Adobe purchased the rights for Photoshop from Thomas and John Knoll for $34.5 million so Adobe would no longer need to pay a royalty for each copy sold—a deal that would prove to be one of the greatest bargains in software history as Photoshop went on to generate billions in revenue.

By the turn of the millennium, Adobe had assembled an impressive portfolio: Photoshop for image editing, Illustrator for vector graphics, PageMaker (later InDesign) for layout, Premiere for video editing, After Effects for motion graphics, and Acrobat for document management. Each product was strong individually, but together they formed something more powerful—an ecosystem where creative professionals could start a project in one application and seamlessly move it to another. The Creative Suite empire was taking shape, setting the stage for Adobe's next transformation.

IV. The Macromedia Acquisition: Flash & Web Dominance (2005)

Bruce Chizen sat in Adobe's boardroom, staring at a single slide showing MySpace pages covered in Flash animations, YouTube's video player powered by Flash, and statistics showing that 98% of internet-enabled desktops had Flash Player installed. It was early 2005, and Adobe's CEO knew his company faced an existential choice: stay focused on print and static graphics while the world moved online, or make the biggest acquisition in the company's history.

Across the valley, Macromedia was riding high on the web revolution. Their Flash platform had become the de facto standard for rich internet applications, animations, and video. Dreamweaver dominated web design. Fireworks challenged Photoshop in web graphics. But beneath the success, Macromedia was struggling—generating only about $40 million annually in net income on $442 million in revenue. They had the technology for the future but lacked the resources to fully capitalize on it. On April 18, 2005, Adobe Systems announced an agreement to acquire Macromedia in a stock swap valued at approximately $3.4 billion on the last trading day before the announcement. The acquisition took place on December 3, 2005, and Adobe integrated the company's operations, networks, and customer care organizations shortly thereafter.

The strategic rationale seemed bulletproof. By 2005, more computers worldwide had the Flash Player installed than any other Web media format, including Java, QuickTime, RealNetworks, and Windows Media Player. Flash wasn't just popular—it was ubiquitous, installed on 98% of internet-enabled desktops. YouTube's video player ran on Flash. MySpace pages danced with Flash animations. Online games, from simple puzzles to complex multiplayer experiences, were built in Flash.

But the integration proved more challenging than anyone anticipated. Adobe and Macromedia had fundamentally different cultures. Adobe was methodical, focused on professional tools with long development cycles. Macromedia was scrappy, web-focused, iterating quickly. The Dreamweaver team clashed with the GoLive team. Flash developers felt marginalized within Adobe's print-centric organization.

The most catastrophic mistake came early. After the acquisition, Adobe had laid off all members of the original mobile business unit from Macromedia that had spearheaded Flash Lite's success in Japan. This team had built a $1 billion market for Flash content on Japanese mobile phones. Their dismissal would prove fatal when mobile became the next battlefield.

Adobe's vision for Flash was ambitious—they wanted to transform it from a web animation tool into a full application platform. Flash Player 6.0 had already moved in this direction, adding enhanced audio, video, and user interface capabilities. ActionScript 3.0, introduced in Flash CS3 Professional in 2007, brought modern programming practices. Adobe AIR let developers build desktop applications with Flash. For a moment, it seemed like Flash might become the universal runtime for rich applications across all platforms.

But storm clouds were gathering. Security vulnerabilities plagued Flash, with new exploits discovered monthly. The software was a resource hog, draining laptop batteries and making fans spin like jet engines. Web standards advocates criticized Flash as proprietary technology that broke the open web. And most importantly, a new computing platform was emerging where Flash had no foothold: mobile.

The death blow came from an unexpected source. On April 29, 2010, Steve Jobs published an open letter titled "Thoughts on Flash." In just 1,685 words, he systematically demolished Flash's reputation. Jobs skewered its security ("Flash is the number one reason Macs crash"), reliability ("Flash has not performed well on mobile devices"), and performance ("Flash performs too poorly on mobile to be useful").

The letter was devastating not just for what it said, but for what it meant. Apple's iPhone and iPad were the future of computing, and Flash was explicitly banned from them. Developers who had invested years mastering ActionScript suddenly found their skills obsolete. Companies that had built their entire web presence on Flash scrambled to rebuild in HTML5.

Adobe fought back initially. Kevin Lynch, Adobe's CTO, even participated in a parody video destroying an iPhone. But privately, Adobe executives knew Jobs was right about Flash's mobile performance. The technology that had been designed for desktop computers with consistent power and large screens simply couldn't adapt to the battery-constrained, touch-based world of smartphones.

By 2011, Adobe surrendered. They announced Flash Player would no longer be developed for mobile browsers. In 2015, they rebranded Flash Professional as Adobe Animate, signaling a shift toward HTML5. And in July 2017, Adobe announced Flash's end of life—support would officially end on December 31, 2020.

The Macromedia acquisition ultimately brought Adobe valuable assets—Dreamweaver remained popular with web developers, Fireworks found a niche with web designers, and the engineering talent helped Adobe build Creative Cloud. But Flash, the crown jewel of the deal, became a cautionary tale about platform transitions and the danger of proprietary technologies in an open-standards world.

At the time of the sale, Macromedia was only generating about $40 million a year in net income, on $422 million in revenue. It would have taken large amounts of cost-cutting, synergies and time to make back $3.4 billion on that sort of financial performance. Whether Adobe ever recouped its investment remains debatable. But the acquisition taught Adobe crucial lessons about web technologies, platform transitions, and the importance of standards—lessons that would prove invaluable in their next transformation.

V. The Creative Cloud Transformation (2012–2013)

The atmosphere in Adobe's San Jose headquarters was electric with tension on May 6, 2013. CEO Shantanu Narayen was about to announce the most controversial decision in the company's 30-year history. No more boxed software. No more perpetual licenses. From now on, if you wanted the latest version of Photoshop, Illustrator, or any Adobe creative tool, you had to pay monthly. Forever.

The internal debates had been fierce. Sales executives warned of customer revolt. Engineers worried about reliability—what if the authentication servers went down? The finance team ran model after model, trying to predict how many customers they'd lose versus the recurring revenue they'd gain. One senior executive reportedly stood up in a meeting and said, "This could destroy the company."

But Narayen and his team saw no alternative. The traditional software model was dying. Adobe Creative Suite 6, released in 2012, had strong initial sales, but revenue dropped off a cliff after the first few months. Customers would buy CS6 and use it for years, maybe decades. Meanwhile, Adobe had to keep paying engineers, developing features that only a fraction of users would ever pay to access.

The math of the subscription model was seductive. Instead of $2,600 for the Creative Suite Master Collection—a price that made even professionals wince—customers could pay $50 per month. For students, it was just $20. The lower entry point would expand the market. The predictable revenue would let Adobe invest more in development. And critically, piracy would become much harder when software required monthly authentication. The announcement came on May 6, 2013, at Adobe's MAX conference in Los Angeles. On May 6, 2013, Adobe announced that they would not release new versions of the Creative Suite and that future versions of its software would be available only through the Creative Cloud. The reaction was immediate and visceral.

Within hours, a Change.org petition demanding Adobe reverse course gathered momentum. Among these was a Change.org petition which reached over 30,000 signatures within a few weeks of the announcement. Forums exploded with outrage. Professional photographers worried about losing access to their tools if they couldn't pay. Designers in developing countries pointed out that $50 per month was a fortune in their economies. Government agencies and educational institutions that couldn't use cloud services faced being frozen out entirely.

The criticism wasn't just about price—it was about control. If subscribers cancel or stop paying, they will lose access to the software as well as the ability to open work saved in proprietary file formats. Your entire professional archive, decades of work, could become inaccessible if you missed a payment or Adobe changed its terms.

But Adobe had done its homework. They knew the initial reaction would be brutal. What they also knew was that their core professional users—the studios, agencies, and freelancers who made their living with Adobe tools—had no real alternative. In a mid-June MacWorld article, Adobe reported a total of 700,000 subscribers, and expected to reach their target of 1.25 million subscribers by the end of 2013.

The transition wasn't without disasters. In May 2014 the service was interrupted for over a day due to a login outage leaving graphics professionals locked out of Creative Cloud. Adobe apologized for this global Creative Cloud failure. Professionals on deadline couldn't access their tools. The incident validated every fear about subscription software—what happens when the authentication servers fail?

The piracy question proved equally complex. Adobe had hoped subscriptions would curtail the rampant piracy of Photoshop, one of the most pirated pieces of software in history. But as a solution for piracy, the jury is still out; one day after the official release of Creative Cloud, a torrent link to a pirated copy was uploaded to The Pirate Bay. Within 24 hours of Creative Cloud's launch, cracked versions appeared online.

Yet something unexpected happened. Despite the outcry, despite the petitions, despite the availability of pirated versions, Creative Cloud began to succeed. The lower monthly price brought in customers who could never afford the upfront cost. Students flocked to the discounted plans. Small studios that previously shared licenses could now afford individual subscriptions.

The financial transformation was stunning. Adobe's recurring revenue exploded. Stock price soared from around $40 in 2013 to over $150 by 2015. Wall Street, initially skeptical, became believers. The predictable revenue stream let Adobe invest heavily in product development. Features that would have waited years for a major release now shipped monthly.

Since it introduced the service last year, Adobe added more than half a million paying Creative Cloud subscribers and two million users who subscribe to its free services. As Adobe's David Wadhwani noted in today's keynote, there is no doubt in his mind that Creative Cloud is the right direction for the company.

The subscription model also changed Adobe's relationship with customers. Instead of massive upgrades every 18-24 months that customers might skip, Adobe shipped continuous improvements. Because the software is now cloud-based, updates and patches will occur more regularly. This is probably one of the greatest advantages to Adobe's subscription service. Instead of waiting for the next cycle of software to get new technology, we'll have access to it the moment it becomes available.

For power users, the value proposition improved over time. Adobe loses money on power users who upgrade every cycle — every new master collection costs $2,500. But Adobe now makes more from the average user who previously used an older version for years or who didn't buy the master collection at all. Access to the entire suite for $50 per month was actually cheaper than buying regular upgrades.

But the transformation went deeper than pricing. Creative Cloud forced Adobe to become a services company. They added cloud storage, font libraries through Typekit, portfolio hosting via Behance, and collaboration tools. The software became just one part of a broader creative ecosystem.

The lessons were profound. First, if you have enough market power and your product is essential enough, you can force even the most reluctant customers through a painful transition. Second, the vocal minority online doesn't always represent the silent majority's behavior. Third, recurring revenue changes everything—it provides stability that enables long-term investment and risk-taking.

By 2015, it was clear the gamble had paid off. Creative Cloud had over 6 million subscribers. Adobe's market cap had doubled. The company that had been vulnerable to every platform shift was now insulated by predictable, recurring revenue. They'd successfully transitioned from selling software to selling an ongoing relationship with creative professionals.

The subscription model would become the template for the entire software industry. Microsoft followed with Office 365. Autodesk moved its CAD tools to subscription. Even Apple launched subscription services. Adobe didn't just change its own business model—it changed how all software was sold. The Creative Cloud transformation proved that with enough conviction and market power, you could completely rewrite the rules of your industry.

VI. The Digital Marketing Pivot & Enterprise Expansion

The conference room at Adobe's San Jose headquarters hummed with nervous energy in September 2009. CEO Shantanu Narayen was presenting a radical vision to his board: Adobe, the company that had built its empire on creative tools, would become a digital marketing powerhouse. The directors exchanged skeptical glances. How could a company known for Photoshop and PDFs compete with Salesforce, Oracle, and IBM in enterprise software?

Narayen pulled up a slide showing the digital advertising market's explosive growth. "Every creative asset our customers make eventually becomes marketing content," he explained. "We own the creation. Why shouldn't we own the distribution, measurement, and optimization?"

The strategy had been percolating since 2008 when Adobe quietly acquired Omniture for $1.8 billion—a price that made even Adobe bulls wince. Omniture's web analytics competed directly with Google Analytics, and many questioned why Adobe would pay such a premium for a company generating just $300 million in annual revenue.

But Narayen saw what others missed. The future of marketing wasn't just about creating beautiful ads—it was about data, personalization, and real-time optimization. Every click, scroll, and conversion was a data point. The companies that could connect creative assets to business outcomes would own the future of marketing. The Omniture acquisition proved to be just the beginning. Now generating hundreds of millions of dollars per quarter, it became the foundation of Adobe's marketing cloud, and has likely already paid for itself. By 2015, Marketing Cloud was on track to generate $1.35 billion in revenue.

But the real power move came in September 2018. Adobe announced it has entered into a definitive agreement to acquire Marketo, the market-leading cloud platform for B2B marketing engagement, for $4.75 billion. The price tag raised eyebrows—Vista Equity Partners had bought Marketo just two years earlier for $1.8 billion. Adobe was paying nearly triple that amount.

The Marketo acquisition was transformative for several reasons. First, it gave Adobe instant credibility in B2B marketing automation, a space where they'd been notably absent. With nearly 5,000 customers, Marketo brings together planning, engagement and measurement capabilities into an integrated B2B marketing platform. Second, it provided a new customer base to cross-sell Adobe's entire Experience Cloud. Third, it positioned Adobe as a direct competitor to Salesforce in the enterprise marketing space.

The integration of Marketo into Adobe's Experience Cloud created something unprecedented: a platform that could track a piece of content from creation in Photoshop, through distribution via marketing automation, to conversion tracking in analytics, all the way to revenue attribution. The combination of Marketo and Adobe's Experience Cloud will form the definitive system of engagement for B2C and B2B enterprise marketers.

But Adobe's enterprise ambitions went beyond marketing. Document Cloud, anchored by Acrobat and PDF technology, quietly became a billion-dollar business. What started as a way to share documents electronically evolved into a platform for digital signatures, form processing, and document workflows. During the COVID-19 pandemic, when businesses scrambled to go paperless, Adobe Sign and Document Cloud became essential infrastructure.

The company also expanded into digital marketing software and in 2021 was considered one of the top global leaders in Customer Experience Management (CXM). Adobe's Experience Cloud now competed directly with Salesforce, Oracle, and SAP for enterprise marketing budgets. Marketing software is included in the Digital Experience business, which generated $614 million in revenue in the most recent quarter, with 21 percent growth year over year.

The strategic brilliance of Adobe's enterprise pivot was how it leveraged their creative tools dominance. Every enterprise needed both creative assets and marketing technology. Adobe was the only company that could provide both, creating a moat that competitors couldn't cross. A CMO could now go to one vendor for everything from video editing to email automation to analytics.

The financial impact was stunning. By 2020, Adobe's Digital Experience segment was generating over $3 billion annually, growing at 20%+ per year. The company that had started by helping computers talk to printers now helped Fortune 500 companies personalize experiences for millions of customers.

The enterprise expansion also changed Adobe's DNA. They hired thousands of salespeople, built professional services teams, and created industry-specific solutions. The scrappy software company had become an enterprise software giant, competing for multi-million dollar deals with consultants and system integrators involved.

Yet challenges remained. Integration between the various acquired platforms proved complex. Customers complained about the steep learning curve and high total cost of ownership. Smaller competitors like HubSpot gained ground by offering simpler, more integrated solutions.

But Adobe's enterprise gamble had fundamentally transformed the company. No longer just the "Photoshop company," Adobe had become essential infrastructure for how modern businesses create, manage, and optimize digital experiences. The digital marketing pivot proved that Adobe could successfully expand beyond its core creative tools—a lesson that would prove crucial as they faced their next challenge: the rise of collaborative, web-based competitors.

VII. The Figma Saga: The $20B Deal That Wasn't (2022–2023)

Dylan Field couldn't sleep. It was 3 AM on a September night in 2022, and the 30-year-old CEO of Figma was about to make the biggest decision of his life. On his laptop screen was a message from Adobe CEO Shantanu Narayen: final offer, $20 billion, half cash, half stock. Take it or leave it.

Just ten years earlier, Field had been a Brown University dropout, funded by Peter Thiel's fellowship program with $100,000 to pursue his vision of browser-based design tools. Now Adobe—the company that defined creative software—wanted to pay 50 times Figma's annual recurring revenue to acquire his company. It was the largest acquisition Adobe had ever attempted, nearly double their market-moving Marketo deal. The backstory was remarkable. Figma had fundamentally disrupted Adobe's dominance in design tools by doing what Adobe couldn't: building a truly collaborative, browser-based design platform. While Adobe's tools required expensive licenses and powerful computers, Figma ran in any web browser. While Adobe files lived on individual machines, Figma files lived in the cloud with real-time multiplayer editing. Most damaging of all, Figma had become the default choice for a new generation of designers who'd never touched Photoshop.

Adobe announced it has entered into a definitive merger agreement to acquire Figma, a leading web-first collaborative design platform, for approximately $20 billion in cash and stock. The company is expected to add approximately $200 million in net new ARR this year, surpassing $400 million in total ARR exiting 2022, with best-in-class net dollar retention of greater than 150 percent.

The price was staggering. Adobe was paying 50 times Figma's annual recurring revenue—a multiple that made even the frothiest dot-com valuations look conservative. Wall Street reacted with horror. Shares of Adobe sank 17%, their biggest plunge since 2010, wiping out $30 billion in market value in a single day.

But Narayen saw what the market missed. This wasn't just about removing a competitor—it was about acquiring the future of design collaboration. Figma had cracked the code Adobe had been trying to solve for years: how to make professional design tools that were simultaneously powerful and accessible, desktop-class yet browser-based, professional yet collaborative.

The design community's reaction was visceral and immediate. Twitter exploded with memes of Adobe as the Death Star consuming the rebel alliance. Designers who'd fled Adobe's subscription model for Figma's more affordable pricing felt betrayed. The fear was palpable: Would Adobe kill Figma? Jack up prices? Force integration with Creative Cloud?

Dylan Field tried to reassure users. Under the definitive agreement, he would continue to lead Figma as CEO, reporting to David Wadhwani. He promised Figma would remain independent, just with more resources. "With access to Adobe's deep expertise and technology, we believe Figma will be able to achieve our vision of 'making design accessible to all' even faster," he wrote.

But almost immediately, storm clouds gathered. Regulators in Europe and the UK launched investigations. The fundamental question: Was Adobe buying Figma to enhance competition or eliminate it? The UK Competition and Markets Authority was particularly skeptical, noting that Adobe's own XD product competed directly with Figma. For fifteen months, Adobe and Figma executives spent thousands of hours with regulators, trying to convince them the deal would benefit competition. But the regulatory environment had fundamentally changed. The era of Big Tech freely acquiring potential competitors was over. Regulators, particularly in Europe, were determined not to repeat what they saw as past mistakes—letting Facebook buy Instagram and WhatsApp, Google acquire YouTube, Microsoft purchase GitHub.

On December 18, 2023, the inevitable happened. Adobe and Figma announced that they have entered into a mutual agreement to terminate their previously announced merger agreement. Although both companies continue to believe in the merits and procompetitive benefits of the combination, Adobe and Figma mutually agreed to terminate the transaction based on a joint assessment that there is no clear path to receive necessary regulatory approvals from the European Commission and the UK Competition and Markets Authority.

The collapse was costly. Adobe will pay Figma a $1 billion termination fee—cash that would supercharge Figma's already impressive growth. To date, Figma has attracted $333 million in funding, so the $1 billion breakup fee is nearly triple their total raised capital. For a company with around 1,400 employees, this windfall could fund years of aggressive expansion.

Wall Street's reaction was telling. Adobe shares gained 2.2% when the termination was announced. Investors who had hated the deal's price tag were relieved. Some analysts argued Adobe was better off—the company had invested heavily in generative AI through Firefly, potentially leapfrogging Figma's collaborative advantages with AI-powered creation tools.

But the failed acquisition revealed deeper truths about Adobe's position. Despite decades of dominance in creative tools, a ten-year-old startup had fundamentally disrupted their business model. Figma had proven that the future of design was collaborative, browser-based, and accessible. Adobe's attempt to buy that future had failed.

The implications extended far beyond Adobe and Figma. The termination sent a chilling message to the entire tech industry: the era of buying your way out of disruption was over. Large tech companies could no longer simply acquire promising competitors. They would have to out-innovate them.

For Adobe, the failure forced a reckoning. They accelerated development of web-based tools, doubled down on AI integration, and began building more collaborative features into Creative Cloud. Adobe XD, their Figma competitor, was quietly discontinued. The company that had successfully acquired its way through multiple platform transitions would have to learn to compete directly.

For Figma, the outcome was perhaps ideal. They kept their independence, gained a billion-dollar war chest, and emerged as the David who'd forced Goliath to pay tribute. Figma wrapped up 2023 at approximately $600 million in revenue, and the company grew 40% year over year. With their strong metrics and the breakup fee, they had the luxury to remain private and time their eventual IPO perfectly.

The Figma saga revealed Adobe's greatest strength and weakness. They had the financial power to make a $20 billion acquisition, but in a world of increased regulatory scrutiny and rapid technological change, money alone couldn't secure the future. Adobe would have to earn its continued relevance through innovation, not acquisition—a challenge that would define its next chapter in the age of AI.

VIII. The AI Revolution & Future of Creative Work

This section was updated on 22-04-2026.

The demonstration at Adobe MAX 2023 left the audience speechless. On stage, a designer typed a simple prompt: "Extend this image of a beach to show a sunset with palm trees." Within seconds, Adobe Firefly had generated multiple options, seamlessly blending new content with the existing photo. No hours of meticulous Photoshopping. No complex masking. Just describe what you want, and AI creates it.

But backstage, Adobe's executives were sweating. Not about the demo—that had been tested hundreds of times. They were nervous about the protests outside, where artists held signs reading "AI STOLE MY JOB" and "ADOBE BETRAYED CREATIVES." The company that had empowered creative professionals for four decades was now accused of building the technology to replace them.

The journey to this moment had begun years earlier, as Adobe watched the AI revolution unfold. OpenAI's DALL-E, Stability AI's Stable Diffusion, and Midjourney had exploded onto the scene, generating images from text prompts with quality that stunned even experts. Adobe faced an existential choice: resist the AI wave and risk irrelevance, or embrace it and risk alienating their core users. Adobe's approach was distinctly different from its competitors. While others trained their models on scraped internet data of dubious provenance, Adobe's first model, focused on images and text effects, was trained on Adobe Stock images, openly licensed content, and public domain content where copyright had expired—designed from day one to generate content safe for commercial use.

This "commercially safe" approach was critical. Professional designers couldn't risk using AI tools that might generate copyrighted content. Adobe offered something unprecedented: Firefly for Enterprise gave businesses the opportunity to obtain intellectual property indemnification for content generated by most Firefly-powered workflows. Within a year of its beta launch in March 2023, users had generated more than 6 billion images with Firefly, making it the most popular AI image generation model designed for safe commercial use.

But Adobe faced a delicate balance. They needed to empower creators with AI without replacing them. Their solution was positioning AI as a "co-pilot" rather than a replacement—Generative Fill in Photoshop, Generative Recolor in Illustrator, Text to Image in Adobe Express. The backlash came anyway. In June 2024, users discovered new terms of service language that seemed to grant Adobe sweeping rights to user content. Creators panicked, believing Adobe would feed their work into training pipelines. The outcry was swift and brutal. Within days, Adobe rewrote the terms to explicitly pledge it would not use customer data to train its AI models—a promise the company would soon need to operationalize at scale.

The operationalization came at MAX 2025 in Los Angeles, where Adobe revealed the next phase of its strategy. Firefly was no longer just an image model. The company unveiled Firefly Video, capable of generating studio-quality clips from text prompts with consistent characters and camera motion, and Firefly Audio, which could compose royalty-free soundtracks, generate voiceovers, and automatically score a Premiere timeline based on the emotional arc of the cut. For the first time, an editor could storyboard, shoot synthetic B-roll, and lay down a custom score without leaving the Adobe ecosystem—all under the same commercial-safety umbrella that had won over enterprise legal departments.

Equally important was what Adobe announced about the rest of the AI landscape. Rather than insisting Firefly be the only model inside Creative Cloud, Adobe opened the door. OpenAI's Sora and GPT image models, Google's Gemini and Veo, Runway's video tools, and Black Forest Labs' Flux were all made available as selectable engines directly inside Photoshop, Premiere, and Express. The pitch to users was elegant: stay in the Adobe canvas, pick whichever frontier model fits the job, and let Adobe handle the layers, the timeline, the color management, and the final delivery. It was a striking philosophical reversal for a company that had built its empire on proprietary control. Adobe was betting that the value had migrated from the model itself to the workflow wrapped around it.

For enterprises that wanted neither the public frontier models nor an off-the-shelf Firefly, Adobe launched Firefly Foundry in late 2025. Foundry let large customers train custom generative models on their own brand assets, character libraries, and product imagery—indemnified, isolated, and never commingled with another customer's data. Coca-Cola, Mattel, and the NFL were among the announced launch partners. This was Adobe's answer to the unspoken question hanging over every enterprise creative team: how do we use generative AI without surrendering our IP or producing content that looks like everyone else's?

Then, at the 2026 Summit in March, Adobe made its most ambitious move yet: the pivot to Agentic AI. The Firefly AI Assistant, embedded across Creative Cloud, could now execute multi-step creative briefs through natural conversation. "Take our Q2 campaign deck, generate fifteen localized versions for our European markets, swap in the regional product photography from our DAM, and queue them for legal review by Friday"—a request that would have consumed a junior designer's week now ran as an agent task overnight. On the marketing side, the new Adobe Experience Agents went further still, autonomously segmenting audiences in Marketo, drafting and personalizing email variants, generating accompanying creative in Firefly, and pushing live A/B tests to Adobe Experience Manager. Human marketers approved, edited, or vetoed; the agents did the assembly work. It was the most concrete vision yet of what "AI as a co-worker" could mean inside an enterprise software stack, and it gave Adobe a story to tell investors that went beyond defending Photoshop.

The legal cloud that had hung over the company since 2024 finally lifted in the same month. On March 12, 2026, Adobe reached a $150 million settlement with the FTC and DOJ over the lawsuit alleging hidden cancellation fees and deceptive subscription practices. The terms were carefully balanced: a $75 million civil penalty paid to the government, and $75 million returned to affected customers as account credits. Adobe also agreed to a consent decree mandating clear, up-front disclosure of early termination fees, a one-click cancellation flow, and five years of FTC monitoring of its subscription disclosures. The damaging internal email comparing cancellation friction to "heroin for Adobe" had become Exhibit A in the government's case, and the settlement was, in effect, the price of making it go away. CFO Dan Durn called the resolution "an opportunity to reset our relationship with our customers." Investors largely shrugged—$150 million was a rounding error against $7 billion in annual free cash flow—but the reputational mark would linger longer than the financial one.

Competition, meanwhile, intensified from every direction. Figma went public in July 2025, pricing above its expected range and closing its first day at a valuation north of $30 billion. The IPO was, in a sense, Adobe's $1 billion termination fee coming home to roost. Newly public Figma immediately rolled out Figma AI—a suite that included AI-generated design variants, automatic component generation from rough sketches, and multiplayer prompt-to-prototype tools that let entire product teams iterate inside the same browser tab. Within months, Figma had moved decisively into territories Adobe XD had vacated and was pressing into illustration and asset creation as well.

Canva, for its part, set out on its own IPO road show in early 2026, reportedly targeting a valuation in the $60 billion range. Its Magic Studio AI suite—built atop a combination of in-house models and licensed access to OpenAI and Anthropic—had blurred the line between "amateur tool" and "professional tool" almost beyond recognition. Affinity, which Canva had acquired in 2024, was now bundled into Canva's enterprise offerings as a Photoshop and Illustrator alternative at roughly a third of Adobe's price. For the first time in two decades, large marketing organizations were seriously evaluating whether they needed Creative Cloud at all, or whether a Canva-Figma pairing could carry the load.

Yet despite these challenges, Adobe's position remains formidable. Creative Cloud has crossed 35 million subscribers. Firefly has surpassed 25 billion cumulative generations. The company's market cap hovers around $250 billion, and Digital Media ARR continues to grow at low-double-digits even as the AI transition reshapes the underlying mix. For all the controversies and competition, Adobe is still the default choice for most professional creative work—and increasingly, the orchestration layer through which the rest of the AI ecosystem reaches that work.

The deeper question remains unresolved. The moat that protected Adobe for decades—the complexity and power of professional creative tools—is being eroded by AI's ability to make complex tasks simple. A teenager with a Sora prompt and a Canva template can now produce work that would have required a full agency in 2020. Adobe's bet is that as creation becomes effortless, orchestration, governance, and brand-safe assembly become the scarce commodities—and that the company holding the canvas, the timeline, the asset library, and the legal indemnity will capture the value regardless of which model is doing the actual generation. Whether that bet pays off will determine not just Adobe's next decade, but the shape of the entire creative software industry.

Leadership Transition: The End of the Narayen Era (2026) (15–20 min)

This section was updated on 22-04-2026.

The email landed in employee inboxes at 6:01 AM Pacific on March 18, 2026, a day after Adobe's Summit keynote had dazzled Wall Street with the agentic AI demos. The subject line was deceptively plain: "A note from Shantanu." What followed was the announcement the board had quietly been preparing for nearly a year. After seventeen years as chief executive, Shantanu Narayen would step down as CEO of Adobe. He would transition to Executive Chair once his successor was named, and remain involved in strategy, customer relationships, and the continued buildout of Adobe's AI platform. But the day-to-day reins of the company he had defined would pass to someone else.

The timing surprised almost no one inside Adobe, and shocked almost everyone outside it. At 62, Narayen had become one of the longest-tenured CEOs in the S&P 500, outlasting four U.S. presidents, two Apple CEOs, and essentially every peer who had been running a major software company when he took the job in December 2007. But in the quiet corners of the 345 Park Avenue offices and the San Jose executive floor, the succession conversation had been building for years. The Figma collapse, the FTC settlement, the bruising share-price volatility during the Firefly rollout—each had been, in different ways, a capstone. The agentic AI launch at Summit gave Narayen the graceful exit narrative the board had been waiting for. The platform pivot was articulated. The next chapter could belong to someone else.

The Accidental CEO Who Rebuilt Adobe

To understand what was ending, you have to remember what Narayen inherited. When Bruce Chizen handed him the keys in late 2007, Adobe was a company that sold boxed software in shrink-wrapped cardboard, whose fortunes rose and fell with the 18-month Creative Suite release cycle, and whose most important strategic partner—Apple—was about to declare war on its flagship mobile platform. Narayen, a soft-spoken Hyderabad-born engineer who had come up through the product ranks, was not the obvious pick. He had none of Steve Jobs's showmanship, none of Larry Ellison's bombast. His press-conference presence was earnest to the point of invisibility. Analysts politely called him "the operator." Skeptics called him "the caretaker."

What the skeptics missed was that Narayen was playing a much longer game. Within a year of taking over, the 2008 financial crisis gutted enterprise software budgets and exposed the brittleness of Adobe's upgrade-cycle business model. Narayen used the crisis as cover to begin the work that would define his tenure: rebuilding Adobe from a product company into a platform company. The Omniture acquisition in 2009 was his opening move. The painful Flash retreat from 2010 to 2012 was his middle act. And the Creative Cloud announcement in May 2013—the decision that nearly every outside advisor told him would break the company—was his signature. He bet Adobe's entire Digital Media business on a subscription model that customers actively hated, and he held the line while the petitions piled up and the analyst downgrades rolled in.

The math eventually vindicated him in a way that still looks almost implausible on a chart. Adobe's revenue in 2007, the year Narayen became CEO, was $3.16 billion. In fiscal 2025, it crossed $23 billion. The market capitalization went from roughly $22 billion to a peak north of $300 billion before settling, through the AI volatility of 2024 and 2025, at around $250 billion. Free cash flow grew roughly tenfold. Recurring revenue, which barely existed as a concept at Adobe when he took the job, came to represent more than 90% of the business. Measured on the single metric of shareholder value creation, Narayen delivered more of it than any other software CEO of the 2010s save one—Satya Nadella at Microsoft. It was the Creative Cloud bet, not PostScript and not PDF, that ultimately made Adobe an enduring franchise, and it was Narayen who forced it through.

Navigating the AI Pivot

The final act of Narayen's tenure was the hardest to script, and in many ways the one on which his legacy will ultimately be judged. The collapse of the Figma acquisition in December 2023 was, on paper, his biggest professional setback—a $20 billion swing-for-the-fences that ended with a $1 billion termination check and a publicly chastened Adobe. Inside the company, the conversations that followed were brutal and productive in equal measure. Narayen reportedly told the executive team in a private session that winter that if Adobe couldn't build its way forward, it didn't deserve to exist as an independent company. The Firefly acceleration, the model-agnostic strategy unveiled at MAX 2025, the Foundry launch, and ultimately the Experience Agents reveal at Summit 2026 all trace back, in varying degrees, to that post-Figma reckoning.

What Narayen managed—and what the new CEO will inherit—was the philosophical reframing of Adobe's role in the AI stack. For forty years, Adobe's identity had been rooted in proprietary tools and proprietary formats. Narayen's late-career wager was the opposite: that in the AI era, the canvas would matter more than the brush, and that Adobe's value would increasingly come from orchestrating other people's models rather than jealously guarding its own. It was, he told employees in his farewell video, "the hardest intellectual shift we've asked this company to make since I've been here." Whether it proves to be as prescient as the Creative Cloud pivot or as premature as the Flash bet will not be knowable for another decade. He is leaving that judgment for the next chief executive, and for history.

The Search for an AI-Native Successor

Within forty-eight hours of the announcement, the board had already been working its succession shortlist for months. Lead director Amy Banse and the committee engaged Spencer Stuart in mid-2025, and by the announcement date they had narrowed the field to roughly half a dozen serious candidates. Three broad archetypes emerged in the leaks that followed. The first was the internal-continuity pick: David Wadhwani, president of Adobe's Digital Media business and the executive who had personally run the Figma negotiation and the subsequent Firefly acceleration. Wadhwani had once left Adobe for AppDynamics, come back in 2021, and was widely seen as the heir apparent throughout Narayen's final years. The second archetype was the enterprise-AI import—names floated in the financial press included senior leaders from OpenAI, Anthropic, and the AI divisions of the hyperscalers, a reflection of the board's stated desire for what it called, somewhat awkwardly, an "AI-native" CEO. The third was the outside CEO with a track record of running a large platform through a technology transition—a Satya-Nadella-style pick, with the Microsoft parallel explicit enough that several candidates in that mold were reportedly approached.

The board's framing of the search told its own story about where Adobe believes it is. Banse, in a CNBC interview on March 19, said the committee was looking for "someone who understands that the creative software of 2030 is going to look as different from today's Creative Cloud as Creative Cloud looked from Creative Suite." The subtext was unmistakable. The incoming CEO would not be asked to operate Narayen's Adobe more efficiently. They would be asked to remake it, possibly painfully, for an era of autonomous agents, orchestrated models, and customers who increasingly expect creative software to do the work rather than merely enable it. Whoever takes the role will inherit a company at the height of its powers and, arguably, at the peak of its vulnerability.

The $25 Billion Signal

On April 9, 2026, three weeks after the CEO announcement and one day after Adobe's Q1 earnings beat, the board delivered its second message. It authorized a new $25 billion share repurchase program, the largest in the company's history, replacing the existing authorization with roughly $4 billion remaining. The program had no expiration date, and management indicated on the call that Adobe intended to execute the bulk of it within three to four years. At the then-current share price, $25 billion represented roughly 10% of the outstanding float.

The signaling was deliberate and layered. On the surface, it was a statement of financial confidence: Adobe was generating more than $8 billion in annual free cash flow, carrying minimal net debt, and had few obvious uses for the cash beyond buybacks given the post-Figma regulatory environment that effectively foreclosed transformative M&A. Beneath the surface, it was a message to a jittery shareholder base about continuity. The CEO transition would be disruptive; the capital return framework would not. "We have tremendous confidence in the long-term opportunity ahead of Adobe," CFO Dan Durn said on the earnings call, "and this authorization reflects that confidence at a moment when clarity matters most to our shareholders." Translation: the leadership may change, but the capital allocation discipline that Narayen had built—consistent buybacks, no dividend, no empire-building acquisitions—would outlast him.

Wall Street read the combined package the way the board had intended. Adobe shares rose 4.3% on the day of the buyback announcement, their best single-day performance in over a year. Several analysts upgraded their price targets on the grounds that Adobe had, in essence, put a floor under the stock during the succession window. Bernstein's note captured the sentiment: "This is a company telling you it is worth more than the market thinks, and backing the statement with a quarter of its market cap."

Endings and Beginnings

Narayen's final letter to shareholders, published alongside the proxy in late April, was characteristically understated. He thanked the founders—"John and Chuck," as he always called Warnock and Geschke—for the culture they built, the employees who had delivered through multiple platform transitions, and the customers who had, often reluctantly, come along for the Creative Cloud journey. He made only one forward-looking commitment, and it was a personal one: that he would remain available to his successor for as long as he or she wanted him involved, and not a day longer.

What he did not say, but what the numbers and the buyback and the careful staging of the succession all implied, was that he believed the Adobe he was handing over was still, at its core, the same company Warnock and Geschke had founded—a company built on the conviction that creative work matters, and that the tools of creation deserve to be engineered with as much rigor as the art they enable. Whether that conviction survives the AI transition under a new CEO is the question that will shape Adobe's next decade. It is also the question that sets up the broader investing lessons that define how a company like Adobe endures, transforms, and occasionally stumbles across more than four decades of reinvention.

IX. Playbook: Business & Investing Lessons

Platform Transitions: The Art of Crossing the Chasm

Adobe's history reads like a masterclass in platform transitions. From PostScript to desktop software, desktop to web, perpetual licenses to subscriptions, and now traditional tools to AI-powered creation—each transition could have killed the company. Instead, Adobe emerged stronger.

The key lesson: cannibalize yourself before others do. When Adobe launched Creative Cloud, they knew it would destroy their packaged software business. CS6 generated massive upfront revenue; subscriptions meant smaller monthly payments. Wall Street hated it initially. But Adobe understood that clinging to the old model meant slow death by a thousand cuts from nimbler competitors.

The execution matters as much as the strategy. Adobe didn't just flip a switch—they offered transition pricing, maintained CS6 for years, and gradually improved Creative Cloud until the value proposition became undeniable. They accepted short-term pain (customer backlash, revenue disruption) for long-term gain (predictable revenue, deeper customer relationships).

The Subscription Model Transformation: From Product to Service

Adobe's shift to subscriptions in 2013 remains one of the most successful business model transformations in software history. The numbers tell the story: Adobe's market cap grew from $20 billion in 2012 to over $200 billion by 2024. But the real lessons go deeper than financial metrics.

First, timing is everything. Adobe waited until broadband was ubiquitous, cloud storage was trusted, and software-as-a-service was proven. They weren't first—they were right. Second, you need monopoly power to force such a dramatic change. Adobe could demand subscriptions because creative professionals had no real alternative. Try this without market dominance, and customers simply leave.

The subscription model fundamentally changed Adobe's relationship with customers. Instead of huge upgrade cycles where they had to convince users to pay again, Adobe now had continuous engagement. They could ship features monthly instead of waiting 18 months. Customer feedback became immediately actionable. The company transformed from a software vendor to a service provider.

M&A Strategy: When to Buy vs. Build

Adobe's acquisition track record reveals a nuanced M&A philosophy. Successful deals (Macromedia, Marketo, Magento) shared common traits: they filled genuine product gaps, brought new customer bases, and could be integrated into Adobe's ecosystem. Failed or abandoned deals (Figma) highlight the limits of acquisition in today's regulatory environment.

The Macromedia acquisition for $3.4 billion in 2005 remains the gold standard. Adobe didn't just buy Flash—they acquired Dreamweaver, Fireworks, and most importantly, web DNA. The cultures clashed, integration was messy, but Adobe emerged with the tools to dominate digital creative work for the next decade.

Contrast this with Figma. At $20 billion, Adobe was paying 50x ARR—a multiple that suggested desperation more than strategy. The deal's collapse saved Adobe from potential buyer's remorse but highlighted a crucial weakness: their inability to build collaborative, web-native tools internally. Sometimes the best deals are the ones you don't make.

Network Effects and Ecosystem Lock-in

Adobe's true moat isn't any single product—it's the ecosystem. A designer starts with Photoshop, adds Illustrator, needs InDesign for layout, Premiere for video, After Effects for motion graphics. Each additional product makes the others more valuable. Files flow seamlessly between applications. Keyboard shortcuts transfer. Skills compound.

This ecosystem lock-in extends beyond products to file formats. PSD, AI, INDD files become industry standards. Even if competitors build better tools, they must support Adobe's formats. Creative teams can't switch unless everyone switches. Agencies can't abandon Adobe unless their clients do too. It's a prisoner's dilemma where cooperation means staying with Adobe.

The lesson for builders: ecosystems beat point solutions. The lesson for investors: look for companies building platforms, not just products. The strongest moats are built not from one deep trench but from interlocking defenses that become stronger over time.

The Power of Standards and File Formats

PostScript and PDF represent Adobe's most underappreciated achievements. By making PostScript an open standard, Adobe sacrificed short-term licensing revenue but gained long-term industry dominance. Every printer manufacturer had to support PostScript. Every designer had to understand it. Adobe controlled the standard that controlled the industry.

PDF took this strategy further. Released free for viewing but charged for creation and editing, PDF became the universal document format. Governments mandated it. Courts required it. Every business used it. Adobe monetized PDF not through the format itself but through the tools around it—Acrobat for creation, Sign for signatures, Document Cloud for management.

The strategic insight: in technology, controlling the standard is more valuable than controlling the product. Make your format indispensable, then monetize the ecosystem around it. Give away the razors, sell the blades—but make sure you own the design of both.

Bundling Strategy and Pricing Power

Creative Suite was a bundling masterpiece. Instead of selling Photoshop for $700, Illustrator for $600, and InDesign for $700 separately, Adobe offered all three plus more for $1,800. Customers felt they were getting a deal. Adobe increased average revenue per user. Competitors selling point solutions couldn't match the value.

Creative Cloud took bundling to its logical extreme. For $50/month, users got everything—over 20 applications plus services. The price seemed high for someone who only needed Photoshop ($20/month standalone) but incredible for anyone using multiple tools. This pricing architecture pushed users toward the higher-value bundle, increasing ARPU while making switching costs prohibitive.

The bundling lesson extends beyond pricing. Adobe bundles features, services, and increasingly, AI capabilities. Each addition makes the bundle more valuable and competitors less relevant. It's a strategy that requires patience and capital but creates compounding competitive advantages.

Managing Innovator's Dilemma

Adobe repeatedly faced the innovator's dilemma—disruptive technologies that threatened their core business. Flash was disrupted by HTML5. Desktop software was threatened by web apps. Professional tools faced competition from prosumer alternatives. Yet Adobe survived and thrived through each disruption.

Their approach: embrace the disruption but on their terms. When web-based tools threatened desktop software, Adobe didn't rush to rebuild everything for browsers. They waited, learned, and eventually launched web versions that complemented rather than replaced desktop apps. When AI threatened to democratize creativity, Adobe integrated AI as a feature, not a replacement.

The key insight: incumbents can survive disruption if they're willing to cannibalize themselves gradually rather than waiting for others to do it suddenly. Adobe's genius was in managing the pace of transition—fast enough to stay relevant, slow enough to bring customers along.

These lessons—platform transitions, subscription models, strategic M&A, ecosystem building, standard setting, bundling, and managing disruption—form Adobe's playbook. It's a playbook that transformed a printer software company into a creative software empire, and it offers enduring lessons for anyone building or investing in technology businesses.

X. Bear vs. Bull Case & Competitive Analysis

This section was updated on 22-04-2026.

The Bull Case: The Enterprise Moat and the Agentic Future

Step back from the noise of the last eighteen months and the bull thesis on Adobe is, at its core, an enterprise thesis. Creative Cloud is the storefront. Experience Cloud is the business. The combination of Creative Cloud, Experience Cloud, and Document Cloud has quietly become the only end-to-end platform that spans the full lifecycle of a digital experience—from the moment a junior designer opens a blank canvas to the moment a marketer measures the click that converted. No other vendor plays across all three layers. Salesforce has the CRM but not the creation tools. Canva has the templates but not the analytics. Figma has the design surface but not the distribution and measurement stack. Adobe sits in the middle, and the middle is where enterprise budgets are consolidating.

The financial profile that underpins this position is, frankly, extraordinary. Fiscal 2025 closed at a record $23.77 billion in revenue. Gross margins remain north of 88%. Operating margins hover around 45%. Free cash flow exceeds $8 billion annually. Net revenue retention across the Digital Experience business continues to print in the 110–115% range. These are the unit economics of a software utility with the growth profile of a platform company, and they are what give the board the room to do things like authorize the $25 billion repurchase program unveiled in April 2026. That buyback, at roughly 10% of the float, is not a defensive crouch—it is a signal that the board believes the market is mispricing an asset whose earnings power is durable enough to swallow a quarter of its own equity within four years.

The AI story, in the bull reading, has also fundamentally changed. Twelve months ago the anxiety was that generative AI would commoditize creation and strand Adobe as a legacy tool vendor. The agentic pivot announced at Summit 2026 reframes the question. Adobe is no longer selling a brush; it is selling the outcome. A Fortune 500 CMO does not want fifteen variants of a European campaign—she wants the variants generated, localized, legally cleared, and queued for review by Friday. That is a workflow Firefly Agents and Experience Agents can now deliver inside a single governance boundary, with indemnification attached. Startups selling raw generative capability cannot match that. Enterprise buyers, for whom brand safety and legal exposure matter more than the specific model under the hood, are exactly the customers Adobe has cultivated for a decade.

And then there is the transition question. The buyback, the model-agnostic strategy, and the agentic roadmap together form a coherent answer to the CEO succession risk. Whoever replaces Shantanu Narayen will inherit a company whose capital allocation framework is pre-committed, whose AI architecture is already announced, and whose balance sheet is arguably the strongest in enterprise software. That is, in the bull view, the definition of a de-risked transition at a great franchise.

The Bear Case: Succession, Siege, and the Shrinking Middle

Bears look at the same facts and see a company at peak vulnerability. Start with leadership. Narayen's retirement, however well staged, removes the single executive whose strategic muscle memory made the Flash retreat, the Creative Cloud bet, and the post-Figma Firefly acceleration possible. Software history is littered with franchises that coasted on an outgoing CEO's momentum for two years and then stalled—Oracle after Ellison stepped back from the CEO role, IBM after Gerstner. An "AI-native" successor parachuting into a 28,000-person creative software company is not a low-risk operation, regardless of how long the search has been running.

The competitive picture, meanwhile, has deteriorated on nearly every flank. Figma's July 2025 IPO, initially priced to raise a few billion, has aged into a public market monster: shares roughly doubled from the first-day close, pushing the company to a market capitalization near $57 billion and giving it a currency for M&A that rivals Adobe's own. "Figma Draw," rolled out in early 2026, is a direct assault on Illustrator's vector franchise—a category Adobe had considered untouchable since 1987. Dylan Field has been explicit that illustration, image editing, and motion are next on the roadmap. Figma is no longer a collaborative design tool nibbling at XD's corpse. It is a full-stack design platform with public-market fuel.

Canva is executing a different but equally pointed pincer. The Affinity acquisition, closed in 2024, is now bundled into Canva's enterprise tier at roughly a third of Creative Cloud Pro's price—Photoshop and Illustrator substitutes sitting one click away from a tool marketing teams already use. The December 2024 acquisition of Leonardo.ai gave Canva a native generative model to slot beneath Magic Studio, reducing its reliance on licensed frontier models and letting it price aggressively against Firefly. And Canva's own IPO road show, underway as of early 2026 at a reported $60 billion target, is designed to arm the company with enterprise sales capacity it has historically lacked. For the first time in two decades, heads of marketing at large enterprises are genuinely evaluating whether a Canva-plus-Figma pairing can replace Creative Cloud outright.

The AI-native flank is worse. Midjourney, Runway, Sora, Flux, and the long tail of specialist models are not trying to replace Adobe—they are redefining what the job is. Why does a social team need Premiere when CapCut plus Sora produces ninety percent of the output at five percent of the cost and zero of the learning curve? Adobe's model-agnostic strategy elegantly addresses this by putting rival models inside its canvas, but it also implicitly concedes that the model itself is a commodity. If the canvas is all Adobe truly owns, the canvas had better be extraordinarily sticky—and Figma has spent a decade demonstrating what happens when a better canvas shows up.

Then there is the margin question, which the bull case tends to sidestep. Agentic workflows are compute-intensive. A single Experience Agent run that generates dozens of creative variants, localizes them, and pushes personalized A/B tests can consume more GPU than a month of traditional Photoshop usage. Adobe has begun passing some of this through as higher ARPU on "Creative Cloud Pro," the AI-premium tier that replaced the standard All Apps plan. But the pricing power is bounded by Canva and Figma below it, and the cost curve on frontier inference is not falling as fast as the bulls assume. The long-term margin profile of a Firefly-led Adobe may be closer to 40% operating margin than 45%, and on $30+ billion of revenue that is real money the market has not yet reckoned with.

Finally, the regulatory ghost has not fully departed. The FTC consent decree runs for five years. The Figma termination is an object lesson that transformative M&A is effectively off the table. Adobe is being asked to out-innovate younger, better-capitalized, regulatorily-unencumbered competitors—with a new CEO, a monitored consumer subscription business, and a compute cost structure it does not fully control.

Competitive Landscape: The Reshaped Map

The competitive picture in April 2026 looks meaningfully different from the one Adobe faced two years ago, and each segment tells a different story about how the moat is holding.

Professional design is now a two-horse race that Adobe is not winning outright. Figma Draw targets the vector workflows Illustrator has owned for nearly forty years, and early adoption inside product-design and marketing teams has been rapid. Adobe's counter—deeper Firefly integration inside Illustrator plus a rebuilt web version—is directionally right but has not yet stemmed the generational handoff to Figma among designers under thirty.

Casual and mid-market creation is increasingly Canva's domain, and the Affinity bundle has pulled Canva upmarket into the exact mid-market accounts where Adobe historically converted freelancers into Creative Cloud Pro subscribers. Adobe Express has grown, but it grows in a market Canva is also growing into, from a stronger base.

Generative AI tools have settled into a layered structure Adobe explicitly embraced. Frontier models from OpenAI, Google, Black Forest Labs, and Runway live inside the Creative Cloud canvas as selectable engines. Firefly coexists alongside them. The open question is whether orchestration value accrues to Adobe or whether the frontier labs eventually build their own canvases—a scenario that OpenAI's direct-to-creator product experiments make less hypothetical every quarter.

Video is bifurcating faster than any other category. Premiere retains its grip on Hollywood and broadcast, where the review-and-approval, color-management, and union-workflow requirements remain genuine moats. But social and creator video has decisively moved to CapCut, with Runway and Sora-first workflows reshaping what "editing" even means. Adobe's Firefly Video plus agentic scoring and voiceover is a credible answer for the professional middle, but the mass-market end is lost.

Enterprise marketing and experience remain Adobe's strongest flank. Experience Cloud plus Marketo plus the new Experience Agents now constitute the most complete B2B and B2C marketing stack on the market. Salesforce still has the CRM anchor, but Adobe's agentic advantage on the creative-assembly side is real, and deal sizes are trending up.

Market Size, Growth, and the Outcomes Shift