The Power Behind the Brain: The Story of Monolithic Power Systems

I. Introduction & Episode Roadmap

Picture the inside of an NVIDIA AI server rack in 2024. The headline act is the GPU — the Hopper, the Blackwell — a slab of silicon worth tens of thousands of dollars, glowing with the heat of a small space heater. But trace the copper backward, away from the GPU, and you arrive at a constellation of small, square chips clustered right beside it. These are voltage regulators, and their job is to take the relatively crude electricity flowing through the server and refine it into the impossibly clean, stable trickle that the GPU demands. Get it wrong by a few millivolts and the most expensive chip in the data center throws an error or melts.

For a remarkable stretch of the AI boom, when you looked at those regulators on NVIDIA's flagship boards, you were very often looking at Monolithic Power Systems silicon. That is the hook of this story. If NVIDIA is the brain of the AI revolution, MPS spent years as one of the primary companies feeding it — and the market rewarded that position by handing a company with under $3 billion in annual sales a market capitalization north of $30 billion.19

The central thesis is almost philosophically tidy. Monolithic Power is an asset-light analog chip designer — it owns no factories — that managed to challenge two of the most entrenched giants in all of semiconductors, Texas Instruments and Analog Devices, by doing something they were structurally reluctant to do: cram an entire power system onto a single piece of silicon. The company name is not branding fluff. "Monolithic" is the strategy. One chip, one die, where rivals shipped many.

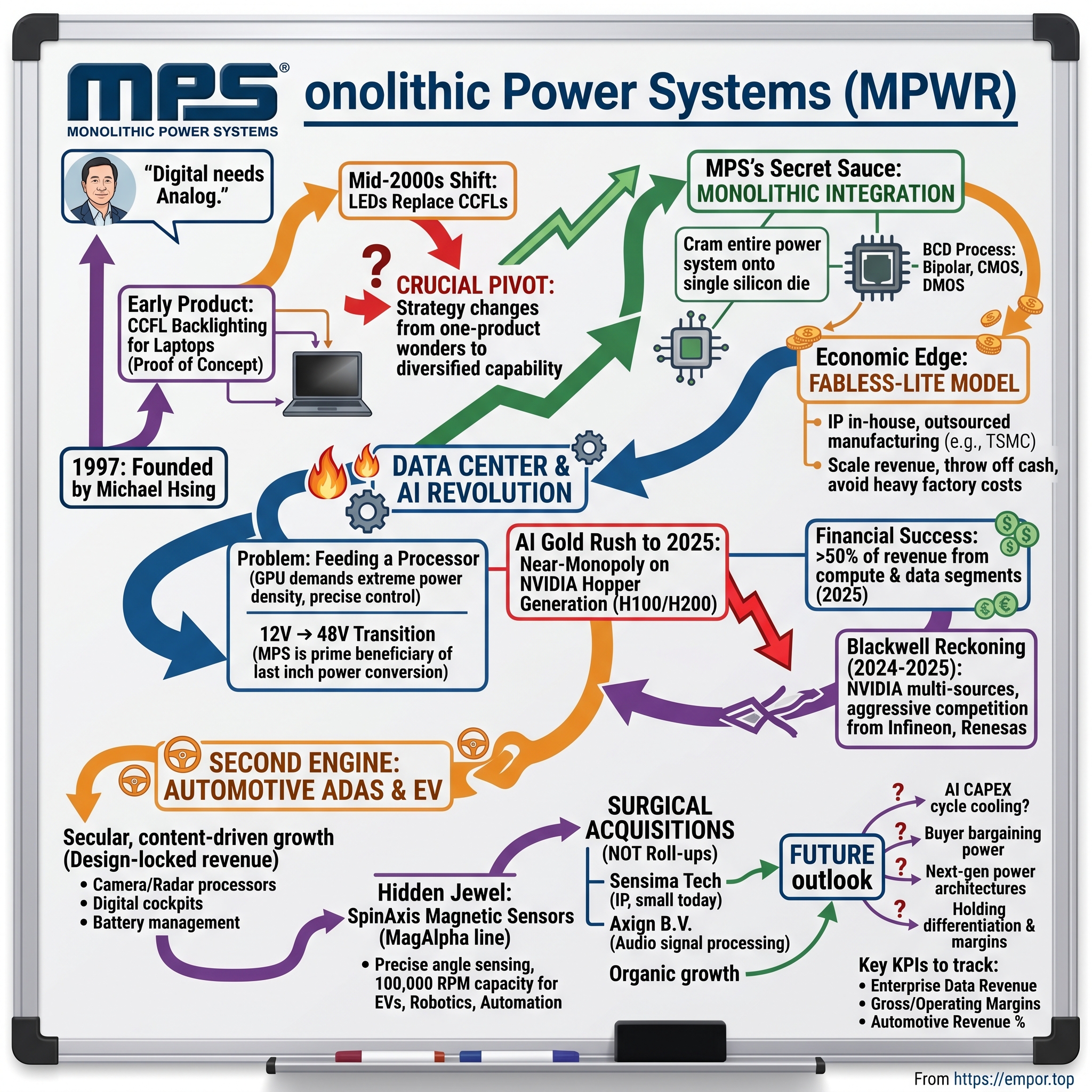

Here is the roadmap for where we are going. We will start in 1997 with a Taiwanese-American engineer who became convinced the entire industry was about to slam into a wall. We will trace the company from solving the deeply unsexy problem of laptop screen backlighting, through a near-death pivot when its first business went obsolete, into the data center and automotive markets that define it today. We will spend serious time on the AI gold rush — and on the painful plot twist of 2024, when MPS went from near-monopoly on NVIDIA's Hopper generation to one squeezed competitor among several on Blackwell. And we will dissect the capital allocation, the ownership culture, and the strategic moats that make this one of the more unusual compounding machines in public markets. Let us begin where every good origin story does: with a founder who saw something everyone else missed.

II. The Genesis: Michael Hsing and the "Monolithic" Dream

In the late 1990s, Silicon Valley was obsessed with the digital — microprocessors, memory, the relentless march of Moore's Law doubling transistor counts. Analog, the messy world of real-world voltages and currents, was treated as a sleepy backwater. It was precisely this backwater that 邢正人 Michael Hsing had spent his career in, and he had come to a conclusion that sounded almost contrarian: the digital revolution would eventually be held hostage by analog.

Hsing was an engineer's engineer, shaped by stints at two of the most respected analog houses of the era — Micrel and Linear Technology. Linear in particular was a temple of analog craftsmanship, a place where power-conversion chips were treated as fine art and gross margins ran at levels that made the rest of the chip industry envious. Hsing absorbed the craft but bristled at the orthodoxy. The orthodoxy held that to build a great power chip, you stitched together discrete components — a controller here, separate power transistors there, diodes and capacitors scattered across the circuit board — each optimized in isolation, then assembled into a bulky multi-chip package.

Hsing's insight was that this was a dead end. As processors grew hungrier and devices grew smaller, the discrete approach would become thermally inefficient, physically bloated, and electrically slow. Every connection between separate chips added resistance, lost energy as heat, and slowed the speed at which the power supply could react to a processor's sudden demands. His crazy bet, the bet that founded the company in 1997, was that you could integrate the high-voltage power transistors and the low-voltage digital brains that control them onto a single semiconductor die. One monolithic chip.

Why this was supposed to be impossible

To appreciate the audacity, you need to understand the manufacturing problem, and it helps to use an analogy. Imagine trying to build, on a single sheet of paper, both a delicate watercolor painting and a steel girder. High-voltage power transistors are the girder — big, brawny structures designed to shove large currents around and tolerate punishing voltages. Precision analog and digital logic are the watercolor — tiny, sensitive features that control everything with surgical accuracy. The fabrication processes for these two things actively fight each other. The heat and voltage tolerance you need for the girder tends to ruin the fine detail of the watercolor.

The reconciling technology is a mouthful: BCD, for Bipolar-CMOS-DMOS. Bipolar transistors deliver the high-precision analog. CMOS delivers the efficient digital control logic. DMOS delivers the high-power muscle. Cooking all three onto one wafer, reliably and cheaply, was the engineering problem Hsing and a small band of veteran analog engineers spent years grinding on. The recipe — the exact sequence of process steps, materials, and tweaks — became the company's crown jewel, a kind of proprietary cuisine refined over decades.10

The fabless-lite masterstroke

Here is where Hsing made the decision that would define MPS's economics for the next quarter-century. The analog giants — Texas Instruments, Analog Devices, Linear — were religious about owning their own factories. The conventional wisdom held that analog performance was so tied to manufacturing nuance that you could not possibly outsource it. Owning fabs meant owning your destiny; it also meant sinking billions into buildings and equipment that depreciated relentlessly.

Hsing did something heretical. He kept the secret sauce — the BCD process recipe — in-house as intellectual property, but he ran it on someone else's ovens, primarily the foundries of 台積電 TSMC.10 This is the "fabless-lite" model. MPS designs the chips and owns the proprietary process technology, but a third party bears the colossal capital cost of the factory. The result was a company that could scale revenue without scaling its balance sheet, throwing off cash and earning returns on capital that fab-owning rivals could only dream of.

It also created a subtle and durable moat, which we will return to: because the recipe lives at the foundry as a co-developed process, a competitor cannot simply buy the same machines and replicate it. They would have to reverse-engineer twenty-five years of accumulated tweaks. That insight — own the recipe, rent the kitchen — is the financial spine of everything that follows. But first, the young company had to find someone willing to pay for its chips at all.

III. Early Years & The First Crucial Inflection Point (1997–2010s)

Every elegant strategy needs a beachhead, and MPS's first one was, of all things, the dim glow of a laptop screen. In the late 1990s and early 2000s, portable computers and gaming systems were lit by cold cathode fluorescent lamps — CCFLs, essentially tiny fluorescent tubes tucked behind the display. Driving those lamps required a power chip that could take the laptop's battery voltage and step it up into the high-voltage alternating current the lamp needed, all while sipping as little energy as possible and fitting into a wafer-thin chassis.

This was a perfect proving ground for the monolithic philosophy. A backlight inverter built from discrete parts was bulky and ran hot; an integrated BCD solution was smaller, cooler, and more efficient. MPS won designs inside notebooks and handheld gaming hardware, and in doing so it proved the thesis in miniature: integration delivered higher power density in tighter spaces. Just as importantly, it earned the company something money cannot buy directly — a reputation among hardware OEMs, the engineers who decide which chips go into which products. In the chip business, that designed-in trust is the entire game.

The cash cow starts to die

Then the ground shifted. By the mid-2000s, the entire display industry began ripping out CCFL backlighting and replacing it with LEDs. LED backlights were thinner, more efficient, more durable, and they did not require the high-voltage drive circuitry that had been MPS's bread and butter. The company's primary commercial engine was, in the span of a few short years, being rendered obsolete by the very march of technology it lived on.

This is the moment that separates the one-product wonders from the durable franchises, and it is worth pausing on, because how a young company handles its first existential threat tells you everything about its DNA. Hsing did not bet the company on clinging to a dying standard, and he did not flail into unrelated markets chasing growth. He looked at what MPS actually owned — not "backlight expertise" but a world-class integrated power-conversion process — and asked where else that capability was needed.

The pivot to DC-DC converters

The answer was almost everywhere. He redirected the BCD process toward general-purpose DC-DC converters — the workhorse chips that take one voltage and efficiently convert it to another, a function required in virtually every electronic device ever made. A laptop needs dozens of them. So does a television, a server, a car, an industrial robot. By pivoting from a single dying application to a horizontal building block, MPS transformed itself from a notebook-backlight company into a diversified power management player, expanding methodically into consumer electronics, industrial systems, communications infrastructure, and the early innings of automotive.

The strategic lesson here is one that recurs throughout the MPS story: the company's true asset was never any single end-product. It was a process capability that could be repointed at whatever market was growing fastest. That flexibility is what allowed a 1990s backlight vendor to be standing, ready and credible, when the single largest demand shock in the history of power semiconductors arrived in the data center. Which is exactly where we go next.

IV. The Core Engine: Powering the Compute and Server Revolution

To understand why MPS became a name that AI investors learned to watch, you first have to appreciate just how absurdly difficult it has become to feed a modern processor. So let us start with the physics, in plain language, because everything financial flows from it.

Why processors are the world's pickiest eaters

A modern AI GPU is a glutton with the refined palate of a Michelin critic. It demands enormous quantities of electricity, but it will only accept that electricity at a very specific, very low voltage — often around 0.8 volts — and it wants that voltage held rock-steady even as its appetite swings wildly from moment to moment as computational loads spike and collapse. The power chips beside it must adjust their output in fractions of a millisecond. If the voltage sags during a sudden demand spike, the chip miscalculates or crashes. If it overshoots, the silicon can be damaged. Feeding a thousand-watt GPU is less like pouring a glass of water and more like keeping a fire hose perfectly aimed at a teacup, continuously, forever.

Now layer on a second problem: getting the power to the chip in the first place. Here is a piece of physics that quietly reshaped the entire data center industry. When you push electrical current through any wire, you lose energy as heat, and that loss scales with the square of the current. Double the current and you quadruple the loss. As AI racks ballooned to draw tens of kilowatts, the old approach of distributing power at 12 volts meant pushing monstrous currents through the boards, wasting enormous energy as heat before it ever reached the processor.

The 48-volt revolution

The industry's answer was to raise the distribution voltage from 12 volts to 48 volts. Because power equals voltage times current, delivering the same power at four times the voltage means one-quarter the current — and since losses scale with the square of current, those resistive losses drop by roughly sixteen times. It is one of those rare engineering wins that feels like cheating.

But there is no free lunch. Distributing at 48 volts means you now have to step that voltage all the way down to 0.8 volts in the final inch before the processor, efficiently, in a space barely larger than a postage stamp, while handling those violent current swings. This "last inch" of power delivery is brutally hard, and it is precisely the kind of high-density, high-speed conversion that MPS's monolithic integration was built for. A challenge that gave conventional discrete-component vendors fits was, for MPS, a home game.[^4]

Where the money actually is

Now follow the money, because this is the heart of the investment case. In fiscal 2025, Monolithic Power's revenue reached roughly $2.79 billion, up about 26% year over year — itself an acceleration on the prior year's growth.1 But the headline number matters less than its composition. The company reports by end market, and two markets now tower over the rest. Storage and Computing — the segment that captures much of the server and data-center compute demand — generated on the order of $732 million, while the Enterprise Data segment, the purest expression of AI data-center power, contributed roughly $702 million.2 Together these two buckets made up more than half of the entire company.

Let that sink in. A business that a decade earlier was diversified across consumer gadgets and industrial widgets had, by 2025, become majority-driven by the compute and AI data-center buildout. The growth in these segments through 2025 was eye-watering; in individual quarters, storage and computing revenue grew on the order of 70% year over year, and enterprise data climbed steeply on AI server demand.2 This concentration is the source of both the bull case and, as we will see, a meaningful chunk of the risk.

David among Goliaths

It is worth setting the scale honestly, because MPS is not the biggest fish — not remotely. Texas Instruments runs well north of $15 billion in annual revenue; Analog Devices comfortably north of $9 billion. Against those giants, MPS's $2.79 billion looks almost modest.1 The giants have vastly larger catalogs, deeper customer relationships across thousands of parts, and the financial muscle of in-house manufacturing.

What MPS has is not breadth but a sharpened edge: in the specific, high-value niches of power density, conversion speed, and customization, its monolithic architecture lets it pack more capability into less space and adapt a design for a demanding customer faster than rivals lugging around their discrete, multi-chip legacies. In a commodity slugfest, scale wins. In a knife fight over the last inch of a thousand-watt GPU, integration and speed win. For years, that knife fight is exactly what AI power delivery was.

The Hopper monopoly and the Blackwell reckoning

During NVIDIA's Hopper cycle — the H100 and H200 generation that ignited the generative-AI boom — MPS occupied an enviable position, supplying the voltage regulator modules that fed those GPUs as something close to the sole source. When demand for AI compute exploded, that near-exclusive position turned the enterprise data segment into a rocket, and it carried MPS's margins and stock to spectacular heights.[^4]

And then came the cautionary tale of customer concentration. As NVIDIA prepared the gargantuan ramp of its Blackwell generation — the B200 and GB200 — the calculus changed. No prudent buyer planning to ship power-hungry chips by the millions wants its entire power-delivery supply chain resting on a single vendor. The risk of a shortage, a yield problem, or simple pricing leverage is too great. So NVIDIA did what enormous buyers do: it multi-sourced, aggressively, and it qualified additional suppliers for Blackwell power.

The newcomers were not lightweights. Legacy heavyweights moved in hard. ルネサス エレクトロニクス Renesas Electronics and Infineon Technologies both secured significant allocations of Blackwell-generation power delivery, with supply-chain analysts at various points estimating that the bulk of certain Blackwell power modules had shifted toward these rivals — Infineon in particular leaning on its strength in higher-voltage, rack-level power architecture.[^4]4 Across the broader market, the top five VRM suppliers for GPUs and AI servers — Texas Instruments, Renesas, Infineon, MPS, and Analog Devices — collectively account for roughly 55–60% of revenue, a sign of just how contested this arena has become.3

When word of MPS losing Blackwell allocation circulated in late 2024, the stock was punished savagely, a vivid lesson in what happens when a market has priced in monopoly and reality delivers oligopoly.11 The takeaway for investors is sober but clarifying: MPS is no longer the lone gatekeeper of AI power. It is a formidable competitor in a multi-vendor, hyperscale market — still winning meaningful sockets, including on certain Blackwell boards, but fighting for every one of them. That shift from monopoly to brawl is the single most important strategic fact about the company today. And it is exactly why the second engine — automotive — matters so much.

V. The Second Engine: Automotive ADAS & EV Power Delivery

If the data center is where MPS's story turned dramatic, the automobile is where it turned diversified. And it is the segment that, more than any other, answers the bear's favorite question: what happens when the AI capex cycle cools?

Walk through any modern car and you are walking through a power-management problem disguised as a vehicle. The transformation underway in automotive is, at its root, the same one that hit computing decades ago — everything is becoming digital, and digital needs clean, precise, reliable power. Advanced driver-assistance systems run banks of processors crunching camera and radar data in real time. Digital cockpits string together multiple high-resolution displays. Electric vehicles manage enormous battery packs where a power fault is not an inconvenience but a safety event. Each of these systems has, in the words the industry likes to use, "zero tolerance" for power fluctuation, because the failure mode is not a frozen screen but a car that misjudges a lane or a battery that misbehaves.

This secular shift turned automotive into MPS's fastest-growing major non-compute business. In fiscal 2025 the automotive segment generated roughly $592 million, growing on the order of 40% or more year over year — in some quarters of 2025, automotive revenue grew more than 60% against the prior year.12 What makes this growth particularly valuable to the long-term story is its character: it is content-driven and design-locked. As cars add more electronics, the dollar value of MPS chips per vehicle climbs, and once a part is designed into a car platform it tends to stay there for the multi-year life of that model. It is growth that is less hostage to the boom-bust rhythm of the data center.

The hidden jewel: SpinAxis magnetic sensors

Tucked inside MPS's smaller Industrial segment — itself worth around $199 million, roughly 7% of revenue in fiscal 2025 — sits a business that punches well above its size in strategic interest.2 It is the company's magnetic position-sensing line, and it is a textbook example of optionality: small today, potentially material tomorrow.

The product is called MagAlpha, and it answers a deceptively simple question that turns out to be everywhere: how do you know, precisely and instantly, the angle of a spinning shaft? Electric motors, robot joints, steering systems, and countless industrial actuators all need to know exactly where their rotor is, right now, to control it smoothly. The traditional answer is the Hall-effect sensor, a decades-old workhorse that is reliable but comparatively slow — it lags, and at very high speeds that lag becomes a real problem.

MPS's MagAlpha line, which grew out of a small Swiss acquisition we will come to shortly, uses a proprietary phase-detection technology branded SpinAxis. Rather than measuring magnetic field strength the way a Hall sensor does, it detects the phase of the magnetic field, which lets it report shaft angle at extremely high resolution and with near-instant response, tracking speeds reported up to 100,000 revolutions per minute.58 In layman's terms: where the old sensor offers a slightly blurry photograph of where the shaft was a moment ago, SpinAxis offers a crisp live video of where it is right now.

Why does a power-chip company care about sensors? Because the fastest-growing, highest-performance electric motors — in EV drivetrains, in surgical robots, in factory automation, in the humanoid-robotics fantasies that increasingly excite the market — all need exactly this kind of fast, precise angle sensing to run efficiently. It is high-margin, it is sticky once designed in, and it positions MPS not merely as the company that powers a motor but as the company that senses and controls it too. It is a small line with a long runway, and it is the kind of quiet optionality that rarely shows up in a headline revenue number. It also happens to be the product of MPS's distinctive approach to acquisitions, which deserves a section of its own.

VI. Capital Allocation & M&A Strategy: The Art of the Surgical Buy

To understand how unusual Monolithic Power's approach to dealmaking is, you have to first appreciate how the rest of the analog industry grew up. The modern analog landscape was built through megadeals — enormous, debt-fueled, premium-priced acquisitions that consolidated the industry into a handful of titans.

The roll-up era

The poster child is Analog Devices, which went on a historic buying spree, acquiring Linear Technology for roughly $14.8 billion and then Maxim Integrated for around $21 billion — two of the largest deals the sector has ever seen.2 Renesas pursued a similar playbook across a string of acquisitions, taking in Intersil, then IDT, then Dialog Semiconductor, paying billions each time to bolt on capability and customers.2 These deals were not foolish; they bought scale, breadth, and entire engineering teams. But they came freighted with consequences: mountains of goodwill on the balance sheet, heavy debt loads, multi-year integration slogs, the ever-present risk of overpaying near a cyclical peak, and the messy human problem of fusing incompatible corporate cultures.

The MPS way

Monolithic Power looked at this and largely declined to play. For most of its history it has grown the hard way — organically, through internal R&D, funded by its own cash flow, carrying a pristine, essentially debt-free balance sheet. This is not an accident or a failure of ambition; it is a deliberate philosophy that flows directly from the fabless-lite, capital-light identity. Why take on billions in debt to buy a competitor's factories and overlapping product lines when your entire model is built on not owning factories?

When MPS does acquire, the deals look nothing like the roll-ups. They are small, cheap, technology-first, and meant to be absorbed rather than bolted on. Two examples define the pattern.

The first is Sensima Technology, a tiny Swiss firm spun out of the orbit of EPFL, the elite Lausanne engineering school, which MPS acquired in 2014. Sensima brought no meaningful revenue and no factories — it brought magnetic-sensing intellectual property. MPS took that IP, ran it through its own engineering and go-to-market machine, and grew it into the MagAlpha and SpinAxis product line we just discussed.25 A modest purchase of pure technology, patiently scaled into a profitable, strategically important franchise.

The second is Axign B.V., a Dutch fabless startup MPS acquired in 2024. Axign's specialty was digital audio signal processing — technology for driving speakers with extremely low distortion, valuable in automotive and high-end consumer audio.2 Again: small, capability-focused, designed to extend what MPS can offer its existing customers rather than to buy a chunk of market share.

The verdict on this approach is best understood through the lens of returns on invested capital. The roll-up giants deployed tens of billions and now carry the goodwill and integration overhang that comes with it. MPS deployed comparatively trivial sums on targeted IP and compounded them organically. For a company of its size, MPS has generated returns on capital that sit near the very top of the semiconductor industry — the natural arithmetic of growing revenue rapidly while keeping the asset base, and the share count discipline, tight. It is capital allocation as an extension of identity rather than as empire-building. And that identity, it turns out, traces straight back to one man who still runs the place.

VII. Current Management Profile & Ownership Culture

There is a particular kind of company that bears the unmistakable fingerprints of a single founder decades after its founding, where the culture, the strategy, and even the temperament of the firm seem to extend directly from one person's personality. Monolithic Power is one of those companies, and the person is Michael Hsing.

Nearly three decades after he founded MPS in 1997, Hsing remains Chairman, President, and CEO — an extraordinary tenure in an industry where founders are typically long gone by the time a company reaches this scale.6 Those who have worked with him describe a leader who is relentlessly engineering-centric, demanding to the point of being exacting, and almost allergic to short-term thinking. He runs MPS less like the multibillion-dollar institution it has become and more like the scrappy startup it once was — flat, fast, technically obsessive, suspicious of bureaucracy. That founder-driven agility, preserved at scale, is itself a competitive asset; it is why MPS can re-point its process at a new market faster than a committee-run giant.

Skin in the game

The phrase investors love — "alignment" — is often hand-waved. With Hsing it is concrete. He personally holds a very large stake in the company he built, in the neighborhood of roughly 2% of all shares outstanding, a position that as of recent disclosures amounted to well over a billion dollars of personal wealth tied directly to the stock price.6 He is not a hired manager collecting a paycheck and a sliver of options; he is, in the most literal sense, an owner who happens to run the company.

The behavioral consequence is the entire point. An executive whose net worth is dominated by his own company's equity tends to make decisions on the time horizon of an owner, not a quarterly-bonus optimizer — favoring durable R&D, balance-sheet conservatism, and the kind of patient, organic growth that has defined MPS. Hsing does periodically sell shares, but he does so through pre-scheduled Rule 10b5-1 trading plans — the mechanism that lets insiders diversify on autopilot without trading on inside information — while retaining an enormous core position.6 The selling is liquidity; the holding is conviction.

Paid only to win

The compensation structure reinforces the same philosophy with almost unusual purity. The overwhelming majority of Hsing's annual pay is "at-risk" — performance-based rather than guaranteed salary — and the performance awards are tied to genuinely demanding, multi-year operating metrics.6 His equity awards vest based on rigorous targets measured over three-year windows: revenue growth, operating margins, and total shareholder return measured relative to peers, not in absolute terms.6

That relative-return design is the detail worth dwelling on. It means Hsing does not get richly rewarded simply because a rising semiconductor tide lifted all boats; he is paid handsomely only if MPS outperforms its competitors over a sustained horizon. It is a structure that explicitly punishes coasting. Shareholders, in turn, have largely endorsed this; the company's "say-on-pay" advisory votes have run strongly in favor in recent years.6 When you combine a founder-owner's billion-dollar stake with a pay package that only pays off through multi-year outperformance, you get an incentive structure pointed squarely at the long term. The question for any investor, though, is whether that aligned, capable management is steering a business with durable competitive advantages — or one whose moat is narrower than its valuation implies. That is a question for frameworks.

VIII. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the AI excitement and the founder mystique, and the question every long-term investor actually needs answered is brutally simple: what stops a competitor from taking this business away? To answer it rigorously, two analytical lenses are useful — Hamilton Helmer's 7 Powers, which catalogs the sources of durable competitive advantage, and Michael Porter's classic 5 Forces, which maps the structural pressures on an industry. MPS is an unusually clean case study for both.

Process Power: the primary moat

In Helmer's framework, the power that best describes MPS is Process Power — an advantage embedded in a company's way of doing things that competitors cannot replicate quickly even if they know it exists. MPS's BCD process technology, refined and re-refined over twenty-five years and co-developed with its foundry partners, is the textbook example. A rival cannot simply purchase the same lithography equipment and produce the same chips, because the advantage does not live in the machines; it lives in the accumulated recipe — the thousands of process tweaks, design-process co-optimizations, and hard-won yield learnings layered on over decades.10 You cannot buy that on the open market, and you cannot reverse-engineer twenty-five years of tacit knowledge in a quarter. Crucially, because MPS runs this recipe at a third-party foundry rather than guarding it inside its own fab, the moat is paradoxically harder to attack — there is no factory to tour, no equipment list to copy.

Switching Costs: the lock-in

The second power, and it is a strong one, is Switching Costs. Power chips are not commodities dropped into a socket; they are designed in to the intricate architecture of a circuit board. When an automotive or AI-server customer selects an MPS regulator, its engineers build the entire board layout, thermal model, and reliability profile around that specific chip. Ripping it out to substitute a competitor's part means redesigning the board, re-running months of qualification and reliability testing, and re-validating thermal behavior — an expensive, slow, risk-laden undertaking. And the cost of getting it wrong is catastrophic: a power failure means a dead GPU worth tens of thousands of dollars, or, in a car, a safety recall. Faced with that asymmetry, customers are deeply reluctant to switch once designed in. This is the moat that produces MPS's enviable gross margins and its sticky, recurring revenue.

Where the moats thin out

But intellectual honesty requires noting where the powers weaken, and this is where Porter's lens sharpens the picture. The single most important structural force acting on MPS today is the bargaining power of buyers, and it cuts both ways depending on the market.

In AI, buyer power is enormous and growing. The Blackwell episode was a live demonstration: a buyer as colossal and sophisticated as NVIDIA can deliberately cultivate multiple suppliers, qualify them in parallel, and play them against one another to secure supply and squeeze price.[^4]11 When your customer is one of the most powerful companies on earth and it represents a large share of your fastest-growing segment, you do not set the terms — you negotiate them. This is the structural vulnerability beneath the AI growth story.

In automotive and industrial, the picture inverts. There, MPS sells into a fragmented universe of customers across thousands of designs, no single one of which holds decisive leverage, and where the multi-year design-in lock makes the relationships stickier still. The diversification into these markets is therefore not just a growth story; it is a deliberate hedge against the buyer power concentrated in AI.

The other dominant Porter force is rivalry, and it is fierce. MPS competes against Texas Instruments, Analog Devices, Infineon, and Renesas — well-capitalized adversaries with enormous catalogs and, in most cases, their own factories. The competitive equilibrium is a genuine trade-off: MPS wins on power density, integration, and speed of customization, while the giants win on sheer breadth of product line and the scale and supply security of in-house manufacturing.3 Neither side dominates outright, which is precisely why the AI power market settled into a multi-vendor brawl rather than a winner-take-all. The threat of new entrants, by contrast, is modest — the BCD process moat and the decades of customer trust are real barriers — and the threat of substitutes is low, because there is no way to run a processor without converting its power. The forces that matter, then, are buyer power and rivalry, and both are most acute exactly where the growth is hottest. That tension is the crux of the investment debate.

IX. The Bull vs. Bear Case & Core KPIs to Track

Every great business story eventually collapses into a single argument between two reasonable people looking at the same facts. With Monolithic Power, that argument is unusually well-defined, because the bull and the bear are not disputing the quality of the company — both concede it is excellent — but the durability of its position and the price the market has assigned to it.

The bull case

The bull starts with a simple observation: the total addressable market for AI server power is expanding so fast that even a shrinking slice of it can yield a growing dollar figure. MPS may have lost its Hopper-era monopoly, but it remains a qualified, design-won supplier into a market growing at a pace few industries ever see. A smaller share of an exploding pie can still be a much bigger meal than the whole of yesterday's pie.3[^4]

Beyond AI, the bull points to the automotive engine as a source of secular, content-driven growth that is far less cyclical and far less concentrated than the data center — every new vehicle platform embeds more MPS silicon for the life of the model, a steady compounding of dollars-per-car.1 Underpinning it all is the capital-light financial model: a fabless-lite structure that converts revenue growth into prodigious free cash flow, funds its own R&D, requires little reinvestment in physical plant, and leaves a debt-free balance sheet with the optionality to make more surgical, high-ROIC acquisitions. And threaded throughout is the optionality of newer lines like SpinAxis sensing, which the market arguably gets for free. This is, in the bull's telling, one of the most efficient compounding machines in the public market.

The bear case

The bear does not dispute the machine's quality — only its exposure and its price. The central worry is customer concentration and the pricing power of hyperscalers and NVIDIA. The Blackwell transition was not a one-off; it was a preview. When a vast share of your growth depends on a handful of enormous buyers who have proven both willing and able to multi-source and squeeze, your pricing power and your margins live on borrowed time.11

The second fear is share erosion in next-generation architectures. As AI power delivery moves toward ever-higher voltages and rack-level systems — the 800-volt architectures where rivals like Infineon have staked out leadership — there is a real risk that MPS gets out-engineered or undercut precisely where the next wave of value is created.[^4]4 Win the last generation, lose the next: it is the oldest way to die in semiconductors. And finally, the bear notes the unglamorous reality that MPS's consumer and standard industrial end-markets remain cyclical, prone to the inventory booms and busts that periodically wash through all of analog. A company priced for relentless compounding has little room for the ordinary disappointments that cyclicality guarantees.

Myth vs. reality

It is worth puncturing one consensus narrative directly, because it cuts to the center of the debate. The myth, peddled at the height of the AI frenzy, was that MPS was "NVIDIA's power company" — a near-permanent monopoly on feeding the world's most important chips. The reality, laid bare by Blackwell, is that MPS was the incumbent supplier on one generation and is now one strong competitor among several in a structurally multi-sourced market.[^4]11 That is a very different — and considerably more contested — proposition than the monopoly story the stock once priced in. Neither cartoon, "unassailable AI monopoly" nor "share-loser in terminal decline," survives contact with the evidence. The truth is a high-quality, capital-efficient franchise with genuine moats in process and switching costs, operating in markets where its two largest growth drivers also carry its two largest structural risks.

The KPIs that actually matter

For an investor tracking this story over time, the noise is endless but the signal narrows to a short list. Three metrics carry most of the information:

First, Enterprise Data segment revenue and its growth rate. This is the single cleanest read on whether MPS is holding, gaining, or ceding its share of the AI data-center buildout. It is the number where the entire Hopper-to-Blackwell drama plays out quarter by quarter, and it is where any further multi-sourcing damage — or any recovery of sockets — will show up first.

Second, gross and operating margins. MPS has historically enjoyed industry-leading gross margins in the mid-50s percent range, a direct readout of its differentiation and pricing power. The absolute level matters less than the trend: a sustained erosion in gross margin would be the earliest, clearest signal that competitive pressure from the giants is forcing MPS to compete on price rather than on integration — the moment the moat starts leaking.

Third, automotive revenue and its share of the total. This is the diversification gauge. As long as automotive keeps growing as a percentage of the whole, MPS is successfully building a more durable, less cyclical foundation beneath the volatile data-center business. If that diversification stalls, the company's fate becomes ever more tightly bound to the boom-bust rhythm — and the buyer power — of the AI capex cycle.

Track those three, and you are tracking the actual thesis rather than the daily noise. Which brings us, finally, to what the whole story means.

X. Epilogue & Outro

Step back from the segment tables and the supplier wars, and the Monolithic Power story resolves into a single, almost stubborn idea that one engineer carried for nearly thirty years. Michael Hsing believed, back when the industry was busy celebrating digital abundance, that the binding constraint on computing would ultimately be physical — that the limits of power, not the limits of logic, would dictate how far the machines could go. For most of his career that was a fringe conviction. In the age of thousand-watt GPUs and data centers straining the electrical grid, it reads as prophecy.

What makes MPS such an instructive case is not merely that Hsing was right about the physics. It is how he chose to be right. He built a proprietary process first and refused to build the factory to run it on, renting the world's best foundries instead. He pivoted ruthlessly when his first market died, repointing a capability rather than mourning a product. He grew through patient organic R&D and the occasional surgical acquisition rather than the debt-fueled empire-building of his peers. And he aligned himself with shareholders not through slogans but through a billion-dollar personal stake and a paycheck that only pays off if the company beats its rivals over years, not quarters. The result was one of the most capital-efficient compounding machines the public markets have produced in this era — a company that turned the unsexy business of voltage conversion into a position of genuine strategic consequence.

The road ahead is unmistakably harder than the road behind. The monopoly is gone, the giants are awake, the buyers are powerful, and the valuation leaves little margin for the ordinary stumbles that semiconductors always eventually deliver. Whether MPS extends its run will depend on whether its process moat and switching costs prove as durable in the 800-volt, multi-sourced future as they did in the 48-volt, single-sourced past — and on whether the second engine of automotive can grow fast enough to make the company less a hostage to the AI cycle and more its beneficiary.

But the deeper lesson outlasts any single product cycle. In a world fixated on the brain — on the processors, the models, the intelligence — Monolithic Power built an enduring franchise by obsessing over the unglamorous question of how to feed it. The brain gets the headlines. The power behind it, as this company spent a quarter-century proving, is where a surprising amount of the value quietly lives.

References

-

Monolithic Power Systems (MPWR) Revenue 2015-2025 — StockAnalysis ↩↩↩↩↩

-

Monolithic Power Systems SEC Filings (Form 10-K, 8-K, DEF 14A) — U.S. SEC EDGAR, CIK 0001280452 ↩↩↩↩↩↩↩↩

-

Power Delivery Module (VRM) Market for GPU and AI Servers — Mordor Intelligence, 2025 ↩↩↩

-

Power Semiconductors for AI Servers: NVIDIA Blackwell Architecture Analysis — Yole Group, 2024-12-05 ↩↩

-

MagAlpha Position Sensors & SpinAxis Technology Overview — DigiKey ↩↩

-

Monolithic Power Systems (NASDAQ: MPWR) 2026 Proxy, Board Changes and Pay — StockTitan ↩↩↩↩↩↩

-

MPS Official Position Sensors Product Catalog — Monolithic Power Systems ↩

-

Monolithic Power Systems 2024 Form 10-K — Monolithic Power Systems ↩↩↩

-

Monolithic Power Falls Amid Risk to NVIDIA Allocation, Edgewater Research Reports — Yahoo Finance, 2024 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube