ReNew Energy: The Architect of India's Green Transition

I. Introduction & The "Climate Infrastructure" Bet

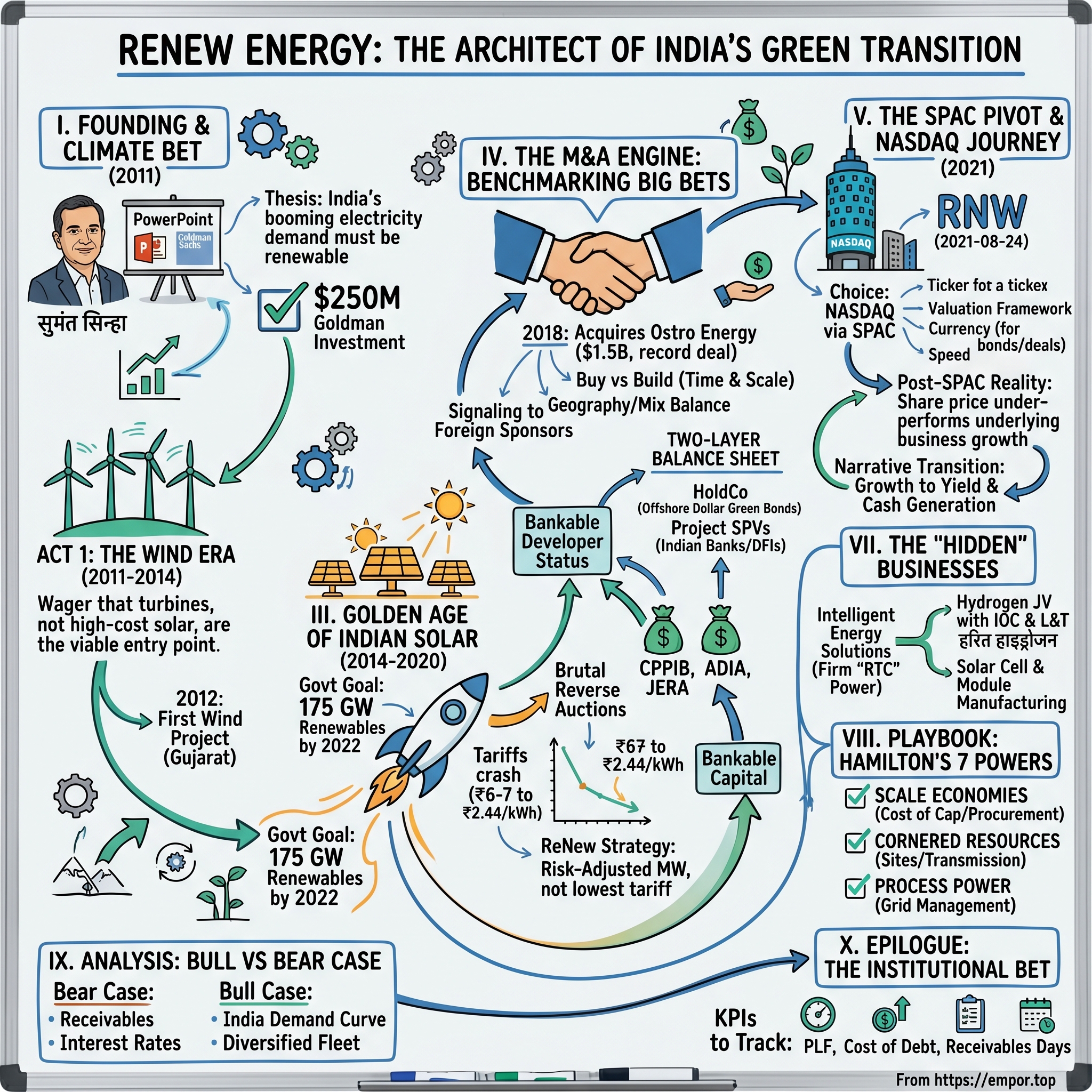

It is the spring of 2011, in a glass-walled office tower in Gurugram. A man in his mid-forties sits across from a row of Goldman Sachs bankers who have flown in from Singapore. He has no power plants. He has no land. He has no permits. He has a PowerPoint deck and a thesis.

The thesis goes roughly like this: India is going to consume electricity at a rate the world has rarely seen, the country cannot afford to do it on imported coal forever, and somebody is going to build the renewable energy fleet that powers the back half of the 21st century. He intends to be that somebody. He is asking Goldman to write him a check large enough to buy a mid-sized public company.

That man is सुमंत सिन्हा Sumant Sinha. The company he is pitching does not exist yet. It will be called ReNew, and within fifteen years it will be the largest pure-play renewable energy company in India, with a capacity portfolio that powers the equivalent of millions of homes and a shareholder register that reads like a who's who of global pension capital.[^1]1

To understand ReNew Energy Global Plc, you have to abandon the typical startup framing. This is not a software company that grew up. This is not a hardware company that pivoted. ReNew is a climate infrastructure company, born of high-finance DNA, scaled through aggressive capital markets engineering, and operated like a public utility decades before it was old enough to act like one. If TSMC is the foundry of global semiconductors and Aramco is the spigot of global oil, ReNew set out to be something equally elemental for India: the wholesaler of clean electrons.

The company's evolution has tracked a generational arc in three acts. Act one — the wind era, 2011 to 2014 — was a wager that turbines were the only renewables that could pencil out in a country where solar panels still cost three times what they would cost a decade later. Act two — the solar boom, 2014 to 2020 — was a punishing race down the cost curve that bankrupted weaker competitors and rewarded the players with the cheapest capital. Act three — the platform era, 2021 to today — is a quiet pivot from megawatts to intelligent megawatts: round-the-clock supply, green hydrogen, in-house manufacturing, and energy services.

The shorthand we will use throughout this piece is that ReNew became "the Goldman Sachs of Indian power." Not because of its founder's pedigree alone, but because the company turned the discipline of capital markets — yield, duration, cost of debt, refinancing windows — into an operating weapon in an industry that historically ran on relationships and bid-day bravado. While its peers fought over who could submit the lowest tariff, ReNew quietly negotiated who could lock in the cheapest dollar.

Three themes will keep recurring. First, asset-heavy scaling in a capital-starved economy: how do you grow a balance-sheet business in a country whose banking system has never been able to digest 20-year project debt? Second, the commoditization of megawatts: when everyone can build the same solar farm, what is the moat? Third, the geopolitics of the energy transition: India is at once a beneficiary of cheap Chinese panels and a hostage to Chinese supply chains, and ReNew sits squarely on that fault line.

By the time you finish this piece, you will see why the most interesting story in Indian renewables is not the headline tariff number. It is the slow, deliberate construction of a financial machine designed to outlast policy regimes, election cycles, and even its founder. Which is why we have to begin, of course, with the founder.

II. The Founding & The Goldman Inflection

In 2011, the conventional path for a man with सुमंत सिन्हा Sumant Sinha's résumé was not entrepreneurship. It was the corner office.

Sinha had assembled the kind of curriculum vitae that, in India, is described with reverent shorthand: IIT, IIM, Columbia. He had read chemical engineering at the Indian Institute of Technology in New Delhi, taken an MBA from the Indian Institute of Management in Calcutta, and then crossed the Pacific for an MBA at Columbia Business School. He had spent his early career in investment banking in New York, then returned to India and become Chief Financial Officer of the आदित्य बिड़ला Aditya Birla Group, one of the country's largest industrial conglomerates. He had been Chief Operating Officer of सुज़लॉन Suzlon Energy, then the world's fifth-largest wind turbine manufacturer at its peak.1[^12]

In other words, the man knew the energy industry from two sides that almost nobody else in India had seen together: as a financial engineer who structured project debt and as an operator who had walked turbine assembly lines. That combination — the spreadsheet and the gearbox — would prove to be the founding insight of the company he was about to build.

The personal stakes mattered. Sinha had a wife, two children, and a perfectly respectable job. He was leaving all of it to start a company in a sector that, in 2011, most Indian commercial banks did not know how to underwrite. Wind energy in India had been a niche tax-shelter business. Solar was a science project. The very phrase "green energy" implied luxury, philanthropy, or government largesse — not a venture-scale opportunity.

What Sinha saw that others missed was not the panels or the turbines. It was the curve. Cell-level solar costs had been falling at roughly twenty percent per year for two decades. Project finance was getting cheaper as global pension funds went looking for yield in a zero-interest-rate world. Indian electricity demand was growing in a way no developed-market grid had grown since the postwar United States. If you could put those three curves on the same chart, the picture was unmistakable. There was going to be a build-out. The only question was who would build it.

Enter Goldman Sachs. In 2011, the firm's principal investments arm wrote what would become a series of commitments to the still-blank-page company ReNew, eventually totaling roughly $250 million.[^4] In Indian venture terms, this was not a Series A — it was an asteroid impact. The largest Indian Series A rounds at the time were measured in the low tens of millions. Goldman was not betting on a startup; it was effectively underwriting a country thesis through a single CEO.

Why ReNew? Why Sinha? Goldman had a partial answer in its own institutional memory — the firm had been an investor in Suzlon and knew Sinha from his time there. But the deeper rationale was that Goldman wanted to deploy "sovereign-scale" capital into Indian infrastructure and could not find a vehicle. Government-backed power producers were politically encumbered. Private conglomerates were diversified across cement, telecom, and chemicals. ReNew offered something rare: a pure-play sleeve, with founder-CEO alignment, that would let a balance-sheet investor own the energy transition without owning everything else.

The early operating strategy that Sinha set was almost contrarian. In 2011, solar was the sexy story — modules were dropping in price, the global headlines were all about photovoltaics. ReNew built wind first. The logic was unsentimental: at then-prevailing tariffs and capital costs, solar projects in India did not clear an institutional hurdle rate. Wind did. The company commissioned its first wind project in 2012 in Gujarat. By the time the solar economics had truly inverted, ReNew was already a credible operator with bid-day muscle and an EPC track record.

That is the often-overlooked subplot of the founding years: ReNew was not just a financial play. It was an operating company that did the unglamorous work — securing land, navigating state electricity regulators, negotiating power purchase agreements with state distribution utilities — long before the boom that would make those skills indispensable. By the mid-2010s, Sinha had built the rarest thing in Indian renewables: a bankable developer.

Which set the stage for the next phase, when the Indian government would suddenly decide that renewable energy was no longer optional.

III. The Golden Age of Indian Solar

In 2014, India elected a new Prime Minister, and within a year the country's renewable energy ambition got an upgrade so dramatic it bordered on disorienting.

The previous Five-Year Plan had targeted 20 gigawatts of solar by 2022. The new government raised the bar to 100 gigawatts of solar and 175 gigawatts of total renewables by the same year — a roughly fivefold leap that almost no one outside the bureaucracy thought was achievable.[^10] To this day, the 175 GW number is the single most important data point in the modern history of Indian renewables, because every developer's strategy from 2015 onward was reverse-engineered from it.

The mechanism that the government chose to deliver this build-out was elegant in theory and brutal in practice: reverse auctions. The state would announce a tender for, say, 750 megawatts of solar capacity. Developers would bid the lowest tariff at which they were willing to sell that electricity for 25 years. Lowest bidder wins. There was no negotiation, no relationship lubricant, no second-prize consolation. It was a knife fight conducted on Excel.

For about three years, this worked beautifully for India and terribly for developers. Solar tariffs in India fell from roughly ₹6–7 per kilowatt-hour in 2014 to a record low of ₹2.44 per kWh in May 2017 — a collapse of more than sixty percent in three years.5 Headline writers globally marveled at India delivering some of the cheapest solar in the world. Inside the developer community, the mood was closer to despair. At ₹2.44, projects pencilled only if you assumed module costs would keep falling, debt would stay cheap, and the discom on the other end would actually pay you.

This is the bidding gauntlet ReNew had to survive, and the way it survived is the most important strategic lesson of the company's middle years. ReNew did not always win the lowest tariff. In several marquee auctions it deliberately did not. Instead, the company optimised for what bankers call risk-adjusted MW: projects with the right counterparty (preferably the central government's Solar Energy Corporation of India rather than a financially weak state discom), the right land position (already secured, not optioned), and the right interconnection (transmission lines that actually existed). In a race-to-the-bottom industry, ReNew tried to be the disciplined buyer.

The pay-off for that discipline was a second wave of capital — and this wave changed the company's gravitational pull. Between roughly 2016 and 2018, ReNew brought onto its cap table three of the most patient pools of capital in the world: the 加拿大養老金 Canada Pension Plan Investment Board (CPPIB), the Abu Dhabi Investment Authority (ADIA), and Japan's JERA, the country's largest power generator and a joint venture of 東京電力 Tokyo Electric Power and 中部電力 Chubu Electric.3[^12]

Why does this matter so much? Because in an industry where the cost of capital is the product, ReNew suddenly had access to a cost of capital that local Indian rivals could not match. A pension fund underwriting a 25-year PPA at a 7% dollar IRR will outbid a domestic developer financing the same project at 11% rupee debt, every single time. ReNew became, in effect, a "global clearinghouse" for foreign yield-hungry capital seeking Indian electrons. The bidding strategy did not have to be the smartest; the funding stack just had to be the cheapest.

There is one more sub-plot worth flagging from this period. ReNew was simultaneously building a portfolio shape that few peers bothered with. The temptation in any bidding-driven industry is to chase whatever the latest auction is selling — if it is solar this quarter, build solar; if it is wind next quarter, build wind. ReNew instead consciously assembled a mixed fleet of wind and solar, with sites geographically distributed across तमिलनाडु Tamil Nadu, कर्नाटक Karnataka, राजस्थान Rajasthan, गुजरात Gujarat, and महाराष्ट्र Maharashtra. The reason was meteorological. Wind blows strong in India in the monsoon months; solar peaks in the dry months. A blended fleet generates more evenly across the calendar, which both raises plant load factor and, crucially, becomes the foundation for the round-the-clock power products that the company would later sell at a premium.

By the time the solar tariff war reached its bloodiest phase in 2018–19, dozens of Indian developers were quietly running out of equity, missing milestones, or selling assets at distressed prices. ReNew, capitalised by Goldman, CPPIB, ADIA, and JERA, was about to do the opposite. It was going shopping.

IV. The M&A Engine: Benchmarking the Big Bets

April 2018. The deal was front-page news in the financial press, and not just in India.

ReNew Power, as the company was then known, announced the acquisition of Ostro Energy — a renewable platform backed by Actis, the London-based emerging-markets private equity firm — for an enterprise value of roughly $1.5 billion. Reuters called it the largest M&A transaction in Indian renewable energy history at the time.2 It instantly added more than a gigawatt of operating and under-construction wind and solar capacity to ReNew's balance sheet.

To understand why this deal mattered, you have to recognise what ReNew was actually buying. Ostro was not a discount platform; Actis had built it carefully over four years and run a competitive auction. ReNew paid full enterprise value, with a price-per-megawatt that industry analysts at the time pegged in the high single-digit-million-dollar range — broadly in line with what Indian peers such as अदाणी ग्रीन Adani Green Energy and टाटा पावर Tata Power would have paid for comparable assets, and arguably above what some private capital sources would have underwritten on a greenfield basis.2

So did ReNew overpay? Probably, in a strict greenfield-vs-brownfield comparison. But that is the wrong frame. Three things made the Ostro deal a different category of bet.

First, time. Building 1 GW of renewable capacity in India from a standing start — finding land, winning auctions, signing PPAs, getting environmental clearances, financing, building, commissioning — would have taken three to four years. Buying it took six months. In a race to scale where the prize was the cost-of-capital advantage that came with size, twelve months was worth a meaningful premium.

Second, geography and mix. Ostro's portfolio strengthened ReNew's wind footprint precisely in the states where ReNew was thin, balancing the rapidly growing solar pipeline. The resulting combined fleet had a more attractive generation profile than either company had on a standalone basis — exactly the round-the-clock substrate referenced in the previous section.

Third, signaling. The Ostro acquisition told every other foreign sponsor in Indian renewables that there was now an obvious natural buyer. Private equity firms invest with an exit horizon. If you are a fund manager sponsoring an Indian renewables platform in 2018, you suddenly have a real, scaled, dollar-funded counterparty who can write a billion-and-a-half-dollar check. That makes the entire asset class more attractive to underwrite in the first place. ReNew was, in a sense, paying to be the consolidator the industry needed.

And consolidate it did. Across the subsequent two to three years, ReNew picked up additional smaller asset packages and project SPVs, often from developers who had won aggressive auctions before module costs rose and who could no longer finance the build-out. This is the unglamorous mechanic of every successful infrastructure roll-up: someone wins the auction, can't fund the project, and sells the half-built asset to a better-capitalised buyer at a price that lets the original developer survive and the buyer earn a marginally lower but still attractive return.

The capital structure that made all this possible is worth pausing on. By the late 2010s, ReNew had pioneered in India what was effectively a two-layer balance sheet. At the project SPV level, each operating plant was financed with non-recourse term loans, typically from a syndicate of Indian public sector banks and increasingly from international development finance institutions. At the holding company level, ReNew tapped the offshore dollar bond market with green bonds — debt instruments labelled and audited as funding "green" assets — that opened a deeper, cheaper, longer-tenor pool of capital than rupee debt could provide.4

The strategic genius here is subtle. The Indian banking system, dominated by public sector banks with concentrated exposure to power-sector loans gone sour, was perpetually nervous about lending to anything that smelled like a generator. But the offshore dollar bond market — buyers in Singapore, Hong Kong, London, New York — was hungry for ESG-labelled paper from emerging-market issuers with hard-currency cash flows. ReNew's PPAs were rupee-denominated, but its currency hedges and tariff structures converted them into something close to dollar-equivalent yield. That arbitrage between domestic banking caution and offshore ESG appetite was a quiet, durable edge.

By 2020, ReNew had become both the largest Indian renewables developer by capacity and one of the most active emerging-market green bond issuers in Asia. The natural next question — for Sinha and his investors — was what to do with this thing. Take it public on the BSE? IPO on the NSE? Or do something different.

They chose something different.

V. The SPAC Pivot & The NASDAQ Journey

In February 2021, the Financial Times broke the news: ReNew Power had agreed to merge with RMG Acquisition Corp II, a US-listed Special Purpose Acquisition Company, in a deal valuing the combined entity at approximately $8 billion.[^6] The closing followed later that year, and on August 24, 2021, shares of ReNew Energy Global Plc began trading on the NASDAQ under the ticker RNW.[^1][^2]

For Indian capital markets watchers, this was — and remains — one of the most unusual listing decisions in recent corporate history. India's domestic equity markets were buoyant. The BSE Sensex was setting record highs. ESG funds in Mumbai were starved for listed renewables exposure. By every conventional metric, ReNew should have listed at home, where it operated, where its assets lived, and where its brand recognition was deepest.

So why NASDAQ? Why SPAC?

The answer has three layers, each worth pulling apart.

Layer one is valuation framework. In early 2021, the public market multiple on global renewable energy pure-plays — names like NextEra Energy, Brookfield Renewable Partners, and the Iberian developers — sat at premiums that Indian markets were not yet willing to pay for clean energy assets. US-listed renewable peers traded at EV/EBITDA multiples comfortably above what Indian utilities had ever commanded. Sinha's team made the bet that ReNew would be valued as a global green-energy growth story in New York and as a regulated Indian power utility in Mumbai. The same EBITDA, two very different price tags.

Layer two is currency. Listing in dollars on NASDAQ gave ReNew a stock-as-acquisition-currency that worked in its dollar-denominated bond stack and in its dollar-thinking foreign investor base. It also avoided the regulatory friction of cross-border share swaps that an Indian listing would have entailed for its global sponsors.

Layer three is speed. The SPAC route in 2020–21 was, for the right kind of asset, materially faster than a conventional IPO. The deal got done in months instead of the year-plus that a typical Indian IPO road show and SEBI review would have required, in a window where global investor appetite for energy transition stories was at its absolute peak. ReNew, in effect, ran straight at the open window.

And then the window closed.

The SPAC market did not just cool in 2022; it collapsed. Hundreds of SPAC mergers from the 2020–21 vintage saw their share prices break issue. Retail and momentum money that had piled in during the boom rotated out, often at a loss. ReNew's stock was caught in the undertow. The company's underlying business kept growing — capacity additions on track, EBITDA expanding, PPAs being signed — but the share price spent the better part of 2022 and 2023 trading well below its de-SPAC reference price.[^1]

This is the part of the ReNew story that founders and operators tend to under-discuss in public, but that is the most instructive for investors. ReNew, mid-life, had to undergo a narrative transition. The 2021 pitch had been "Indian green growth at global scale." That worked when the market was paying for growth. By 2023, US investors no longer wanted to hear about growth stories with negative free cash flow. They wanted to hear about yield and cash generation.

To management's credit, the company adapted. The communication shifted, the capital-recycling story moved to centre stage, and the operating playbook tightened. ReNew began to talk publicly about a multi-year programme of refinancing project debt, partially monetising operating assets into yield-co-style vehicles, and recycling that capital back into greenfield growth and new businesses — the playbook of a mature infrastructure compounder rather than a venture-stage growth name.[^11][^15] Project-level debt has progressively been replaced or refinanced with longer-tenor green bonds and structured facilities at lower spreads, and Fitch and S&P have published rating profiles tracking the evolving leverage and coverage metrics.4

The strategic question that hovers over today's RNW shareholders is whether the market will eventually pay for that mature, cash-generative profile. The company's earnings updates through fiscal 2024 and 2025 have shown steady operating-capacity growth, expanding contracted EBITDA, and improving plant performance — but a share price that has trailed those operating improvements.[^2][^8] Bridging that gap is the central preoccupation of the current management team.

Which brings us to who, exactly, is running the place now.

VI. Current Management & Governance

Walk into ReNew's Gurugram headquarters and you encounter something that is half investment bank, half engineering firm. The corridor outside the founder's office is lined with photographs of wind farms in कच्छ Kutch and solar projects in भादला Bhadla, and the meeting rooms are named after rivers. The vibe is intentional. Sinha has spent a decade trying to fuse the cultures of high finance and heavy industry inside a single company, and the architecture of the office is part of that effort.

Fifteen years in, Sinha occupies a role somewhere between founder-CEO and chairman-architect. He has been a visible public figure in the global climate conversation — he served as chair of the energy transition working group of the B20 Business Twenty business forum during India's G20 presidency, and he is a familiar face at the annual संयुक्त राष्ट्र COP United Nations climate conferences — and he uses that platform to position ReNew internationally.[^12] But on a day-to-day operational basis, his leadership style has matured into what insiders describe as "founder-plus-professional": he sets the long-range capital allocation strategy, but the company is increasingly run by a deep bench of professional executives in finance, engineering, and operations.

That professionalisation is itself a strategic choice. In a founder-led Indian conglomerate, the temptation is to keep decision rights centralised. ReNew, by structural design, has had to do the opposite. With pension fund sponsors holding board seats and audit committees enforcing rigorous governance standards, the company operates closer to a US- or Canadian-listed utility than to a typical Indian promoter-driven business. Capital allocation decisions, in particular, are increasingly subjected to a returns-first hurdle rather than a capacity-first hurdle.

That is the second important behavioural shift of the current era. For the first decade of the company's life, the implicit operating principle was "grow the megawatts; the returns will follow." It was a land-grab mentality, appropriate for a moment when the prize was scale and the cost of capital advantage that came with it. By 2023–24, that calculus had inverted. With auction tariffs squeezed and the platform already at substantial scale, growth for its own sake no longer made sense. The new operating principle is closer to "earn the return first, build the megawatts second" — meaning that the company will pass on auctions where the math does not work, and will deploy capital toward higher-return adjacencies even if it means slower headline-capacity growth.[^15]

The board itself reflects this hybrid governance model. Sinha's voting stake in the company is in the mid-teens range — meaningful but not controlling — and the largest non-founder shareholders include sovereign and pension-style investors with seats and observer rights.3 The result is a governance structure where neither the founder nor any single investor can unilaterally drive decisions, and where strategic shifts of any magnitude require genuine board-level consensus.

For investors trying to assess management quality, the most important tell is probably the willingness to walk away. Through 2023 and 2024, ReNew publicly declined to bid aggressively in several large central tenders where competitors submitted tariffs that, in Sinha's framing, "did not clear the cost of equity." That discipline is unusual in any utility business and historically rare in Indian renewables, where the cultural pull toward scale-at-any-price has been almost gravitational.[^11]

The natural risk of this kind of governance maturation is that it can ossify into bureaucracy. A company that began as a contrarian venture bet has to be careful not to become so committee-driven that it misses the next big inflection — and there is at least one such inflection visibly on the horizon. Which is the subject of the next section, because some of the most interesting things happening inside ReNew today are not in its core PPA business at all.

VII. The "Hidden" Businesses: Beyond the PPA

Spend an hour in a ReNew earnings call from 2018, and almost everything you hear is about one number: contracted operating megawatts. Spend an hour in a ReNew earnings call from 2025, and you hear about four numbers. The other three are the interesting ones.

Start with what ReNew now calls its Intelligent Energy Solutions segment — the unofficial internal name is something like "the brain." The premise is that intermittent renewable energy is not actually a commodity. A megawatt-hour delivered on a windless afternoon is worth more than a megawatt-hour delivered at noon on a sunny day, and customers — particularly industrial customers — increasingly want firm power, not just cheap power. ReNew has built a software and operations stack to combine its wind, solar, hybrid, and storage assets into "round-the-clock" (RTC) power products: a blended supply that looks much more like a conventional baseload utility than like a weather-dependent renewable.[^15]

The strategic shift this represents is profound. It moves ReNew up the value chain from "I will sell you whatever electrons my plants produce" to "I will sell you a firm electricity contract, and I will manage the intermittency." The economic implication is that customers pay a premium for firmness, and the premium is mostly margin to whoever can manage the underlying portfolio. ReNew, with the largest and most geographically diversified renewable fleet in India, is the natural firmness wholesaler. Moneycontrol, in its January 2024 reporting on the company's strategy, described this pivot as the centerpiece of the next chapter.[^15]

Then there is हरित हाइड्रोजन Green Hydrogen — the moonshot. In April 2022, ReNew, इंडियन ऑयल Indian Oil Corporation, and लार्सन एंड टुब्रो Larsen & Toubro (L&T) signed joint-venture agreements to develop green hydrogen production capacity in India.[^9] The structure was deliberate: IOC brings the offtake demand (it runs the largest refineries in the country, and refineries are among the largest consumers of grey hydrogen today), L&T brings the EPC and electrolyser engineering capability, and ReNew brings the renewable electricity supply that makes the hydrogen "green."

Is this a real business or a press release? The honest answer in 2026 is "still developing." Green hydrogen at sub-$2/kg — the rough threshold at which it begins to compete with grey hydrogen — requires renewable electricity at roughly ₹2 per kWh delivered firm, plus electrolyser capex still falling on its own learning curve. India's राष्ट्रीय हरित हाइड्रोजन मिशन National Green Hydrogen Mission, launched by the government in 2023, set an ambition of 5 million tonnes per annum of green hydrogen production by 2030 and earmarked production-linked incentives to bridge the cost gap.[^10] If even a fraction of that ambition lands, ReNew sits in pole position to be one of two or three Indian players that can supply it at scale. If it does not, the JVs are an inexpensive option that can be deferred or downsized without crippling the parent company.

The third hidden business is solar manufacturing. For a decade, Indian renewable developers were happily dependent on Chinese solar cell and module imports, which were the cheapest in the world by a wide margin. The COVID supply-chain shock of 2020–21, followed by India's geopolitical pivot to reduce dependence on Chinese imports under the आत्मनिर्भर भारत Atmanirbhar Bharat (self-reliant India) policy banner, changed that calculation. The Indian government introduced basic customs duties on imported solar modules and rolled out a Production Linked Incentive scheme for domestic solar manufacturing.5 ReNew has been steadily building backward into its own solar cell and module production, partly to qualify for incentives, partly to insulate its project pipeline from Chinese supply volatility, and partly to capture an additional layer of margin.

The fourth — still small but with margin profile that punches above its weight — is carbon credits. As renewable assets generate offsets that can be sold into voluntary and compliance carbon markets, ReNew has begun monetising a stream of high-margin credit revenue from global corporate buyers, particularly large technology companies pursuing net-zero pledges. This business is too early to materially move the consolidated income statement, but the unit economics are unusual for a utility: near-zero marginal cost on volumes already generated.

Taken together, these four "hidden" businesses constitute the strategic answer to the central question of "what is the moat in a commoditised megawatt market?" The answer is that ReNew is trying to stop being a megawatt company at all and start being a complete electron-and-molecule platform: firm clean power, hydrogen, manufactured modules, and tradable offsets, layered onto a financial backbone of long-duration green bond funding. Whether the market eventually pays for that platform is the question we have to address next, with the tools of strategic analysis.

VIII. Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Step back from the operating detail and ask: what is the underlying competitive structure of this industry, and where does ReNew sit within it?

Start with Hamilton Helmer's Seven Powers framework — the most useful modern lens for distinguishing real competitive advantages from things that merely look like advantages. Of the seven (scale economies, network economies, counter-positioning, switching costs, branding, cornered resources, and process power), three are clearly relevant to ReNew, and the others are largely not.

Scale economies are the most important. In the renewables business, scale shows up in two places. First, in cost of capital: a developer with a multi-gigawatt operating fleet, an investment-grade credit rating, and access to the dollar bond market borrows materially more cheaply than a sub-gigawatt developer reliant on rupee bank debt. Over a 20-year asset life, every 100 basis points of debt cost is enormous economic value. Second, in procurement leverage: a developer placing multi-gigawatt orders with GE (now GE Vernova), Siemens Gamesa, 金风科技 Goldwind, or domestic suppliers commands meaningfully better pricing and delivery slots than a smaller player. ReNew has both flavours of scale, and they reinforce each other.4

Cornered resources are the second power, and they are subtler than they look. In Indian renewables, the cornered resource is not the technology — it is the site. The best wind sites are the windy ones, and they are not making any more of those. The best solar sites are the ones with high irradiance, near transmission, and on land you can actually acquire. ReNew was an early mover in securing wind capacity in तमिलनाडु Tamil Nadu's पलघाट Palakkad Gap and solar capacity in राजस्थान Rajasthan and गुजरात Gujarat — and those positions, once held, are very expensive for late movers to replicate. Transmission interconnection rights, similarly, are functionally rivalrous: a developer with grid access at a key substation has an edge that does not appear on a balance sheet.

Process power is the third — emerging, not yet decisive. ReNew's institutional skill in managing distributed, intermittent fleets through a centralised operations and data platform is a capability that has compounded over more than a decade and is genuinely hard for a new entrant to replicate quickly. Whether this rises to the level of a defensible moat depends on how rapidly software-enabled energy management commoditises across the industry.

The remaining four powers — network effects, switching costs, counter-positioning, branding — are mostly absent or weak. PPAs are 25-year contracts, which is a form of switching cost for individual offtakers, but at the industry level the customer (a state discom) does not switch developers in any meaningful sense.

Now overlay Porter's Five Forces.

Threat of substitutes is structurally low and getting lower. In the medium term, there is no economically viable substitute for clean electricity at scale. Coal is constrained politically, environmentally, and increasingly economically; nuclear in India is moving but slowly; gas is import-dependent and price-volatile. Renewables, paired with storage, are the substitute, not a substitute against.

Threat of new entrants is moderate to high. The capital required is meaningful, but it is not prohibitive — अदाणी ग्रीन Adani Green Energy, टाटा पावर Tata Power, JSW Energy, रिलायंस Reliance Industries (through its new energy business), and a long tail of mid-size developers are all in the market. What protects ReNew is not absence of entrants but its scale-cost-of-capital edge against most of them.

Bargaining power of suppliers is mixed. Module suppliers — historically dominated by Chinese manufacturers — held real leverage, which is precisely why backward integration into manufacturing matters. Turbine OEMs are more consolidated and pricing-rational. Land owners and state governments, treated as suppliers of permits and access, are perpetually negotiated.

Bargaining power of buyers — this is the perennial Indian problem. The buyers are the state distribution utilities, the discoms. They are financially fragile, politically encumbered, and historically slow to pay. Receivables risk has been the single biggest non-market risk that any Indian renewable developer carries.[^11] The mitigant has been to skew offtake toward central counterparties — the Solar Energy Corporation of India, NTPC, and corporate offtakers — which is exactly what ReNew has done in a deliberate, multi-year shift.

Rivalry among existing competitors is intense but rational at the top of the market. The largest four or five Indian renewable developers compete fiercely on bids but cooperate implicitly on industry norms around discom risk, payment security mechanisms, and policy advocacy. Below the top tier, the competitive picture is more fragmented and more brutal.

Synthesise all of this, and ReNew's moat looks like the following: a cost-of-capital advantage protected by a scaled operating fleet, a cornered set of land and transmission rights, and an emerging platform capability in firm power, hydrogen, and manufacturing. None of those alone is a permanent moat. Together, they are a durable structural position in an industry where most of the economic value will eventually accrue to two or three vertically integrated platforms.

The next question is what could go wrong.

IX. Analysis: Bull vs Bear Case

In Acquired tradition, the most useful version of an investment debate is the one where both sides are taken seriously. So let us do that, in the form of a "myth vs reality" treatment of the central narratives that surround RNW today.

Myth one: "Indian renewables is a one-way bet because the policy goal is set." Reality: policy ambition and policy execution are not the same thing. India has revised its renewable targets multiple times, and the actual pace of build-out has consistently lagged announced timelines — auction calendars slip, transmission gets bottlenecked, and discom financial health deteriorates in election years. The 175 GW target for 2022 was missed; the 500 GW non-fossil ambition for 2030 is on a similar trajectory of being ambitious-but-late.[^10] The investable opportunity is real; the slope of the curve is shallower than press releases imply.

Myth two: "ReNew is just an Indian utility and should trade like one." Reality: ReNew's revenue mix, customer concentration, and capital structure are materially different from a typical Indian distribution utility. It earns dollar-linked cash flows from long-tenor contracted assets, increasingly funded with hard-currency green bonds, with a meaningful and growing share of revenue from central and corporate offtakers rather than discoms. That profile is closer to a global infrastructure compounder than to a domestic state-regulated utility. Whether the market pays for that distinction is the open question.4

Myth three: "The SPAC listing was a mistake." Reality: it was a trade-off. The route delivered scale, currency, and global visibility on a timetable that no Indian IPO could have matched, at the cost of being whipsawed by the SPAC-vintage derating that followed. Calling it a mistake requires assuming the counterfactual Indian IPO would have happened on the same terms and held its valuation, which is not obvious.

With the myths interrogated, the structured cases:

The bear case rests on four pillars. First, receivables risk and counterparty health: a meaningful share of ReNew's revenue still flows from state discoms with histories of payment delays, and the worst Indian electricity-sector stress in living memory has historically not been fully telegraphed in advance.[^11] Second, interest rate sensitivity: any asset-heavy utility is a leveraged spread bet between PPA tariffs and the cost of debt; a sustained rise in global rates compresses returns even if everything else stays the same. Third, competition from larger conglomerate platforms: अदाणी ग्रीन Adani Green Energy and रिलायंस Reliance Industries' new energy business have access to internal capital pools and political weight that ReNew, as a standalone, simply does not match. Fourth, execution complexity: the platform pivot into hydrogen, manufacturing, and intelligent energy is the right strategic move, but it is also a multi-year capital-intensive bet whose payoff is uncertain.

The bull case rests on a quieter, more arithmetical argument. India's electricity demand is the single largest under-discussed growth curve in the global economy. The country will roughly double its electricity consumption over the next decade and a half — there is essentially no scenario in which that demand is met without a massive renewable build-out. ReNew enters that build-out with the largest installed base, the deepest pool of long-duration capital, the most diversified renewable-mix fleet, and an emerging platform of higher-margin adjacencies. If you believe in India's growth and the inevitability of the energy transition, ReNew is the most concentrated public-market expression of both bets.

A few second-layer items worth flagging: credit ratings have been the subject of multiple cycles of refinement by Fitch and S&P as the capital structure has evolved, with detail in the agencies' public rating profiles.4 The company's auditor signals, going-concern language, and accounting judgments around capitalisation of project costs and impairment of underperforming assets are normal items to track in the 20-F filings.[^2] On the ownership side, the post-SPAC float has remained relatively concentrated among sovereign and pension-style holders, which both stabilises the register and limits the public market's price discovery — a 13F look at incremental institutional shifts is more useful here than headline index inclusion data.

If you are tracking ReNew over the next several quarters, the data points that actually matter — the KPIs investors should keep in front of them — are smaller in number than the disclosure tables imply. Three stand out.

KPI one: Plant Load Factor (PLF) for the operating fleet. This is the percentage of theoretical maximum output that ReNew's plants actually deliver. It is the cleanest single read on operational execution — wind speeds and solar irradiance you cannot control, but everything else (downtime, soiling, transmission curtailment, scheduling) you can. A trend up is good; a trend down is a real flag.[^2][^8]

KPI two: Weighted-average cost of debt. Because this is a leveraged spread business, the long-run economic value of the company depends almost mechanically on the average rate at which it refinances. Every refinancing cycle either compounds the moat or erodes it.4

KPI three: Days Sales Outstanding (DSO) on receivables. This is the single best window into discom health and counterparty mix shift. It is the place where the perennial Indian problem either becomes a paragraph in a footnote or a paragraph on the front page.[^11]

Two-and-a-half KPIs, if you want to be honest. Plant load factor, cost of debt, and receivables days. Track those, and you will know more about ReNew than ninety percent of the published research will tell you.

X. Epilogue & Final Reflections

Step back from the spreadsheet for a moment and consider what ReNew actually is, in the broader story of the 2020s and 2030s.

For a century, the global energy industry has been organised around a small number of long-lived assets in a small number of geographies — the supermajors and their oil fields, the national champions and their gas pipelines, the utilities and their coal fleets. The energy transition is, among other things, a redistribution of those assets to different geographies and different corporate forms. India is one of the geographies where that redistribution will happen at the largest scale, and ReNew is one of the corporate forms it has taken.

There is a temptation, in covering a company like this, to frame the story as Sinha's. And in some ways it is. Few founders in modern Indian business have so consistently bent the curve of an entire industry around a single thesis. But the more interesting frame is institutional. ReNew is the first Indian corporate experiment in building a utility of the future — a balance-sheet business with venture-stage ambition, public-market discipline, and emerging-market exposure — and getting it to operate at sovereign scale.

The risks are real. The auctions will keep being brutal. The discoms will keep paying late. Rates will move; sentiment will whipsaw; the platform pivot will take longer and cost more than the most optimistic deck implies. None of that is the part that matters most.

The part that matters most is whether ReNew, as an institution, can outlast the cycles. Whether the founder can hand off without breaking the culture. Whether the capital structure can keep refinancing into ever-cheaper, ever-longer-duration debt. Whether the platform layers — hydrogen, manufacturing, intelligent energy, carbon — actually accrete into a moat that survives the next decade of intensifying competition.

If they do, the company built on a 2011 monsoon-soaked pitch deck in a Gurugram conference room will turn out to have done something more enduring than any single megawatt it ever installed. It will have built one of the first true climate-infrastructure utilities of the 21st century — assembled, characteristically, in the language of finance, the metal of turbines, and the sunlight of the Thar Desert.

The rest is execution.

References

-

Sumant Sinha: The Man Behind ReNew's Green Empire — Forbes India, 2021-08-25 ↩↩

-

India's ReNew Power buys Ostro Energy in record $1.5 billion deal — Reuters, 2018-04-03 ↩↩

-

CPPIB and ReNew Power: Long-term Capital Partnership — CPP Investments ↩↩

-

Fitch Ratings: ReNew Energy Global Plc Rating Profile — Fitch Ratings ↩↩↩↩↩↩

-

India's Solar Power Tariffs: The Low-Cost Challenge — BloombergNEF, 2023-11-10 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube