FactSet Research Systems Inc. (FDS): The Excel Whisperer and the Battle for Wall Street's Middle Office

I. Introduction & Episode Roadmap

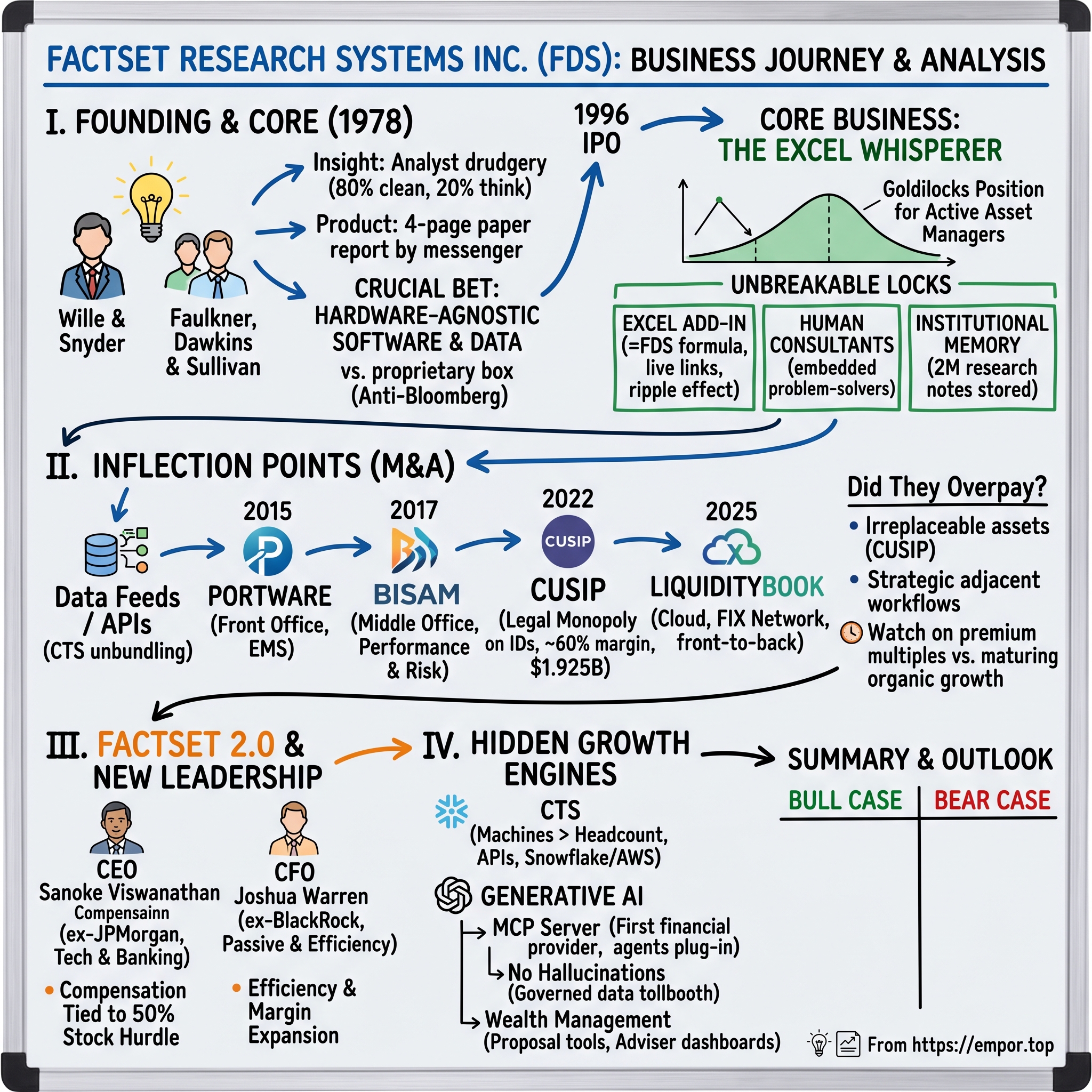

In the autumn of 2021, two of the most powerful data empires on Earth were trying to become one. S&P Global was attempting to swallow IHS Markit in a stock-for-stock deal worth roughly $44 billion, a transaction so large it would reshape the plumbing of global finance. But Brussels had a problem. Before the European Commission would bless the marriage, its competition regulators went looking for the chokepoints — the assets so essential that combining them would hand one company a stranglehold. On October 22, 2021, the Commission cleared the merger, but only after extracting a list of forced divestitures.2 Buried in that list was the crown jewel of the entire financial system: CUSIP Global Services, the registry that assigns the nine-character identification code stamped on virtually every stock and bond traded in North America.

S&P didn't want to sell it. CUSIP is the closest thing in capital markets to a literal tollbooth — a small, sleepy, fabulously profitable business that collects a fee every time anyone licenses, stores, or distributes the codes that make trading possible. But regulators don't negotiate with crown jewels. So on December 27, 2021, S&P announced it would sell CUSIP Global Services to FactSet Research Systems for $1.925 billion in cash.[^2][^4] The deal closed on March 1, 2022. S&P's antitrust pain became FactSet's structural windfall. A company that began life in 1978 as a four-page paper report delivered by bicycle messenger had just bought a legal monopoly on the identity system of American securities.

That juxtaposition is the whole story of FactSet in miniature. It is not the loudest name in financial data. It is the fourth-largest of the so-called Big Four, dwarfed by Bloomberg, by the London Stock Exchange Group, and by the very S&P that just handed it CUSIP. And yet, by fiscal 2026, FactSet had grown into a roughly $17 billion market-capitalization business generating more than $2.4 billion of annual subscription value, with a client base of over 9,100 firms and a retention rate that hovers in the mid-90s.1 It has compounded revenue for more than four decades without a single down year.

The thesis we want to test in this episode is that FactSet is the ultimate anti-Bloomberg. It did not win by building a proprietary glowing terminal and charging a $27,000-a-year status-symbol toll. It won by doing something quieter and arguably more durable: embedding itself into the plumbing of Microsoft Excel, blanketing clients with white-glove human service, and colonizing the unglamorous middle office of asset management — the world of performance attribution, risk, and compliance that nobody writes magazine profiles about. The question for investors is whether that quiet moat is as deep as the bulls claim, or whether a maturing core, a structural drift from active to passive investing, and the arrival of generative AI are about to test it for the first time in forty-five years.

Here's our roadmap. We'll start with the founding and the hardware-agnostic bet that defined everything. We'll dissect the core economics behind that mid-90s retention number, and then map the four-player oligopoly FactSet competes in. We'll walk the inflection points of the last two decades — the pivot to raw data feeds, and the acquisition chain of Portware, BISAM, CUSIP, and LiquidityBook. We'll interrogate whether management overpaid. We'll meet the new commanders of "FactSet 2.0," CEO Sanoke Viswanathan and CFO Joshua Warren. We'll examine the hidden growth engines in data solutions and AI. We'll run the business through Hamilton Helmer's 7 Powers and Porter's Five Forces, subject it to an activist stress test, and close on the bull and bear cases. Let's begin where every good origin myth begins — with two men who quit.

II. Founding & The Hardware-Agnostic Bet

Picture lower Manhattan in 1978. The Dow is going nowhere, stagflation is grinding down the economy, and Wall Street research is still an analog craft. An analyst who wants to compare three companies' balance sheets does it the hard way: pulling annual reports, copying numbers onto ledger paper by hand, double-checking arithmetic with a calculator. Into this world walked Howard Wille and Charles Snyder, two men whose employer, the brokerage Faulkner, Dawkins & Sullivan, had just been swallowed in an acquisition.4 Wille had run research there. Snyder was the quantitative mind, a mathematician fascinated by what the new mainframe computers could do.

Wille had made a deceptively simple observation watching his analysts work: they spent roughly eighty percent of their time finding and cleaning data and only twenty percent thinking about it. The scarce, valuable human judgment was being drowned by clerical drudgery. If you could flip that ratio — automate the gathering and let the analyst think — you'd have a product Wall Street would pay almost anything for. In September 1978, the two founded FactSet Research Corporation to chase exactly that idea.4

The first product was almost charmingly literal. It was the fact set: a standardized, four-page summary of a company's fundamentals — revenues, margins, ratios, the essentials an analyst needed at a glance. A client would order one on a given company, and a courier would physically deliver the printed report.4 It was the right insight wrapped in the wrong technology. Paper doesn't scale, and it doesn't refresh. But the insight underneath — that the value was in pre-cleaned, structured, comparable data — would prove to be one of the great durable franchises in business.

Then came the fork in the road that defined the next half-century. Snyder understood that mainframes could run the database queries that produced those reports far faster than any human. The obvious move, the move a hardware company would make, was to build a proprietary machine — a dedicated terminal that clients would rent, locking them into FactSet's box. A young trader named Michael Bloomberg would make precisely that bet a few years later, in 1981, and build a colossus on it. Wille and Snyder went the other way. They decided FactSet would be hardware agnostic — it would run on whatever machine the client already owned.4

This sounds like a footnote. It was the whole architecture of the company's future moat. By refusing to sell hardware, FactSet was forced to be a software and data company, and software and data have economics that hardware never will: near-zero marginal cost to serve another user, and the ability to ride every wave of someone else's hardware innovation for free. As Wall Street migrated from mainframes to PCs through the 1980s and 1990s, FactSet didn't have to retool a factory. It just wrote software for the new machines. As early as 1981 it could download data straight into spreadsheets — the first hint of the Excel strategy that would later become an unbreakable lock.4

Through the 1980s the product steadily climbed the value chain. What began as a single integrated database grew, by the end of the decade, into a more sophisticated private database service that let clients layer their own proprietary information on top of FactSet's content — an early, analog version of the institutional-memory lock that would later prove so powerful.4 Each step followed the same logic: do the unglamorous work of integration so the analyst doesn't have to, and make the resulting product so woven into the daily routine that leaving becomes unthinkable. The genius was that FactSet was building switching costs before "switching costs" was a phrase anyone on Wall Street used.

The business model that emerged was elegant. FactSet didn't generate most of its own raw data. Instead it licensed feeds from many external providers — Compustat fundamentals, SEC filings, pricing services — then did the unglamorous work of integrating, cleansing, and reconciling them into one consistent, queryable whole, and streamed the result to the client's own machine. It was, in essence, an aggregator and a janitor: the company that made everyone else's messy data usable. That position — owning the integration layer rather than the raw content — is subtle, and it's why FactSet could later be both a customer and a competitor of the very firms whose data it resold.

On June 28, 1996 — thirty years ago to the day as we record this — FactSet Research Systems listed on the New York Stock Exchange under the ticker FDS.4 It was small and profitable, and the market filed it under "low-margin software services," a sleepy reseller of other people's numbers. What investors missed entirely was the flywheel quietly spinning underneath: a subscription business with brutal switching costs and a service model that turned customers into hostages who were thrilled to be captured. To understand why that flywheel is so powerful, we have to open the engine up.

III. The Heart of the Story: The Core Business & Wall Street's Oligopoly

Walk onto any institutional trading floor and you'll see the screens. The glowing amber-and-black of a Bloomberg Terminal. The dense data grids. What you can't see is the more interesting war — the one being fought not over the trader's desk but over the analyst's spreadsheet, the risk manager's model, and the compliance officer's report. That invisible territory is where FactSet lives, and to understand the prize, you first have to understand the battlefield.

Financial data is an oligopoly of four players operating at wildly different scales. At the top sits Bloomberg, the undisputed hegemon, with an estimated $13–15 billion in annual revenue and roughly a third of the entire market. Its strength is fixed income, real-time news, and — crucially — the Instant Bloomberg chat system, the messaging network where the buy side and sell side actually talk to each other. That chat function is a genuine social network with genuine network effects: you keep your Bloomberg not because the data is irreplaceable but because everyone you trade with is on it. Leaving means going silent. That's a different, and in some ways deeper, moat than anything FactSet has.

Second is the London Stock Exchange Group, which in 2021 absorbed Refinitiv — the old Thomson Reuters terminal and data business — for around $27 billion. LSEG carries an enormous global footprint, perhaps $10 billion of financial-data revenue and roughly a fifth of the market, with particular strength in foreign exchange and trading infrastructure. But it inherited Refinitiv's notoriously tangled legacy technology, and much of its energy this decade has gone into untangling it rather than gaining share. Third is S&P Global Market Intelligence, home of the Capital IQ platform — the gold standard for fundamental credit data, M&A deal screening, and private-market intelligence, the natural tool of the investment banker and the credit analyst. S&P deserves a closer look because it is the rival most likely to threaten FactSet directly. The two overlap heavily on fundamental data, and S&P has spent years investing to close the gap in portfolio analytics — the one area where FactSet has historically been clearly superior. S&P also enjoys a structural advantage FactSet can't easily match: it owns enormous amounts of proprietary content outright, from credit ratings to indices to the vast private-company datasets it pulled in through the IHS Markit merger. FactSet, by contrast, still licenses much of its underlying raw data from third parties and competes on integration and workflow rather than on owning the content. That distinction — owner versus aggregator — is exactly what the CUSIP acquisition was designed to start changing, and it helps explain why FactSet was willing to pay so dearly for an asset it could finally own outright.

And then there's FactSet, the smallest of the four, with roughly $2.4 billion of revenue and only a low-single-digit share of the global pie.1 But that framing is misleading, because FactSet is not trying to be everywhere. It is a surgical specialist in one specific workflow: the daily life of the active asset manager.

It's worth pausing on why being the smallest player has, paradoxically, been a strength rather than a weakness. Bloomberg and LSEG are platform companies; their scale forces them to be all things to all clients, which makes them powerful but also bloated and slow to change. FactSet's relative smallness let it stay focused and let it counter-position — it never had to defend a giant legacy revenue base from cannibalization, the way Bloomberg must defend its premium terminal. Smallness also meant FactSet could be the agile partner that customizes, that ships the feature an asset manager actually asked for, that sends a human to sit beside the client. In a commoditizing data industry, "we are the specialist who actually understands your job" is a defensible position precisely because the giants find it uneconomic to match. The risk on the other side of that coin is that a specialist has nowhere to hide if its one chosen niche shrinks — concentration cuts both ways.

Here is the single most important number for understanding the company. Roughly four-fifths of FactSet's annual subscription value — what the company calls ASV — comes from the buy side: active asset managers, hedge funds, wealth managers, and pension funds. Only a slim minority comes from the volatile sell side of investment banking and advisory.1 That mix is a feature, not an accident. Banking revenue swings violently with the deal cycle; you can lose thirty percent of it in a bad year. Asset managers, by contrast, pay to run their portfolios every single day, in bull markets and bear markets alike. FactSet deliberately anchored itself to the steadier, stickier customer.

Why do those asset managers choose FactSet over the bigger names? It comes down to a Goldilocks position. Bloomberg is overkill — and overpriced — for a junior analyst who just needs to build a fundamental valuation model; you don't pay full terminal freight to look up a company's revenue history. S&P's Capital IQ is superb for screening deals but historically thin on the portfolio analytics an asset manager needs to measure performance, attribute returns, and monitor risk across an entire book. FactSet sits precisely in the gap: rich enough on fundamentals and analytics for the portfolio manager, affordable enough for the analyst, and built around the workflow of running money rather than doing deals. It fits the middle, and the middle is enormous.

But the position alone doesn't explain the retention. The lock does. And the lock is Excel.

This is the part of the story that deserves to be taught in business schools. FactSet did not try to defeat Microsoft Excel or replace it with a proprietary interface. It did the opposite — it became Excel's plumbing. FactSet's Excel Add-in lets an analyst write a formula like =FDS(...) directly into a spreadsheet cell, and that cell becomes a live, refreshable link to FactSet's databases. Pull up a model in the morning, hit refresh, and yesterday's prices and the latest filings flow in automatically. Now multiply that across a firm. A mid-sized asset manager has thousands of proprietary valuation models, built over years by analysts who have since left, each one hard-wired with FactSet formulas. Ripping out FactSet doesn't mean swapping a login. It means rewriting every one of those spreadsheets by hand, re-validating each model, and praying you don't introduce an error that blows up a real trade. The switching cost isn't high. It's closer to infinite — and it's the kind of cost that compounds the longer a client stays.

Then there is the human layer, which is where FactSet does something genuinely unusual. Most software companies treat customer service as a cost center to be minimized and offshored. FactSet treats it as a weapon. The company hires smart, energetic, relatively inexpensive recent college graduates as "Consultants" and embeds them with clients. These consultants don't just answer tickets — they write the custom Excel formulas, build the models, and solve the analyst's actual problems. For an asset manager, a FactSet consultant functions as an outsourced, included-in-the-price junior analyst. That does two things at once: it makes the product dramatically stickier, because the client's workflows are co-built with FactSet, and it converts the price-conscious buyer into a loyalist. You don't churn the vendor whose people effectively work on your team for free.

There is a third lock that gets less attention but may be the deepest of all: the data the client creates inside FactSet. Buy-side analysts don't just consume FactSet's numbers — they write their own. Their proprietary research notes, their estimates, their internal flags and overrides accumulate inside the platform year after year. By management's own account on the Q2 fiscal 2026 call, FactSet's buy-side analyst clients store more than two million research notes in its databases, a figure that has been growing north of 35 percent annually for three straight years.13 Think about what that means for switching costs. An asset manager can, in theory, rebuild its Excel models elsewhere. It cannot easily extract a decade of institutional memory — the accumulated judgment of analysts past and present — and re-implant it into a rival system. FactSet doesn't just sit in the workflow; it becomes the firm's memory. Management openly calls this one of the crown jewels of the franchise, and from a moat perspective it's hard to argue.

The result of the Excel lock, the human lock, and the institutional-memory lock is a retention rate that sits in the mid-90s — meaning that in any given year the company keeps the overwhelming majority of the revenue it had, and grows from a near-intact base.1 For investors, that is the entire engine. A subscription business that almost never loses a customer needs only to add a little, sell a little more, and let the compounding do the rest. It is worth being precise about what this retention number does and doesn't tell you, though. A high retention rate measures the stickiness of existing relationships; it says nothing about whether the pool of customers is growing or shrinking. You can retain 95 percent of a market that is itself contracting, and the math will quietly erode beneath you. That is exactly why the most important risk to FactSet isn't a competitor prying clients loose — it's the clients themselves shrinking, consolidating, or disappearing into passive vehicles that need fewer analysts. Hold that thought; it's the heart of the bear case, and we'll come back to it. First, the moves that turned a research tool into an operating system.

IV. The Great Inflection Points of the Last Two Decades

Every durable franchise eventually faces the same quiet danger: the core business matures while management is still congratulating itself. FactSet's leadership saw it coming in the early 2010s, and the past fifteen years are best understood as a series of deliberate moves to keep the company indispensable even as its original product — the desktop workstation — slowed. Each move pushed FactSet into a new room of the client's house.

The pivot to data feeds. The first realization, in the early 2010s, was uncomfortable. The financial crisis had left every institution hunting for costs, and one of the most visible targets was the row of expensive data terminals on the trading floor. Banks and asset managers began rationalizing their "desktop footprint" — counting the screens, asking which analysts truly needed a full workstation, and trimming. If FactSet's entire business was workstation seats, this was an existential trend, not a passing one. But management noticed something subtle about how clients behaved. It is relatively painless for a firm to cancel a workstation seat — you take back a login, the analyst grumbles, life goes on. It is agonizing to rip out a raw data feed that has been wired directly into the firm's own databases, risk engines, compliance systems, and quantitative models, because dozens of downstream processes silently depend on it. Removing a feed risks breaking things nobody fully understands anymore.

So FactSet leaned into that asymmetry. It began selling unbundled, clean data delivered straight into client data lakes via standardized feeds and APIs — the business it eventually branded Content & Technology Solutions. The strategic logic was elegant and, in hindsight, prescient: decouple FactSet's fortunes from the human headcount on the floor. Even if a firm laid off ten percent of its analysts, its machines — its models, dashboards, and risk systems — would consume more data, not less, and FactSet could capture that spend in a form that didn't require anyone to be sitting at a screen at all. This was the company quietly building its own hedge against the very trend that threatened its core, years before the market understood the threat existed.

Portware (2015) — into the front office. Historically FactSet was a place where you decided what to trade, not where you traded it. An analyst studied the data, the portfolio manager made the call, and then everyone switched to entirely different software to actually execute. That handoff was a leak — value flowing to other vendors. In September 2015, FactSet acquired Portware, a multi-asset Execution Management System, for $265 million in cash, closing the deal that October.5 Portware pushed FactSet directly into the transactional front office, into the moment of execution itself. It was initially margin-dilutive, and skeptics fairly asked whether a research company could run a trading system. But it planted the flag in territory FactSet had never held.

BISAM (2017) — owning the middle office. If Portware was about the glamorous front office, the 2017 acquisition of BI-SAM Technologies for $205.2 million was about the unglamorous middle office — and arguably mattered more.6 BISAM was the premier tool for portfolio performance measurement, return attribution, and GIPS-compliant reporting: the machinery that tells a pension fund exactly why it beat or missed its benchmark, and proves it to auditors. This is mission-critical, deeply regulated, and almost never ripped out. With BISAM, FactSet went from being the place asset managers gathered data to the place they measured themselves — cementing its grip on the steadiest, most defensible part of the workflow.

CUSIP Global Services (2022) — becoming the tollbooth. Then came the move we opened with, and it belongs in a different category entirely. For $1.925 billion, FactSet acquired the registry that administers the nine-character security identifiers required to clear, settle, and trade essentially every equity and debt instrument in North America.[^2] Every other acquisition made FactSet a better cleaner of data. CUSIP made it an owner of data — or more precisely, an owner of the identification standard itself. Anyone who stores or processes a CUSIP code pays a licensing fee, and there is no legal way to route around it because the codes are mandatory. Overnight, FactSet bolted a high-margin, recurring, monopoly-like cash stream onto a subscription software business. We'll examine whether the price was sane in the next section — and the litigation that now threatens it later — but strategically it was a transformation, not a bolt-on.

LiquidityBook (2025) — modernizing the front office. Finally, on February 7, 2025, FactSet closed its acquisition of LiquidityBook for $246.5 million in cash, funded from its revolving credit line.7 The logic here was that Portware, a decade on, was aging architecture in a cloud-native world. LiquidityBook brought modern, cloud-based order and execution management, plus a proprietary FIX network connecting to over 200 brokers and routing orders to more than 1,600 destinations across 80 markets.7 That network is the connective tissue of trading, and owning it pulls FactSet toward a genuine front-to-back capability — research, to portfolio construction, to order, to execution — inside one stack.

Step back and the pattern is unmistakable. Over fifteen years FactSet expanded from a research screen into execution, into performance and risk, into the identification layer of the entire market, and into the trading network itself. Each step deepened the switching cost and broadened the share of a client's workflow it controlled. But expansion-by-acquisition raises the obvious, uncomfortable question every disciplined investor must ask: did they pay too much?

V. M&A Analysis & Capital Allocation: Did They Overpay?

Let's put the acquisitions on the operating table, because the answer is genuinely different for each one, and the differences reveal how management thinks.

Start with the controversial one. FactSet paid $1.925 billion for CUSIP Global Services, a business reported to generate somewhere in the neighborhood of $175 million of annual revenue at the time of the deal.3 That works out to roughly eleven times revenue — and on the surface, eleven times revenue for a low-growth registry sounds like the kind of price that gets a CFO fired. Net of the tax benefits FactSet expected to realize, the effective multiple was a bit lower, closer to ten times. On an earnings basis, with CUSIP reportedly running at extraordinarily high margins north of sixty percent, the deal penciled out to something like high-teens times operating profit.

Is that overpaying? The case for "no" rests on a single word: irreplaceable. You cannot build a competing CUSIP. The identifier is embedded by mandate in the entire North American settlement system; a rival registry would have no users because no one is allowed to use a non-CUSIP code where a CUSIP is required. So the question isn't "what's a fair multiple for a data business growing at X percent" — it's "what's a fair multiple for a structurally protected, ~60%-margin annuity that immediately lifts your own operating margins and that will essentially never be for sale again?" Seen that way, the premium looks less like exuberance and more like the cost of a one-time opportunity. Compare the comps in the same era: S&P itself paid roughly ten times revenue for IHS Markit, and LSEG paid around four-and-a-half times for Refinitiv — but Refinitiv came with sluggish organic growth and required billions in restructuring to fix. By quality-adjusted standards, CUSIP was arguably the cleanest asset of the lot. The honest counter-argument, which we'll develop in the risk section, is that a price built entirely on a legal monopoly is only as safe as the legal monopoly — and that monopoly is now in court.

The other deals were more conventionally disciplined. BISAM, at $205 million on a business of roughly $28 million in revenue, came in around seven times sales — a restrained price for a category-leading, mission-critical analytics tool.6 Portware was the most speculative, dilutive at first and harder to value on day-one economics, but it bought a strategic foothold in execution that FactSet could not have built organically in any reasonable timeframe. The more recent deals — LiquidityBook in 2025, and the corporate investor-relations platform Irwin acquired around the same period — drew sharper skepticism. Critics argued FactSet was paying premium technology multiples, well into double-digit multiples of recurring revenue, and that the timing was suspicious: were these acquisitions genuinely strategic, or were they bolting on inorganic ASV to paper over a maturing organic story in the core workstation business, where seat growth was flattening? That is a fair challenge, and the only honest answer is that it depends on integration — on whether LiquidityBook's network and Irwin's corporate relationships actually compound, or just pad the top line for a few quarters. The jury is still out.

Now, the part of the capital-allocation record that is harder to argue with: what FactSet does with the cash the business throws off. The company has been a relentless retirer of its own shares — a "serial cannibal" in the old Henry Singleton sense — shrinking its share count from roughly 46 million in 2012 toward the high-30-millions by 2026, which mechanically boosts earnings per share even when net income grows modestly.[^16] It has also raised its dividend for more than a quarter-century, putting it in the rarefied company of long-duration dividend growers.[^16] And it demonstrated real financial discipline after the CUSIP deal: having borrowed about a billion dollars to fund the purchase, FactSet used its prodigious cash conversion to pay down a large chunk of that debt within a few years, rapidly de-levering and proving that the underlying business genuinely generates the cash its margins imply.[^16]

There's a second-order lesson hidden in the integration record that's worth drawing out. The market's instinctive reaction to a software company doing serial M&A is suspicion — most acquisitive tech roll-ups eventually trip over integration, culture clashes, and goodwill write-downs. FactSet's defense is that its acquisitions have largely been workflow-adjacent: each target slots into a step the client already performs near FactSet's existing footprint — execution sits next to research, attribution sits next to portfolio data, CUSIP sits underneath everything. That adjacency lowers integration risk because the acquired product doesn't have to be bolted onto an unrelated business; it has to be wired into a workflow the company already understands intimately. The contrast with a sprawling, unfocused roll-up is the whole point — this is acquisition as deepening rather than acquisition as diversification. The watch item, again, is the most recent vintage: LiquidityBook and Irwin are slightly further from the historical core and were bought at richer prices, so they are the truest test of whether the adjacency discipline still holds.

What does all this tell us about management? It says capital allocation has been, on the whole, rational and shareholder-friendly — disciplined buybacks, a reliable dividend, fast de-leveraging, and a willingness to swing big when a truly unique asset like CUSIP comes loose. The yellow flag is the recent drift toward pricier, smaller technology acquisitions at exactly the moment the core is slowing, which is precisely the kind of behavior that can quietly mask deceleration. Watching whether organic ASV growth holds up without the acquisition sugar is the single best test of whether this team is compounding value or just compounding the share count. And the people now making those calls are almost entirely new.

VI. Current Management & The "FactSet 2.0" Transition

For most of the last decade, FactSet was run by a lifer. Phil Snow joined the company in 1996 — the year it went public — worked his way up through the ranks, and became CEO in 2015. Under his tenure revenue roughly doubled and earnings per share compounded at a steady double-digit clip.8 He was the embodiment of FactSet's culture: methodical, client-obsessed, grown from within. So when the board decided in 2025 that the next chapter required someone from outside — and not just outside the company but outside the industry's traditional gene pool — it was a genuine statement of intent.

On June 3, 2025, FactSet announced that Snow would retire and that Sanoke Viswanathan would become CEO, effective early that September.8 This was not an internal promotion or a safe pair of hands. Viswanathan came from JPMorgan, where he had spent over fifteen years and risen to the top tier of the firm — he had served as Jamie Dimon's chief strategy officer and then run JPMorgan's International Consumer and Wealth business, where he was the architect of Chase's high-profile launch in the United Kingdom. He sat on JPMorgan's operating committee, one of a handful of people running one of the largest banks on the planet.8 The signal in his hiring was unmistakable: the board wanted a leader with deep banking-client relationships, a global perspective, and — above all — a technologist's instinct for the coming AI transition, rather than another data-industry insider.

Luring someone of that stature out of JPMorgan is expensive, because executives at that level walk away from enormous piles of unvested stock. To make Viswanathan whole, FactSet structured a make-whole package of roughly $49 million, consisting of about $13 million in cash and $36 million in restricted stock to replace the JPMorgan equity he forfeited.8 Make-whole packages are routine for senior external hires; the more revealing number is what FactSet did to align him going forward. The centerpiece of his incentive is a roughly $22 million performance-based stock-option grant — and here's the catch that should make investors sit up: those options only vest if FactSet's stock price reaches a hurdle of 150 percent of the grant price, a 50 percent appreciation, within five years.9 In other words, Viswanathan makes the big money only if shareholders make big money first. It is an aggressively pro-equity-holder structure that gives him every reason to push for stock appreciation — for better and for worse, since it also incentivizes bold swings. By mid-2026 he had also built a direct personal stake of over 58,000 shares, putting real money alongside the options.9

The second new commander arrived in the spring. On April 8, 2026, FactSet announced that Joshua B. Warren would become CFO, effective April 13, succeeding Helen Shan.10 Warren's résumé reads like a deliberate complement to Viswanathan's. He had most recently been CFO of Envestnet, where he led a sweeping transformation of the finance and operating functions — read: a margin-improvement program. Before that he was Global Head of Business Strategy for iShares and Index Investments at BlackRock, and earlier a managing director in BlackRock's corporate strategy and development team.10 Pairing a banking-and-tech CEO with a CFO who comes from the passive-investing heartland of BlackRock and who has a track record of squeezing out efficiency is a clear two-part message: drive margin expansion, and execute the newly authorized billion-dollar share-repurchase program. Notably, Warren's package back-loads his equity incentives into fiscal 2027 and beyond, again tying his payout to multi-year performance rather than a signing bonus.10

The real test of any management team, though, is not the press release — it's how they talk when analysts push back. On the second-quarter fiscal 2026 earnings call in March 2026, the new team was pressed repeatedly on a deteriorating-looking margin: adjusted operating margin came in at 35 percent for the quarter, down from 36.2 percent in the prior quarter and 37.3 percent a year earlier.13 A defensive management would have blamed macro. Instead, the answer was concrete: they are deliberately spending now — on cloud and technology infrastructure, on product development, on professional services — and accepting near-term margin compression because, in their framing, the terminal spend in the industry is shifting toward data-as-a-service and AI delivery, and they would rather invest into that shift than protect a hundred basis points of margin this year.13 On the call, Viswanathan repeatedly characterized these as "high-ROI investments." Whether that proves true is unknowable today, but the transparency is itself a data point: they named the trade-off rather than hiding it.

Equally telling was how they handled the hardest structural question. Asked about consolidation eroding the active buy-side customer base, the team did not pretend headcounts would rebound. The honest read of their answer was that buy-side seat counts are likely to stay roughly flat, which is why they are redirecting sales energy toward wealth management and toward data delivered through APIs and the new MCP channel rather than trying to force more workstation seats into a shrinking market.13 That is a realistic, non-promotional framing of the company's core challenge.

It's also worth scrutinizing what the new team is not doing, because absence can be as revealing as action. There has been no dramatic restructuring announcement, no splashy rebrand, no promise to "double revenue in five years" — the kind of round-number ambition that often precedes a stumble. Instead the early signals point to continuity of strategy with a sharper edge on execution: the same playbook of cross-selling data into existing clients, expanding in wealth, and investing in AI, but pursued with a banker's relationship rolodex and a passive-world CFO's instinct for cost. The genuine question marks are governance and culture. FactSet was, for decades, a company that grew its own leaders; importing a CEO from JPMorgan and a CFO from BlackRock and Envestnet is a deliberate break with that tradition, and integration risk runs in both directions — outsiders can bring fresh discipline, or they can misread a culture that worked precisely because it was idiosyncratic. The compensation structure also raises a legitimate governance point worth monitoring: an option grant tied to a 50 percent stock-price hurdle is squarely shareholder-aligned, but it also rewards aggression, and leaders chasing a vesting hurdle have been known to over-pay for acquisitions or over-stretch on buybacks.9 These are not red flags today; they are items on the watch list. What the early calls do establish is that the team explains its trade-offs in concrete terms rather than slogans — a reasonable proxy for credibility until the multi-year results arrive. And that sets up the two engines they're betting will carry the next decade.

VII. The "Hidden" Growth Engines: CTS and Generative AI

If the workstation is the FactSet that everyone pictures, the two businesses that actually matter most to the future are the ones nobody pictures at all. The first hides behind an unglamorous acronym, and the second is the most-hyped technology of the decade — and FactSet's relationship to it is more interesting than the hype suggests.

Start with Content & Technology Solutions, or CTS, which now represents on the order of a fifth to a quarter of total ASV and grows meaningfully faster than the workstation business.13 The premise is simple but powerful. Not every consumer of FactSet's data is a human staring at a screen. Increasingly, the consumer is a machine: a quantitative hedge fund's model, a bank's enterprise risk system, an internal data lake sitting in Snowflake or on AWS. CTS pipes FactSet's clean, structured data directly into those systems via feeds and APIs, bypassing the desktop entirely. Why does this matter so much? Because it severs FactSet's growth from headcount. If a client lays off ten percent of its human analysts — the exact structural fear hanging over the active buy side — its workstation seat count falls, but its machine appetite for clean data to feed models and dashboards keeps rising. CTS lets FactSet capture the data budget even as the human budget shrinks. On the Q2 fiscal 2026 call, management pointed to double-digit data growth across essentially every client type — banking, wealth, and the buy side — as evidence that this cross-sell still has substantial room to run within the existing client base.13 That's the most important strategic hedge the company has.

Then there's generative AI, where the prevailing Wall Street worry is that large language models will disintermediate FactSet — that if an AI can read SEC filings and clean data itself, who needs a premium data janitor? FactSet's response is to try to flip the threat into a toll. The key move was becoming, by its account, the first major financial-data provider to launch a functional Model Context Protocol server. In plain English: MCP is an emerging open standard that lets AI agents safely plug into an external data source and query it directly. Think of it as a universal, secure adapter between an LLM and a trusted database. FactSet's MCP Server, launched in December 2025, lets a hedge fund's AI agent — built on Claude, or Gemini, or any model — pull FactSet's structured, verified financial data in real time rather than guessing.13

Why does that matter to the investment case? Because the Achilles' heel of an LLM is hallucination. An AI analyst that invents a revenue figure is worse than useless on a trading desk; it's a liability. The only way to make an AI analyst trustworthy is to feed it clean, structured, governed data — and that is precisely what FactSet sells. By being early to MCP, FactSet positions itself not as the thing AI replaces but as the thing AI runs on. Management's framing is that AI converts a disruption threat into a seat-expansion and usage-based pricing opportunity: every bank's fleet of AI agents becomes a new consumer of FactSet data. There's early evidence the pitch is landing — on the Q2 call, management said the MCP Server had attracted over 120 actively engaged clients within months of launch and was the company's fastest-growing solution, and that 48 of its top 50 clients were already using at least three of its AI offerings.13

There is a quieter, nearer-term version of the AI story that may matter more than the headline MCP narrative, and it shows up in wealth management. Wealth is the channel where FactSet has been growing ASV at roughly ten percent — well above the company average — and it is also the channel where AI delivers the most obvious productivity win.13 A financial adviser's day is full of repetitive, document-heavy tasks: generating client proposals, summarizing earnings transcripts, building portfolio review decks. FactSet has been embedding AI tools — proposal generators, adviser dashboards, a "Transcript Assistant" that digests earnings calls — directly into the adviser's workflow, and management reported on the Q2 call that wins like a landmark UBS deal and an international private-bank proposal-generation mandate were driving that double-digit growth.13 The strategic insight is that wealth is still early in its digitization journey, which makes it a longer-tail opportunity than the already-saturated institutional market: there are far more financial advisers in the world than there are buy-side analysts, and each one is a potential seat. If FactSet can ride AI-driven productivity into the wealth channel, it has a genuine, demographically expanding new market to offset the flat-to-shrinking institutional buy side.

The appropriate investor posture on all of this is interested but unconvinced. The strategy is genuinely clever, the wealth traction is real, and the early MCP adoption numbers are encouraging. But "120 engaged clients" and "fastest-growing solution off a tiny base" are not yet "material revenue," and management has been careful — to its credit — to call this optionality rather than a current earnings driver. The bull case requires that MCP and data-as-a-service become the industry standard for financial AI and that FactSet captures usage-based economics from it. The bear case is more subtle and more dangerous: the same open standard that lets FactSet plug into a client's AI also lowers switching costs and invites cheaper data providers to plug in right beside it. For decades FactSet's moat depended partly on the friction of integration; if MCP makes every data source equally easy to connect and disconnect, that friction could fall for everyone, not just for FactSet. The company is betting that being first and being trusted will let it capture the new channel before the commoditization risk catches up. Which way that breaks is the single most important open question about the next decade. To weigh it properly, we need the analytical frameworks.

VIII. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question every long-term investor must: what, exactly, prevents a competitor from taking this business away? Hamilton Helmer's 7 Powers framework is the sharpest tool for the job, and FactSet has unusually clear claims to three of the seven.

The strongest, by a wide margin, is switching costs. We've described the mechanism — the thousands of Excel models hard-wired with FactSet formulas, the co-built workflows, the BISAM performance engines threaded through compliance reporting. The power isn't just that leaving is expensive; it's that leaving is risky, because re-creating years of models by hand invites the kind of error that can mis-price a trade or fail an audit. That converts a vendor relationship into something closer to embedded infrastructure, and it's the mechanical source of the mid-90s retention rate.1 Of all seven powers, this is the one FactSet most clearly possesses and most clearly controls.

The second is cornered resource, and it has a name: CUSIP. A cornered resource is preferential access to a coveted asset on terms others can't get, and a legally mandated, unduplicatable security-identification monopoly is about as cornered as a resource gets. Every North American securities transaction must reference a CUSIP; you cannot bypass it; and FactSet owns the registry.[^2] The crucial caveat — and we'll press it hard in the next section — is that a cornered resource granted by legal structure can be revoked by legal challenge, and that challenge is live.

The third is counter-positioning, the most elegant of FactSet's powers and the one that built the company. For decades FactSet positioned itself precisely against Bloomberg's expensive, all-or-nothing terminal — that roughly $27,000-a-year, take-it-or-leave-it status symbol. FactSet unbundled the desktop, sold lower-priced workstations and customizable packages, and won the junior analysts and middle-office teams for whom Bloomberg was simply cost-prohibitive. The reason this is counter-positioning and not mere price competition is that Bloomberg could not easily respond without cannibalizing its own premium, all-in pricing model — the very thing that makes Bloomberg so profitable. A challenger picks a model the incumbent can't copy without bleeding itself. FactSet did exactly that. The honest note is that this power is more historical than fresh; the price gap has narrowed over the years, and counter-positioning is a one-time conquest, not a renewable resource.

Now Porter's Five Forces, which reframes the same business as a competitive ecosystem. The threat of new entrants is very low — assembling, cleaning, and licensing decades of global historical financial data is a multi-billion-dollar, multi-decade barrier no startup can vault. The threat of substitutes is moderate: cheap software and open-source scraping can replicate basic data, and over time AI may compress the premium for simple data-cleaning, but neither can easily replicate high-end portfolio attribution, GIPS-compliant reporting, or CUSIP tracking. The two forces that genuinely bite are rivalry — Bloomberg, LSEG, and especially a resurgent S&P Capital IQ all want FactSet's analytics turf — and, most importantly, the bargaining power of buyers, which is high and rising. As active asset managers consolidate under relentless passive-fee pressure, the survivors get bigger, and bigger clients negotiate harder, pushing for bulk data discounts and enterprise deals rather than per-seat pricing. That single force — buyer power compounding as the customer base concentrates — is the thread that ties together every risk in the business. It's time to pull on it.

IX. Activist Stress Test & The Current Risk Radar

Imagine a sharp long/short investor building the short case in a pitch meeting. What would they put on the slide? Three things, and they're all serious.

First, valuation versus growth. FactSet has long traded at a premium forward earnings multiple — in the mid-to-high twenties — which is a rich price for a company whose organic ASV grows in the mid-single digits. In fiscal 2026 organic ASV plus professional services grew about 6.7 percent, with full-year organic ASV guidance implying roughly 5.4 to 6.7 percent.1 A skeptic's framing is blunt: you're paying a growth multiple for a GDP-plus grower, and any slip toward the low end of that range — or below it — could compress the multiple painfully. The bull rebuttal is that the recurring, high-retention, high-margin nature of the revenue justifies a premium. Both can be true; the point is that the stock has little margin for disappointment baked in.

Second, M&A as a mask for organic deceleration. We raised this earlier, and the activist would sharpen it: did management overpay for LiquidityBook and Irwin specifically to bolt inorganic ASV onto a workstation business whose organic seat growth is flattening? If the core is decelerating, the activist argues, the cash spent on premium-multiple acquisitions would have been better returned to shareholders through even more aggressive buybacks. The only refutation is execution — proof that the acquired businesses compound rather than merely pad — and that proof takes years to accumulate.

Third, and most acute, the CUSIP litigation. The crown jewel that transformed FactSet's financial profile is under direct legal attack. CUSIP Global Services, alongside S&P Global, the American Bankers Association, and FactSet, has been named in antitrust litigation alleging that the parties conspired for decades to eliminate competition in security identifiers, and that the licensing fees rest on dubious copyright claims — the core contention being that CUSIP numbers are essentially public identifiers that should not command monopoly licensing fees.11 A separate action brought by the Global Infrastructure Finance and Development Authority alleged that CGS abused its gatekeeping role over the CUSIPs needed to issue municipal bonds, seeking an injunction to force fair processing of applications.12 If courts ultimately rule that CUSIP cannot charge the way it does, the high-margin annuity FactSet paid nearly two billion dollars for could be structurally impaired. This is the single largest binary risk on the company's books, and it is precisely the risk that a price built on a legal monopoly always carries. It is a genuine overhang, and its resolution is not within management's control.

A fourth line of attack a careful skeptic would raise is the quality of the growth itself. FactSet reports impressive client-count gains — it added 98 net new clients in a single quarter to reach 9,101, and grew its user base past 241,000 — but management has been candid that much of that expansion comes from corporates, wealth managers, and private-equity firms rather than from its traditional, high-value institutional buy-side core.113 A wealth client win can mean signing thousands of advisers at a lower price per seat, which flatters user-count and client-count headlines while diluting average revenue per user. The skeptic's question is whether FactSet is genuinely expanding its addressable market or simply trading high-margin institutional seats for a larger number of lower-margin ones — growth that looks better in the metrics than in the margin line. The bull would counter that wealth is a land-grab worth winning on volume first and monetizing later. Both are plausible, and the mix-shift is precisely the kind of thing that won't be obvious for a few years.

Beyond the activist's challenges, two structural risks sit on the radar. The first is the active-to-passive migration — the slow tide that defines the whole bear case. FactSet's core customer is the active asset manager, and money has flowed for years out of active mutual funds and hedge funds into passive ETFs run by Vanguard and BlackRock. Passive vehicles need far fewer analysts per dollar managed, so the long-run trajectory points toward fewer buy-side seats. FactSet's own management has effectively conceded that buy-side headcounts will likely stay flat at best, which is the honest version of this risk.13 The second is AI disintermediation — the mirror image of the AI opportunity. If open or cheap AI models can scan filings and clean data at near-perfect accuracy, the premium FactSet earns specifically for cleaning could compress, even as its premium for proprietary analytics holds. The company's MCP bet is precisely an attempt to land on the right side of that line.

One further risk deserves a brief mention because it is structural to the business model rather than cyclical: data security and trust. FactSet's entire value proposition rests on being a governed, trusted source — the place a hedge fund stores two million proprietary research notes, the registry settling North American securities, the data feed wired into a bank's risk engine. A serious breach, a corruption of data integrity, or a high-profile error would damage the one asset FactSet can least afford to lose, which is credibility. For a company whose moat is partly "you can trust our numbers," cybersecurity is not an IT line item but a core franchise risk, and it is one reason management has flagged spending on cybersecurity and platform resiliency as a deliberate priority even at the cost of near-term margin.13 Whether the AI bet succeeds, and whether the trust franchise holds, together form the crux of the entire debate — and they point us toward the durable lessons of the story.

X. The Playbook: Durable Business & Investing Lessons

Pull back from the quarter-to-quarter and FactSet's forty-five-year arc offers a handful of lessons that travel far beyond financial data.

Lesson one: don't fight Microsoft — build on top of it. The single most consequential distribution decision in FactSet's history was refusing to force users into a proprietary interface and instead becoming the live data layer inside Excel, the tool every analyst already lived in. Where Bloomberg made users come to its box, FactSet went to where the work already happened. The deeper principle: when a platform has already won the user's habit, the highest-leverage move is often to become indispensable within it rather than to compete against it. The same =FDS(...) formula that made the product useful made it nearly impossible to remove — distribution and moat in a single design choice.

Lesson two: service can be a product moat, not just a cost. By embedding bright, inexpensive consultants who actually build clients' models, FactSet turned the line item most companies try to minimize into its sharpest retention and acquisition tool. The lesson isn't "be nice to customers" — it's that deeply integrating your people into a client's workflow can manufacture switching costs that pure software cannot. The caveat for investors is that this is a labor-intensive moat; it doesn't scale with the costless elegance of software, and it's worth watching whether AI lets FactSet preserve the intimacy while shedding the cost.

Lesson three: the magic is in the middle office. The front office — traders, bankers, dealmakers — is glamorous, well-paid, and brutally cyclical. The middle office — risk, compliance, performance attribution — is boring, invisible, and mission-critical in every weather. By anchoring itself to that steady, regulated, deeply embedded layer through BISAM and its analytics suite, FactSet built revenue that holds up when the deal cycle collapses. For investors hunting durable compounders, "boring and essential" beats "exciting and cyclical" more often than the market prices in.

Lesson four: capitalize on antitrust disruption. Crown-jewel monopoly assets almost never come up for sale — except when a regulator forces a divestiture. FactSet's purchase of CUSIP is a textbook case of a company with a strong balance sheet standing ready to catch an asset that would otherwise be unattainable at any price, transforming its financial profile in a single stroke. The discipline that makes this possible — low leverage, high cash conversion, patience — looks like underperformance right up until the moment a once-in-a-generation asset shakes loose. The unfinished footnote, of course, is that an asset acquired because of antitrust can also be threatened by antitrust. Which brings us to the verdict.

XI. Summary & Bull vs. Bear Case

If you track only a few numbers on FactSet, track these three. First, organic ASV growth, which management guides toward the mid-single digits — this is the pulse of the subscription engine, and the cleanest read on whether the core is healthy without acquisition help.1 Second, adjusted operating margin, recently running around 35 percent as the company invests through the AI transition — the test of whether Viswanathan and Warren can convert AI and CUSIP into efficiency rather than just spending.13 Third, CTS / data-solutions growth, the double-digit grower that determines whether FactSet successfully shifts from selling human seats to selling machine-readable data.13 Those three, watched over several years, will tell you almost everything. A useful way to read them together: organic ASV tells you whether the franchise is alive, margin tells you whether the new management is disciplined, and CTS growth tells you whether the company is winning the transition that will define its future. If all three hold, the bull thesis is intact regardless of any single quarter's noise. If organic ASV slips toward the low single digits while margins compress, that is the combination that would validate the bear.

The bull case runs like this. Active management stabilizes rather than collapses, and FactSet captures a wave of seat expansion in wealth management — where it is already growing ASV around ten percent and winning large advisers — and in under-penetrated international markets.13 The AI bet pays off: FactSet's MCP Server becomes a de facto standard for financial AI, every bank's fleet of agents runs on FactSet's governed data, and usage-based revenue layers on top of subscriptions, converting the AI threat into the company's biggest growth driver in a generation. The CUSIP litigation resolves favorably, preserving a high-margin annuity that lifts the whole margin structure. In this world, the switching-cost moat holds, the premium multiple is justified, and a forty-five-year compounding streak extends well into its sixth decade.

The bear case is equally coherent. S&P's Capital IQ closes the analytics gap that was FactSet's whole reason for being, and intensifying competition plus consolidating, harder-bargaining buyers grind down pricing. The GIFDA and antitrust actions succeed in gutting the CUSIP pricing model, impairing the asset FactSet paid nearly two billion dollars for. And the structural bleed of active-management headcount forces FactSet into the trap it has so far avoided — cutting workstation prices to defend a shrinking seat base — producing years of margin contraction that no amount of buyback can offset. In this world, the premium multiple unwinds, and the quiet compounder is revealed to have been riding a cycle that finally turned.

Both cases hinge on the same two questions. Can FactSet convert AI from a disintermediation threat into a usage-based tollbooth before cheap models compress its data-cleaning premium? And does the legal monopoly under CUSIP survive contact with the courts? Everything else — the Excel lock, the middle-office franchise, the disciplined capital allocation — is real, proven, and durable. It is these two open questions, not the forty-five years of history, that will determine the next chapter.

XII. Outro

There's a pleasing symmetry in the timing. As we record this on June 28, 2026, it is exactly thirty years since FactSet rang the bell on the New York Stock Exchange, and forty-eight years since Howard Wille and Charles Snyder decided that the real bottleneck on Wall Street wasn't analysis — it was the drudgery of gathering the facts to analyze. Their first product was four pages of paper carried across Manhattan by a bicycle messenger. Their fateful decision was to refuse to build a box and instead pour themselves into the software and data running on everyone else's machines.

From that humble report grew something close to a quiet operating system for the buy side: the formulas inside the analyst's spreadsheet, the engine measuring the pension fund's performance, the network routing the trade, and — improbably — the registry stamping an identity on nearly every American security. FactSet never became the loudest name in its industry, and it never tried to. It became the indispensable one in a specific, defensible corner of it.

Is it one of the most underappreciated compounding machines in modern business history? The forty-five-year track record makes a powerful case. But the honest answer is that the company now sits at the first genuine inflection of its existence — a new outsider CEO, a shifting tide beneath its core customer, a legal challenge to its crown jewel, and a technology revolution that could either be its greatest threat or its greatest tailwind. Wille and Snyder bet that the work of turning messy data into usable facts would always be valuable. For forty-five years they were right. The next decade will test whether that bet survives the machines now learning to do the work themselves.

References

-

FactSet Reports Results for Second Quarter 2026 — GlobeNewswire / FactSet, 2026-03-31 ↩↩↩↩↩↩↩↩

-

Mergers: Commission clears acquisition of IHS Markit by S&P Global, subject to conditions — European Commission, 2021-10-22 ↩

-

S&P Global to sell CUSIP unit to FactSet for $1.93 bln — Reuters, 2021-12-27 ↩

-

FactSet — Wikipedia (company history: founding 1978, Wille and Snyder, NYSE listing 1996) ↩↩↩↩↩↩↩

-

FactSet Acquires Portware, Execution Management System (EMS) Provider — GlobeNewswire / FactSet, 2015-09-22 ↩

-

FactSet Acquires BISAM, Leading Performance Measurement Provider — GlobeNewswire / FactSet, 2017-03-20 ↩↩

-

FactSet Acquires LiquidityBook — GlobeNewswire / FactSet, 2025-02-10 ↩↩

-

FactSet Announces CEO Succession Plan: Sanoke Viswanathan to succeed Phil Snow — FactSet Press Release / SEC 8-K Exhibit 99.1, 2025-06-03 ↩↩↩↩

-

FactSet CEO Succession Form 8-K — CEO Agreement Exhibit, SEC, June 2025 ↩↩↩

-

FactSet Announces Chief Financial Officer Transition — Appointment of Joshua B. Warren, FactSet Press Release, 2026-04-08 ↩↩↩

-

S&P, FactSet, Banking Group Face Antitrust Suit Over CUSIP — Bloomberg Law, 2022 ↩

-

Munibond Issuer Takes Aim at CUSIP Global Services' Monopoly (GIFDA case) — FinOps Report / WatersTechnology, 2025 ↩

-

FactSet Research Systems Inc. Second Quarter Fiscal 2026 Earnings Call — Transcript and Webcast, 2026-03-31 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube