Globant S.A.: The Argentine Experience Engine

I. Introduction & Episode Roadmap

Picture Mountain View in 2006. Google is the most paranoid software company on the planet—a fortress built around a proprietary codebase so secret that engineers joke the search ranking algorithm is guarded like the recipe for Coca-Cola. The company has never let an outside vendor touch its core engineering. Outsourcing, in Google's culture, is something other companies do—slower companies, dumber companies, companies that have stopped believing they can build the future in-house.

And then a tiny, unknown firm walks in and wins Google's first-ever external software engineering contract. The firm is not from Bangalore. It is not from Silicon Valley. It is from La Plata, Argentina—a university town an hour outside Buenos Aires, in a country that had defaulted on its sovereign debt only a few years earlier in the largest such default in history at the time. The firm is barely three years old. Its founders had started it with roughly $5,000 and a conviction born in a bar.

How does that happen? How does a company conceived during an economic apocalypse end up writing software that powers Google, builds the digital nervous system of Walt Disney World, and runs reservation systems for Southwest Airlines? That is the story of Globant.

Today Globant S.A. trades on the New York Stock Exchange under the ticker GLOB. In fiscal year 2025 it generated $2.455 billion in revenue and employed more than 29,000 people—who, in a piece of branding that tells you everything about the culture, call themselves "Globers."[^1] For most of its public life, the market has valued Globant at a premium to the legacy IT giants of India, treating it less like a body shop selling cheap labor and more like a creative engine selling reinvention.

This episode is, at its heart, an investigation into three Acquired-style themes. The first is counter-positioning: how a Latin American upstart deliberately refused to fight the Indian giants on their own turf of legacy maintenance and ERP migrations, and instead invented a whole new category—"digital experience engineering." The second is the multiple-arbitrage consolidation engine: a disciplined machine that buys private services boutiques at one-to-two times revenue and folds them into a public vehicle the market values at four-to-six times revenue. The third, and the one that will decide whether Globant is a great business for the next decade, is the AI pivot: the gamble that Globant can stop selling hours and start selling capability through a new construct called AI Pods.

That last theme frames the core investment question. Every services company on earth is staring down the same existential threat: if artificial intelligence makes a software engineer thirty percent more productive, the client will eventually demand a thirty percent discount, and the entire revenue base erodes. Can a premium digital engineering firm escape that "services trap" by reinventing itself as something closer to a software platform—or will AI quietly commoditize the very thing it sells? Hold that question. We'll spend three and a half hours building toward it. But to understand how Globant thinks about reinvention, you have to start where the founders did: in the ruins of a collapsed economy.

II. The Bar in La Plata: Founding in the Ruins of the Peso

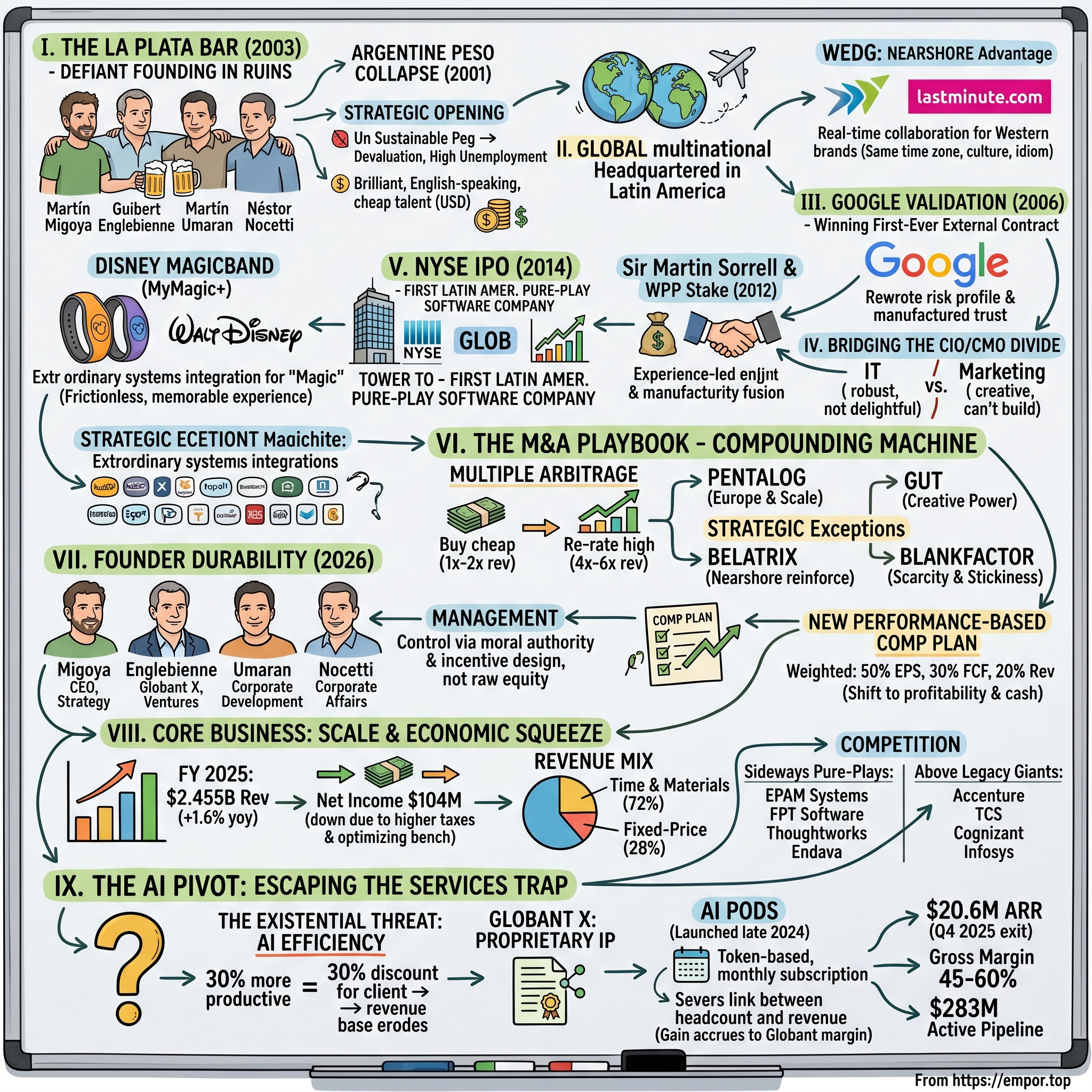

To understand Globant, you have to understand what it felt like to be a young, talented engineer in Argentina in December 2001. For a decade, the country had run a system called convertibilidad—the peso pegged one-to-one to the US dollar, a monetary straitjacket designed to kill the hyperinflation that had ravaged Argentina in the 1980s. For a while it worked. Then it didn't. The peg became unsustainable, capital fled, and the government, desperate to stop a bank run, froze citizens' deposits in a measure Argentines bitterly nicknamed the corralito—the "little corral." People who had dollars in the bank simply could not get them out.

What followed was one of the worst economic collapses in modern history outside of war. The government defaulted on roughly $100 billion of sovereign debt. The currency peg shattered, and the peso, once worth a dollar, eventually traded at a quarter of that. GDP cratered—the economy contracted by roughly eleven percent in a single year. There were five presidents in two weeks. Unemployment ran above twenty percent. For a generation of educated young Argentines, the message was brutal and clear: the local economy could not absorb your talent, and the local currency could not store your wealth.

Now—here is the strange alchemy. An economic catastrophe for a country can be a strategic opening for an entrepreneur who sees the world correctly. And sitting in a bar in La Plata in 2003 were four friends who saw it correctly: Martín Migoya, Guibert Englebienne, Martín Umaran, and Néstor Nocetti. All engineers. All products of Argentina's free, high-quality public university system, which for decades had been quietly minting world-class technical talent that the domestic economy could no longer pay world-class wages to.

Over beers, they did the arithmetic of their moment and arrived at two truths that would become the founding logic of the company. The first truth: Argentina was overflowing with brilliant, highly educated, English-speaking engineers who had grown up culturally fluent in American media and Western product sensibilities. The second truth: because the peso had collapsed, that talent was suddenly, dramatically cheap when priced in dollars. A company that could pay engineers in devalued pesos while billing clients in hard US dollars would enjoy a structural margin spread that no Silicon Valley firm could match.

But the genuinely contrarian decision—the one that separates Globant from the thousands of regional IT shops that came and went—was what they chose not to do. The obvious path was local: provide cheap IT support to Argentine banks and retailers, hunker down, survive the crisis. The four founders rejected that path entirely. Their ambition was almost absurd given the circumstances: to build a global multinational headquartered in Latin America, selling to the world's most demanding brands. They named the company by fusing "global" and "brilliant"—Globant—a name that was either delusional or prophetic, and for a long time nobody could be sure which.

Their wedge was a geographic insight that the industry had underrated for years: nearshore. The Indian outsourcing model required a US client to accept a nine-and-a-half-hour time difference—you wrote your requirements at the end of your day and got answers the next morning, a workable rhythm for back-office maintenance but a terrible one for the messy, iterative, collaborative work of building a consumer product. Argentina, by contrast, sits in roughly the same time zones as the United States. A Globant engineer in Buenos Aires could hop on a real-time call with a product manager in San Francisco at two in the afternoon for both of them. Same hours, similar culture, shared idiom—but at Argentine cost.

With about $5,000 of starting capital, they began hunting for proof that a high-end consumer software product could be built from South America.[^7] They found it in Europe, landing an early international contract with the British travel site lastminute.com—a real, recognizable Western consumer brand entrusting customer-facing software to a startup operating out of a country that had just defaulted on its debt. It was small. It was scrappy. But it was the first data point in a thesis that would soon attract the attention of the most demanding software buyer on Earth.

III. The Google Validation & Counter-Positioning the "Big Factories"

To appreciate the audacity of what Globant did next, you have to map the competitive landscape of offshore IT in the mid-2000s, because it was utterly dominated by a single, very specific business model. The kings were the Indian giants—Tata Consultancy Services, Infosys, and Wipro—and they had built something genuinely magnificent: industrial-scale software factories. Their genius was process. They could take an enormous, boring, mission-critical job—migrating a Fortune 500 company's ancient mainframe systems, integrating a sprawling SAP or Oracle ERP installation, maintaining millions of lines of legacy back-office code—and execute it with relentless, standardized, predictable efficiency across tens of thousands of engineers. They competed on three things: cost per hour, process maturity, and sheer headcount.

Here is the crucial strategic insight the four founders had, and it is a textbook example of what Hamilton Helmer would later call counter-positioning: Globant could never, ever win that war. A startup from La Plata was not going to out-scale Infosys on headcount or out-systematize TCS on process. To fight the giants on their chosen battlefield was suicide. So Globant chose a different battlefield entirely—one where the giants' greatest strengths became liabilities.

The giants were built for maintenance. Globant decided to sell innovation. The giants organized around verticals and back-office function. Globant organized around something it called "Technology Studios"—specialized centers of excellence in the emerging disciplines that legacy outsourcers barely understood: mobile, gaming, big data, user experience and interface design. The studio model was borrowed in spirit from Hollywood and from creative agencies, not from the IT body shop. When a client came to Globant, the pitch was not "we will maintain your systems cheaper." The pitch was "we will help you build something your customers will love."

This was a profound act of category creation. The Indian giants were locked into long-term, low-margin contracts maintaining the software equivalent of plumbing. Globant positioned itself one layer up, at the glamorous, high-margin surface where companies touch their customers—the app, the interface, the experience. And critically, this was a position the giants could not easily copy, because their entire org structure, sales motion, and cost-per-hour pricing were optimized for the opposite kind of work. Counter-positioning works precisely when the incumbent cannot respond without cannibalizing its own profitable core.

Then came the moment that turned a clever positioning into an unstoppable narrative. In 2006, Google came calling. Google's engineering problems were not the tidy, structured problems of ERP migration; they were sprawling, complex, unstructured challenges that demanded engineers who could think like product builders, not ticket-closers. Google needed collaborators who could work in real time, iterate fast, and understand the why behind the code. Globant pitched its nearshore, product-centric, studio-driven model—and won Google's first external engineering outsourcing contract.[^7]

It is hard to overstate what this did for a company barely three years old. In enterprise sales, the hardest thing to manufacture is trust, and the fastest way to manufacture it is borrowed credibility. Google was the ultimate trust certificate. The logic for every CIO and CTO in the Fortune 500 was devastatingly simple: if these Argentines are good enough to touch Google's sacred codebase, they are certainly good enough for ours. The Google deal didn't just win Globant a client—it rewrote the company's risk profile in the eyes of every buyer on the planet. A firm that might have been dismissed as "cheap South American labor" became "the firm Google trusts." That single reputational asset would open doors for the next two decades. But to walk through the biggest of those doors—the world of global brands and marketing budgets—Globant needed a different kind of validator. It needed someone who understood that technology was about to eat advertising.

IV. Sir Martin Sorrell & Bridging the CIO/CMO Divide

By the early 2010s, a tectonic shift was rumbling through the corporate world, and one man understood it better than almost anyone: Sir Martin Sorrell, the legendary, combative, relentlessly numerate founder and chief executive of WPP—then the largest advertising and marketing conglomerate on Earth. Sorrell had spent decades assembling an empire of creative agencies, the firms that made the beautiful television commercials and glossy print campaigns that defined consumer culture. But Sorrell could see the ground shifting beneath his industry. Marketing was no longer about a thirty-second spot. It was increasingly about software: the app on your phone, the website you shopped on, the personalized recommendation, the loyalty program, the seamless checkout. Technology was eating marketing.

This created a strange and lucrative gap in the market, and it sat right along an organizational fault line inside every large company: the divide between the CMO and the CIO. The Chief Marketing Officer controlled enormous budgets and understood brand, emotion, and consumer desire—but the marketing department couldn't write production-grade software. The Chief Information Officer ran the engineering and the systems—but the IT department often had no instinct for branding, delight, or consumer emotion. The traditional ad agencies could design something gorgeous they couldn't build. The traditional IT consultancies could build something robust nobody wanted to use. Globant, with its studio model fusing design and engineering, sat precisely in the gap.

In 2012, Sorrell made his move. WPP took a roughly 20 percent stake in Globant for approximately $70 million.[^7] For a young, private, Latin American software firm, having the most powerful man in global advertising write a check and lend his name was a second trust certificate, every bit as valuable as Google's—but pointed at a completely different audience. Google validated Globant to the world's engineers. WPP validated Globant to the world's brand marketers.

The strategic logic was elegant. WPP began injecting Globant into its global client relationships, positioning the Argentine firm as the "experience-led" engineering partner that could take a brilliant creative concept and actually ship it as working software. Globant was no longer just installing back-end servers in a basement; it was building the digital interfaces that millions of consumers would touch with their thumbs. The partnership fused two worlds that had always eyed each other with suspicion—Madison Avenue creativity and offshore engineering discipline—and Globant became the connective tissue between them.

The investment also turned out to be a financial home run for WPP, which is the kind of detail that, in hindsight, validates the whole thesis. WPP held its stake for years, riding Globant through its public listing, and eventually exited for more than $300 million—roughly quadrupling its money on a position it had taken for strategic, not purely financial, reasons.[^7] The capital relationship eventually unwound, but the strategic DNA did not. The conviction that engineering and creativity belong fused together—that you cannot separate how a product works from how it makes a customer feel—became permanently embedded in Globant's identity. It is the reason Globant would later spend hundreds of millions buying an advertising agency, a move that would baffle anyone who still thought of it as an IT shop. But before that, Globant had a bigger stage to step onto, and a billion-dollar wristband to help build.

V. The NYSE IPO & Disney's Billion-Dollar Wristband

On July 18, 2014, a bell rang on the floor of the New York Stock Exchange that carried a peculiar historical weight. Globant priced its initial public offering at $10.00 per share, valuing the company at roughly $400 million, and in doing so became the first Latin American pure-play software company to list on the NYSE.[^7] For a company born in a bar during a sovereign default, ringing the opening bell in Lower Manhattan was a fairy-tale milestone. But the romance, while real, was secondary to the strategy. The IPO handed Globant something far more useful than prestige: a publicly traded, high-multiple equity currency. As we will see, that currency would become the fuel for an acquisition machine that turned the stock itself into a tool for compounding.

But to understand what made Globant special in this era, forget the stock for a moment and walk into the Magic Kingdom. Because while the IPO was the financial coming-of-age, the Disney relationship was the artistic one—the project that proved, beyond any pitch deck, what "experience engineering" actually meant.

In the early 2010s, Bob Iger, the chief executive of Walt Disney, greenlit one of the most ambitious technology investments in the history of the leisure industry: a roughly one-billion-dollar bet to reinvent the theme park experience itself.3 Iger's obsession was friction. A day at Disney World was magical, but it was also a logistical grind—long lines, paper tickets, fumbling for a wallet, room keys, separate ride reservations, the constant small frictions that chipped away at the magic. Iger wanted to make the friction disappear. The initiative was called MyMagic+, and its physical centerpiece was the MagicBand: a sleek, colorful rubber wristband worn by every guest.

Here is the part that matters for our story, and it's the part most people get wrong. When the public marveled at the MagicBand, they marveled at the hardware—the wristband itself, the RFID chip, the radio that pinged sensors around the park. But the wristband was the easy part. The miracle was the software behind it, and a great deal of that complex back-end architecture was written by Globant's engineers.3

Think about everything that wristband had to do, invisibly, in real time. Tap it on your hotel door and the lock opens—so the band had to be wired into the hotel's physical security system. Buy a churro and just tap—so the band had to be linked to retail point-of-sale and your payment account. Walk toward a ride and a sensor recognizes you—so the band fed into crowd-routing and queue-management algorithms that could, in theory, nudge thousands of guests around the park to balance wait times. Reserve a slot on Space Mountain through FastPass+ and have it sync to the "My Disney Experience" mobile app—so the band, the app, the reservations engine, and the ride systems all had to speak to one another flawlessly. This is an extraordinary feat of systems integration. It is connecting hotel locks, payment rails, ride reservations, and location sensors into a single, seamless, invisible layer of magic. That is experience engineering, and Globant was building the nervous system.

The Disney relationship did something profound for Globant's brand and business. It proved that Globant didn't just build systems—it built memories. A child who taps a wristband and watches a door open like a wizard isn't experiencing an API call; she's experiencing magic. That emotional payload is exactly the thing the Indian factories could not sell, and it justified premium pricing.

Disney became, and has remained, Globant's crown-jewel client. The depth of that relationship is visible in the numbers more than a decade later: in fiscal year 2025, Disney was still Globant's single largest customer, contributing 8.7 percent of total revenue.[^1] That figure is a double-edged sword we will return to in the bear case—a relationship that deep is both an enormous asset and a concentration risk. But in 2014, with a fresh listing, a marquee creative engagement, and a high-multiple stock, Globant had everything it needed to build the machine that would define its next decade: a relentless, disciplined acquisition engine.

VI. The M&A Playbook: Benchmarking and Multiple Arbitrage

Most acquisitive companies destroy value. The corporate landscape is a graveyard of empire-building CEOs who overpaid for trophies, botched the integration, and diluted their shareholders into oblivion. So when you learn that Globant has acquired more than fifty companies over its lifetime, the natural reaction of any disciplined investor should be deep suspicion. And yet Globant's M&A engine has been, for most of its history, a genuine source of value creation rather than destruction. To understand why, you have to understand the beautiful, almost mechanical logic of multiple arbitrage.

Here is the trick, stated plainly. A small, private software-services boutique—say a 300-person firm in Romania with $50 million in revenue—is worth, on the private market, somewhere between one and two times its annual revenue. That's just what private services businesses fetch; they're seen as people-dependent, lumpy, and hard to scale. But Globant, as a beloved public company, has historically traded at four to six times its revenue. So watch what happens: Globant buys that private boutique for, say, 1.5 times revenue. The instant that boutique's revenue lands inside Globant's public income statement, the market re-rates it at Globant's multiple. Revenue that cost 1.5x to acquire is now valued at 5x. You have, almost by financial alchemy, created value out of the spread between the private and public multiple. Do this fifty times with discipline and you have built a compounding machine.

But—and this is the part the amateurs miss—multiple arbitrage only works if the acquired business doesn't fall apart after you buy it. Services firms are made of people, and people walk. So the second half of Globant's playbook is about retention and incentive alignment. Globant structures its deals with substantial contingent earn-outs, typically in the range of 20 to 30 percent of the total deal value, paid out over years and tied to the acquired business hitting performance targets. The founders of the acquired firm don't get all their money on day one; they get it only if they stay, integrate, and grow. The earn-out is a golden handcuff that turns a seller into a partner. This is the disciplined machinery that turns acquisitions from value-destroyers into value-creators.

Now let's benchmark the actual deals, because the pattern—and the deliberate exceptions to it—tells you exactly how Globant thinks.

Start with the textbook case: Pentalog, acquired in 2023 for total consideration of about $182 million.[^4] This was a classic scale-and-geography play—Pentalog brought more than 1,300 engineers across France, Germany, and Romania, deepening Globant's European footprint at the exact moment Europe was becoming its fastest-growing region. And the price was disciplined: against roughly $163 million of revenue, Globant paid about 1.1 times revenue.[^4] Right in the sweet spot. Buy cheap, re-rate high.

Then Belatrix, acquired in 2019 for about $65 million.4 This was a nearshore reinforcement—strengthening Globant's Latin American delivery muscle, its original home turf. Against over $35 million in revenue, the implied multiple was around 1.8 times—still firmly inside the standard range, paying a touch more for talent in Globant's core geography.4

But now look at two deals that deliberately broke the playbook, because the exceptions are where strategy lives.

The first is GUT, acquired in 2023 for roughly $245 million.2 GUT was not an engineering firm at all—it was the most awarded independent creative advertising agency in the world. Why on earth would a digital engineering company pay a quarter of a billion dollars for an ad agency? Because this was the WPP thesis, made permanent and brought in-house. Globant wasn't buying revenue at a services multiple; it was buying pure brand power and scarce, award-winning creative talent. It was doubling down on the creativity-meets-code intersection that had defined it since the Sorrell investment. You don't value the world's best creative agency on a revenue multiple any more than you value a Picasso on the cost of the paint.

The second exception is the most instructive of all: Blankfactor, acquired in 2024 for roughly $312 million.[^3] Blankfactor was a highly specialized, high-end payments and financial-services engineering firm generating only about $48 million in revenue. Run the math and the implied multiple is roughly 6.5 times revenue—an enormous premium against Globant's standard 1x-to-2x range.[^3] So the obvious question: did Globant overpay? Against industry comparables, unambiguously yes. But the strategic logic is where it gets interesting. Payments engineering is one of the scarcest, most defensible skill sets in all of software—it requires deep expertise in security, compliance, real-time settlement, and the byzantine plumbing of global finance. That talent is nearly impossible to build from scratch and almost as hard to poach. By buying Blankfactor, Globant instantly bought its way into high-margin, sticky, mission-critical contracts with tier-one global banks—relationships that, once embedded, are extraordinarily hard to dislodge. The premium bought scarcity and stickiness, not just revenue.

The Blankfactor and GUT deals reveal the sophistication of the engine. The base playbook is mechanical arbitrage—buy cheap services revenue, re-rate it. But the exceptions are strategic land-grabs: occasionally Globant will pay a steep premium when the asset is genuinely scarce and unlocks a high-margin beachhead that compounding alone could never reach. For an investor, the question to keep asking is whether each premium deal is a Blankfactor (scarce capability, defensible) or the beginning of the kind of overpaying that eventually catches up with every serial acquirer. So far, the discipline has held. But discipline is a function of the people enforcing it—which brings us to the founders, who, remarkably, are still very much in charge.

VII. Inside Globant Today: Current Management & Governance

Here is a genuine rarity in technology. Walk into most companies two decades after founding and a public listing, and the founders are long gone—cashed out, board-seated, off sailing or angel-investing, the company now run by professional managers and private-equity-trained operators. Now walk into Globant in 2026 and you find all four of the men from that La Plata bar still running the place. Not as ceremonial chairmen. As operators, in the seats that matter.

Martín Migoya remains Chief Executive Officer, the public face and chief strategist, the man who has narrated Globant's reinvention story to Wall Street for more than a decade. Guibert Englebienne, long the technical conscience of the company, runs Globant X and Globant Ventures—the innovation and investing arms where the company's future AI products are being incubated. Martín Umaran serves as Chief Corporate Development Officer, which—given everything we just learned about the M&A engine—makes him the chief architect of the acquisition machine. And Néstor Nocetti is Executive Vice President of Corporate Affairs. Four founders, four complementary roles, twenty-plus years later. That kind of founder durability is itself a soft asset; it means the original counter-positioning instinct—sell reinvention, not hours—still lives at the top of the house.

But founder control comes with a wrinkle that disciplined investors should understand, and it's a function of how the company financed its growth. To fund all those acquisitions and all that hiring, Globant raised capital repeatedly—and every raise diluted the founders. The four of them now collectively own only somewhere in the neighborhood of 2 to 2.5 percent of the company. To put a fine point on it: as of early 2026, Martín Migoya held a 0.49 percent beneficial ownership stake—roughly 211,040 shares—though his fully diluted potential stake, counting long-term restricted stock units vesting out through 2030, is closer to 1.23 percent, or about 533,283 shares.5 So the founders run the company through moral authority, board control, and incentive design far more than through raw equity ownership. That's a governance structure worth watching: their interests are aligned through compensation, not through a controlling block.

And the compensation design is where the recent governance story gets genuinely interesting, because it reveals a board responding to external pressure. Consider the short-term incentive plan, or STIP—the annual cash bonus for executives. It is tightly bound to hard corporate targets, principally non-GAAP operating income and revenue. And in the difficult environment of fiscal 2025, the board did something that ought to reassure shareholders worried about rubber-stamp pay: executive payouts were restricted to just 82.2 percent of target.5 When the business underperformed, the executives got paid less. That is the comp plan working as designed rather than as theater.

The more strategically revealing move came in the long-term incentive plan, which Globant overhauled in 2025. The catalyst was institutional pressure—Globant's shareholder base now includes serious, value-oriented institutions such as Brandes Investment Partners, holding roughly 7.93 percent.5 These are not momentum tourists; they are disciplined value investors who care intensely about cash and returns, not growth-at-any-cost. To satisfy them, Globant restructured its operational performance-based restricted stock units around three weighted metrics: 50 percent on adjusted earnings-per-share growth, 30 percent on free-cash-flow conversion, and 20 percent on year-over-year revenue growth.5

Read that weighting carefully, because it is a message in code. For most of Globant's life, the implicit incentive was growth—grow revenue, grow headcount, grow the empire through acquisitions. The new plan flips the emphasis decisively toward profitability and cash. EPS growth and free-cash-flow conversion together account for 80 percent of the operational weighting; pure revenue growth is down to a fifth. The board is, in effect, telling management: we no longer reward you primarily for getting bigger. We reward you for getting more profitable and generating hard cash. After two decades of building an empire through dilutive M&A, the owners have repointed the incentives toward discipline. Whether management can deliver that profitability is, of course, a question that lives entirely in the underlying economics of the core business—so let's go look at them.

VIII. The Core Business: Scale, Competitors, and Industry Economics

Let's open the books, because fiscal year 2025 was the year the music slowed down. For most of the prior decade, Globant had been a compounding machine, growing revenue at twenty-percent-plus rates year after year, supercharged by the great digital-transformation boom of the pandemic era, when every company on earth suddenly needed to ship software fast. In 2025, the record kept growing but the growth rate did not. Revenue reached a record $2.455 billion—but that was up just 1.6 percent year over year.[^1] After years of torrid expansion, Globant had hit a wall of macroeconomic caution, as enterprise clients tightened technology budgets and stretched out spending decisions.

The profit picture told an even sharper story of the squeeze. IFRS net income came in at $104.0 million, down meaningfully from $169.0 million the prior year.[^1] What caused the drop? Two things, and neither is the kind of catastrophic operational failure that should terrify a long-term investor, but both deserve attention. First, the effective tax rate jumped to 25.3 percent from 19.7 percent the year before—a significant headwind that has nothing to do with how well the business runs and everything to do with the shifting geography of where profits land.[^1] Second, Globant incurred "business optimization" costs—the polite phrase for restructuring, which in a services firm means right-sizing the "bench," the pool of engineers who are on payroll but not currently billing a client. When growth slows, the bench grows, and an idle engineer is pure cost. Trimming that bench costs money up front but protects margins later.

Now, how does Globant actually make money? This is worth slowing down on, because the revenue mix is central to the whole AI debate. The business sells engineering work two ways. The first, accounting for 72 percent of revenue, is Time & Materials—the classic services model, where Globant bills the client for the hours its engineers work, at a rate per hour.1 You sell elite engineering time by the unit. The second, at 28 percent of revenue, is Fixed-Price—where Globant commits to deliver a defined project for a defined price.1 Fixed-price work carries more execution risk (if the project runs long, Globant eats the overage), but it offers higher margin potential, especially when Globant can throw its own proprietary tools at the problem and deliver faster than the price assumed. Hold onto that 72 percent Time & Materials figure—it is the single number the entire AI bull-and-bear debate revolves around, because it is exactly the revenue most exposed to AI-driven efficiency.

Now let's war-game the competition, because Globant fights on two fronts at once. Above it loom the scaled legacy peers, the giants whose revenue dwarfs Globant's: Accenture at roughly $64 billion, Tata Consultancy Services at around $29 billion, Cognizant at about $19 billion, and Infosys near $18 billion. Globant cannot out-scale these companies; it competes by being more specialized, more design-led, more "premium." The more dangerous fight is sideways, against the digital pure-plays—the cohort Globant genuinely belongs to.

Survey that cohort and you understand Globant's exact position in the pack. At the top sits EPAM Systems, the undisputed king of scaled digital platform engineering, with roughly $5.46 billion in fiscal 2025 revenue and rebounding at around a 15 percent clip—more than twice Globant's size and growing far faster. Globant, at about $2.46 billion, is the Latin American experience leader, but it was visibly digesting a market slowdown with growth of only around 1.3 percent. Beneath Globant comes the hyper-growth threat from the East: FPT Software, the Vietnamese competitor at roughly $1.3 billion, wielding a massive, ultra-low-cost talent factory and growing rapidly—the same cost-arbitrage weapon Globant once wielded against the West, now pointed at Globant. Then Thoughtworks, around $1.0 to $1.1 billion, struggling through restructuring, heavy debt, and utilization problems after being taken private by Apax Partners—a cautionary tale of what happens to a premium brand when the growth stops. And Endava, near $980 million, growing modestly at about 4 percent, focused like Globant on Eastern European and Latin American nearshore delivery. The takeaway for an investor: Globant is squeezed. It is not the fastest grower in its peer group (EPAM and FPT are faster), and it is not the cheapest (FPT is cheaper). Its entire defense rests on being the most premium—the experience and creativity story.

The geography of the revenue, though, contains the most hopeful signal in the whole income statement. North America still drives the business—54.3 percent of revenue, about $1.33 billion.[^1] But the growth is happening elsewhere. Europe now contributes 19.1 percent of revenue, roughly $469 million, and growing fast—which is exactly what the Pentalog acquisition was designed to accelerate.[^1] And then there is the rocket in the corner of the statement: "New Markets," at 6.5 percent of revenue, about $159.5 million, and exploding.[^1] The anchor of that explosion is a lucrative push into Saudi Arabia, where Globant has hitched itself to رؤية 2030 Vision 2030—the kingdom's sweeping, state-funded program to diversify its economy away from oil through massive digital transformation. Government-funded transformation contracts in the Gulf are large, high-margin, and relatively insulated from the budget-tightening that has hit Western corporate clients. New Markets is small today, but it is the clearest growth vector in the portfolio—and a preview of the geographic-arbitrage bull case.

But geographic expansion alone doesn't answer the existential question. A faster-growing region full of Time & Materials contracts is still a region full of billable hours—and billable hours are exactly what AI threatens to make cheaper. To survive the next decade, Globant has to break the link between headcount and revenue altogether. That is the entire purpose of Globant X.

IX. Escaping the Hours Trap: Globant X and AI Pods

Let's name the monster directly, because it is the single most important strategic problem in the entire IT services industry, and Globant's answer to it is the whole investment case. In a traditional services business, your revenue is shackled to your headcount. Want to double revenue? Hire twice as many engineers. There is no operating leverage; growth is linear and labor-intensive forever. This is the "services trap," and for fifty years it has capped the valuation multiples of services firms relative to software companies, which can sell the same product a million times at near-zero marginal cost.

Now AI takes that chronic problem and turns it into an acute, possibly fatal one. Suppose an AI coding assistant makes a Globant engineer 30 percent more productive—she ships in seven hours what used to take ten. Wonderful for the world. Catastrophic for the business model. Because Globant bills 72 percent of its revenue by the hour, and the client is not stupid. The client will say: "If your engineer needs 30 percent fewer hours, I'll pay you for 30 percent fewer hours." AI efficiency, in a Time & Materials world, flows straight to the client as a discount and straight out of Globant's revenue. The very tool that makes Globant's engineers better could shrink Globant's top line. That is the existential crisis, and every investor in this sector should be losing sleep over it.

Globant's answer lives inside Globant X, the product incubator run by co-founder Guibert Englebienne, whose mandate is to build proprietary software—real, ownable intellectual property—rather than just selling labor. Two of its assets predate the AI panic and are worth understanding as foundations.

The first is GeneXus, a low-code development platform Globant acquired in 2022. Think of low-code as a tool that lets people build enterprise software by describing what they want at a high level, with AI and automation generating much of the underlying code automatically—dramatically less hand-coding. At acquisition, GeneXus was financially tiny, contributing roughly $30 million in revenue, only about 1.7 percent of Globant's total. So why does it matter? Two reasons. It gives Globant genuine, ownable AI-driven code-generation technology—a technical moat rather than a labor pool. And it came with a massive, loyal foothold in Japan, a notoriously hard market for foreigners to crack, where GeneXus had spent decades building deep enterprise relationships. The second asset is StarMeUp, a SaaS platform—originally an internal tool for cultural recognition and employee engagement—that Globant productized and now sells to external clients including Walmart and Santander. Small, but a proof point: Globant can build and sell software products, not just services.

But the asset that, in the company's own framing, represents the entire valuation case is AI Pods, launched in late 2024.[^11] This is Globant's frontal assault on the hours trap, and the design is genuinely clever. Instead of selling you a team of engineers and billing by the hour, Globant sells you an "AI Pod"—a cross-functional delivery unit that combines human engineers with specialized AI agents built on Globant's own proprietary software, working together as one productive unit.[^11] And crucially, Globant does not bill the pod by the hour. It sells the pod on a token-based, monthly subscription model.[^11]

Sit with why that pricing change is so radical. By moving to a subscription priced on tokens of capability rather than hours of human time, Globant severs the link between its revenue and its headcount. If an AI agent inside the pod does the work of three engineers, that productivity gain now accrues to Globant's margin instead of being handed to the client as an hourly discount. The efficiency that was an existential threat under Time & Materials becomes a margin tailwind under subscription. Same AI, opposite financial outcome—purely because of how it's priced. That is the whole idea.

What do the early numbers look like? As of exiting the fourth quarter of 2025, AI Pods had reached $20.6 million in annual recurring revenue—about 1 percent of total company revenue. Tiny. But the margin profile is the tell: AI Pods carry gross margins of roughly 45 to 60 percent, versus Globant's corporate average of around 38 percent. And the forward pipeline is the genuinely exciting figure—an active commercial pipeline of about $283 million heading into 2026. A 1-percent revenue line is, by itself, immaterial. But this is one of those cases where you have to value the slope, not the level. If that $283 million pipeline converts and the ARR compounds, Globant will have done something almost no services firm has ever managed: broken the linear chain between bodies and revenue, and re-rated itself from a services multiple toward a software-enabled-services multiple. AI Pods are small today and could fizzle. But they are, quite literally, the entire bull case in embryo—which is exactly why the strategic frameworks are worth running before we render judgment.

X. Strategic Playbook: 7 Powers & Porter's 5 Forces

Let's put Globant on the dissecting table and run it through the two frameworks every serious investor should keep in their back pocket: Hamilton Helmer's 7 Powers, which asks what protects this business from competition, and Michael Porter's Five Forces, which asks how attractive is the industry it lives in. The goal is not to award points; it is to locate, honestly, where Globant's durable advantages are real and where they are thin.

The 7 Powers Analysis

Counter-Positioning is Globant's foundational and most historic power, and we've watched it operate throughout this story. By pitching "reinvention and experience" to CMOs and CIOs precisely when Accenture and Infosys were locked into long-term legacy maintenance and ERP contracts, Globant occupied a position the incumbents could not attack without abandoning their own profitable core. The caveat for investors: counter-positioning is most potent during the disruption itself. As the digital-transformation wave matured and the giants built their own digital practices, this power has weakened from a moat into a head start.

Switching Costs are very high, and this is arguably Globant's most durable defensive power today. Once Globant's pods are woven into a client's core product lifecycle—Disney's guest-management systems, Santander's mobile banking apps—ripping them out is not a vendor swap; it is open-heart surgery on a live patient. The institutional knowledge of how those systems actually work lives inside the Globant teams. The operational risk of replacing them is so high that clients rarely try. This is what makes the revenue sticky and the marquee relationships endure for a decade or more.

Cornered Resource has evolved interestingly over time. In the early years, Globant's cornered resource was the high-quality, time-zone-aligned, English-speaking talent pool of Latin America—a genuine scarcity it got to first. But talent pools eventually get discovered and competed for; that early corner has eroded. Globant's bid for a new cornered resource is its proprietary AI intellectual property—GeneXus, plus tools like the code-comprehension engine Augoor and the AI-powered quality platform MagnifAI—technology that, if it genuinely makes Globers more productive than competitors' engineers, would be a resource rivals cannot easily replicate. The honest grade here is "moderate and unproven": the IP exists, but whether it confers a durable productivity edge is exactly what the next few years will reveal.

Scale Economies are moderate. At 29,000-plus employees, Globant can bid on enormous, multi-year global enterprise contracts that a boutique simply cannot staff or de-risk—but it is an order of magnitude smaller than Accenture or TCS, so it does not enjoy the largest scale advantages in its industry. It has enough scale to compete for big deals, not enough to win on scale alone.

Brand is high, and it is the power that does the most work in justifying Globant's premium. Globant is, in the industry's own shorthand, the "cool outsourcer"—the firm associated with Google and Disney rather than with back-office cost-cutting. That reputation, reinforced by a famously high Net Promoter Score around 83 and its status as a top employer-of-choice across Latin America, gives Globant pricing power with clients and recruiting power with talent. Brand is the shield against commoditization, and it is the single most important reason Globant has historically escaped being valued like a body shop.

Process Power is moderate. The "Agile Pod" culture—small, autonomous, cross-functional teams—is highly optimized and genuinely good, but it is the kind of organizational design that competitors can study and replicate over time. It's an edge, not a fortress. Network Economies are weak-to-nonexistent; the only real candidate is the internal data flywheel of the StarMeUp platform, and it's minor. Globant simply is not a network-effects business, and investors should not pretend it is one.

Porter's Five Forces Analysis

Threat of New Entrants is low. Anyone with a laptop and three friends can start an IT boutique—the bar mentioned this article. But scaling to 29,000 engineers, achieving the global delivery and security compliance that Fortune 500 procurement demands, and—hardest of all—earning the trust to touch a Google codebase or a Santander payment system: that is a barrier measured in decades, not dollars. The Google-validation story is, itself, a moat against newcomers.

Bargaining Power of Buyers is high, and rising. This is the force that hurt Globant in 2024 and 2025. When the macro tightens, enterprise clients hold the whip hand—they delay projects, demand discounts, and consolidate vendors. The deceleration to 1.6 percent revenue growth was buyer power made visible. Clients can always take work in-house or shop it to EPAM or Endava, and they know it.

Bargaining Power of Suppliers—meaning engineers—is moderate, and has shifted in management's favor. For years, the global tech-talent shortage gave engineers enormous leverage, bidding up wages and squeezing the nearshore spread. But two recent forces have handed some of that bargaining power back to corporate management: AI efficiency means each engineer can do more (so you need fewer of them), and industry-wide consolidation and slower hiring have cooled the once-frantic labor market.

Threat of Substitutes is moderate. The eternal substitute for any outsourcer is the client's own in-house engineering team. The newer, more insidious substitute is AI low-code platforms that let clients build software with far fewer outside engineers—the very technology that powers the hours-trap fear. Globant's strategy here is shrewd: rather than be disrupted by the substitute, it is trying to co-opt it, becoming a seller of low-code and AI capability itself through GeneXus and AI Pods. Better to sell the disruption than be killed by it.

Intensity of Competitive Rivalry is very high. This is the defining feature of Globant's industry, and we mapped it in the prior section: squeezed from above by Accenture and Cognizant, attacked from the side by EPAM, Endava, Thoughtworks, and the low-cost insurgent FPT Software. There is no comfortable, uncontested niche. Every dollar of Globant's revenue is fought for. Put the two frameworks together and a clear picture emerges: Globant is a good business in a hard industry, defended primarily by switching costs and brand, betting its future premium on whether proprietary AI IP can become a genuine cornered resource. That tension is exactly what the bull and bear cases argue over.

XI. The Investment Case: Bull vs. Bear

Every great investment debate comes down to a single fault line, and for Globant the fault line is almost poetic in its symmetry: AI is simultaneously the bull case and the bear case. The same technology that could re-rate Globant into a high-margin software-enabled franchise could also gut its core business faster than the new model can scale. Let's steelman both sides, because an investor who can only argue one of them doesn't really understand the company.

The Bull Case rests on three pillars, and the load-bearing one is the AI migration. If AI Pods scale from roughly $20 million in ARR toward $100 million and beyond—and that $283 million pipeline says it's at least plausible—then Globant accomplishes the holy grail of services: it breaks the headcount-revenue chain, captures AI's productivity gains as margin rather than surrendering them as discounts, and earns the right to be valued like software rather than like labor. A re-rating from a services multiple to a software-enabled-services multiple is, by itself, a thesis that could double the stock without any heroics in the core business. The second pillar is geographic arbitrage: the New Markets line, anchored by Saudi Arabia's Vision 2030, opens a vein of large, high-margin, state-funded government transformation contracts that are structurally insulated from the Western corporate budget cycle that has been the recent drag. The third pillar is consolidation dominance: a strong balance sheet lets Globant keep running its multiple-arbitrage machine, hoovering up high-quality but distressed boutiques—think of the premium assets shaking loose from a struggling, debt-laden Thoughtworks—at depressed valuations, exactly when weaker competitors can't. In downturns, the disciplined consolidator gets to go shopping.

The Bear Case answers each pillar with a knife. The central bear argument is the AI commoditization trap, and it is the mirror image of the bull's central hope. The fear is one of timing and speed: that clients armed with their own AI coding assistants realize they can shrink their outsourcing spend faster than Globant's AI Pods can scale to replace the lost revenue. Remember, 72 percent of revenue is still Time & Materials—still billable hours exposed to exactly this compression. If the legacy core erodes at, say, 10 percent a year while AI Pods are still a 1-percent revenue line, the math is ugly no matter how exciting the pipeline looks. The race between core erosion and new-model scaling is the whole ballgame, and the bear thinks the core loses the race. The second bear pillar is client concentration: Disney alone is 8.7 percent of revenue, and the broader book carries the usual services concentration in a handful of anchor accounts. Losing a Disney-scale relationship—to a competitor, to in-housing, or to a budget cut—would blow a hole in growth and shatter the premium narrative in a single quarter. The third pillar is the unwinding of the original magic: the nearshore spread. Globant's whole founding edge was paying engineers in a cheap currency while billing in dollars. If Latin American currencies strengthen, or domestic wage inflation runs hot, or talent costs simply rise as the region gets discovered, the structural margin spread that has subsidized everything compresses—and a premium priced-for-growth stock with compressing margins is a dangerous place to be.

So how should a long-term investor actually monitor which way this resolves? Forget the dozens of metrics in the quarterly deck. Zero in on the three that matter, in priority order. First and most important: AI Pods ARR and its growth trajectory. This is the number. It is the direct, quantitative scoreboard for whether the entire reinvention thesis is real. Watch whether that $20.6 million compounds toward and past $100 million, and watch how much of the $283 million pipeline actually converts. If ARR stalls, the bull case is broken regardless of anything else. Second: organic revenue growth, stripped of acquisitions. Because Globant grows partly by buying companies, reported revenue can mask what's happening in the underlying business. Organic, constant-currency growth re-accelerating from the ~1.6 percent trough back toward double digits would signal that buyer power is easing and demand is healthy; staying flat would confirm the bear's erosion fear. Third: gross margin. This is the ultimate referee of the whole AI war. If AI Pods and proprietary IP are genuinely working, the blended corporate gross margin should drift upward over time, away from that ~38 percent average. If AI is instead commoditizing the core and clients are clawing back the efficiency, gross margin will grind downward. Margin direction is the single cleanest read on who is winning the existential fight. Track those three, and you don't need the rest of the deck.

XII. Epilogue & Key Takeaways

Step back from the spreadsheets and the frameworks, and the deepest lesson of Globant is almost embarrassingly simple: brand is the only durable shield against commoditization. Run the counterfactual. Imagine the four founders had walked out of that La Plata bar in 2003 and built exactly what the moment seemed to demand—a firm selling cheap hours of Java coding from a low-cost country. That company would have been a commodity from birth. It would have been ground down by the superior scale of the Indian giants, then undercut by the even-lower cost of Vietnam's FPT, and finally automated into irrelevance by AI. It would not exist today. Globant survived and commanded a premium for two decades because it refused to sell hours. It sold experience and reinvention—Google's trust, Disney's magic, the fusion of creativity and code—and that intangible, emotional, brand-laden positioning is precisely the thing that cost-arbitrage and automation cannot easily replicate. When your product is a feeling, the race to the bottom can't reach you. That is the business lesson worth carrying out of this story.

The second takeaway is quieter but nearly as important: the historically underrated power of nearshore. For years the entire industry assumed the only axis that mattered in global delivery was cost—find the cheapest hour on Earth and sell it. Globant proved that time-zone alignment, cultural proximity, real-time collaboration, and shared product instinct are worth a real premium, especially for the messy, iterative work of building things customers love. Same hours, same idiom, adjacent culture—it turns out those were undervalued assets all along, and Globant built a multibillion-dollar company partly by pricing them correctly when no one else did.

And so we arrive back where we started, and the symmetry is the point. A company conceived by four friends over beers, in a country in free fall, that defaulted on its debt and froze its citizens' savings—a setting that should have produced survival, not ambition—instead produced a global digital powerhouse that writes software for Google, builds memories at Disney, and now stakes its entire future on whether it can teach machines to do what its engineers do, and sell that capability by subscription instead of by the hour. The next chapter of that story is genuinely unwritten. The AI gamble may re-rate Globant into something the services industry has never seen, or it may prove that even the coolest outsourcer cannot outrun the commoditizing force of the very intelligence it is racing to embrace. But the journey from a bar in La Plata to the floor of the New York Stock Exchange remains one of the great global technology stories of the twenty-first century—and it is, fittingly, a story about reinvention told by a company whose entire business is selling it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube