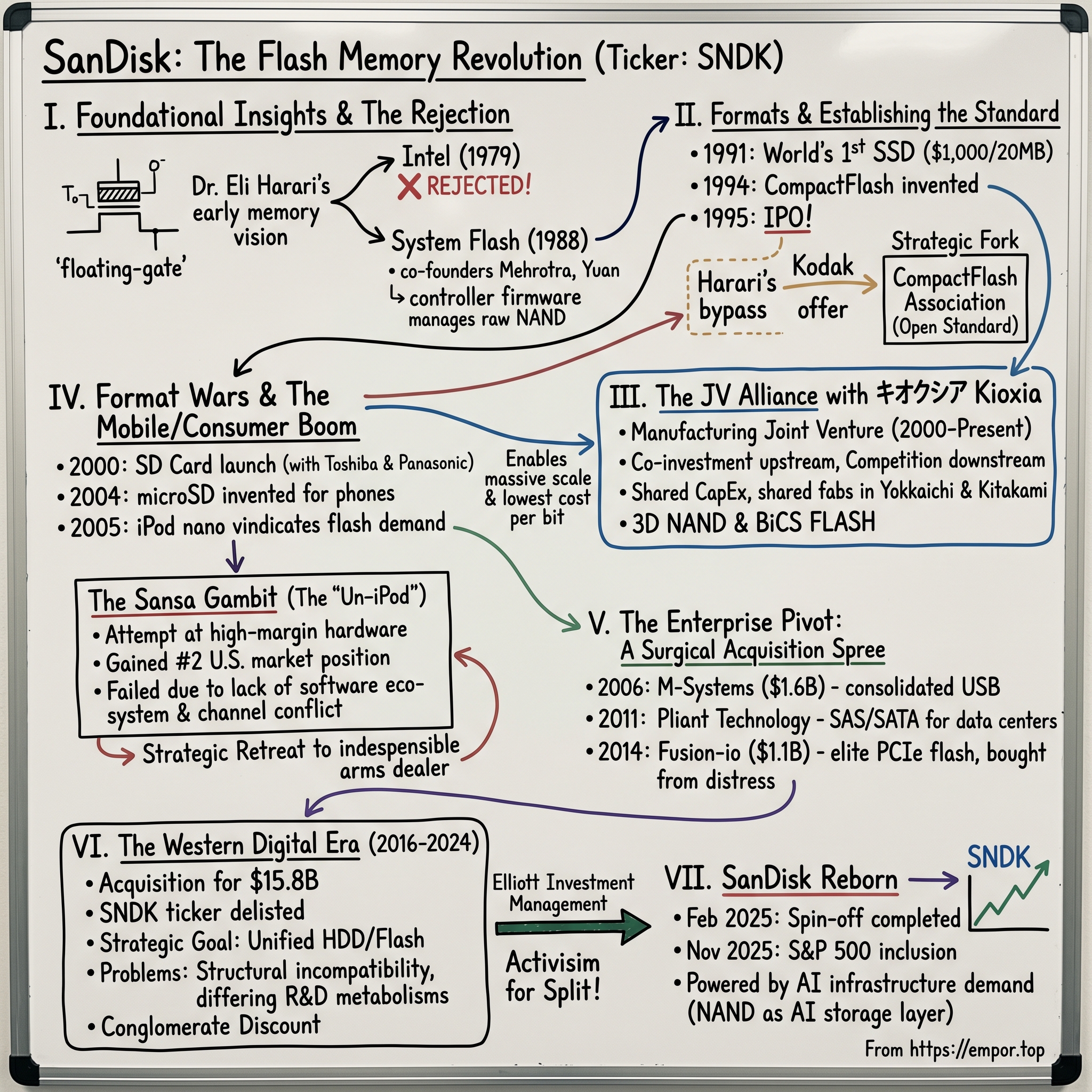

SanDisk: The Flash Memory Revolution

I. Introduction & Episode Roadmap

On the morning of November 24, 2025, a line item buried in a routine index-maintenance notice from S&P Dow Jones Indices set off one of the strangest victory laps in recent market history. Effective before the opening bell on November 28, a company called Sandisk Corporation would join the S&P 500, taking the slot vacated by Interpublic Group.[^1] To most retail investors the name landed somewhere between nostalgia and confusion. Wasn't SanDisk the brand on the little gray-and-red memory cards in the camera drawer? Wasn't it bought years ago and folded into something else? Both true. And yet here it was, ticker SNDK, trading on the Nasdaq again, and the announcement alone sent the stock up roughly 13% in a single session on enormous volume.1

Step back and the arithmetic is almost absurd. SanDisk had been spun out of Western Digital and relisted as an independent company only in late February 2025.[^3] In the nine months between that quiet re-debut and its S&P 500 induction, the shares had climbed more than 500%, vaulting a company that began the year as a sleepy carve-out into a roughly $30-plus billion enterprise riding the single biggest infrastructure build-out of the decade.1 Index inclusion is supposed to be a coronation that arrives years after the real work is done. SanDisk got there in three quarters.

The detail that makes business-history nerds sit up straight is the ticker itself. SNDK is not a new symbol minted for a new company. It is the same four letters that first appeared on the Nasdaq in November 1995, the same letters that went dark in May 2016 when Western Digital closed its acquisition and delisted the brand. For nine years the symbol sat in the graveyard of retired tickers, the digital equivalent of a tombstone. Then it was exhumed, dusted off, and handed back to a company carrying the same name, selling the same fundamental product, run by people who had spent the better part of a decade inside the acquirer. How often does a public company die, get absorbed into a larger organism, and then claw its way back out with its original identity intact and a market capitalization larger than it ever commanded the first time around?

That is the puzzle at the center of this story. How did three immigrant engineers, working from an idea that Intel's leadership flatly rejected, build the physical foundation of modern digital storage? How did that company define the formats inside every digital camera and smartphone of the 2000s, get swallowed by a hard-drive maker fighting for its own survival, and then re-emerge as one of the four firms that physically manufacture the memory feeding the artificial-intelligence boom?

Here is the road we'll travel. We start in 1988 with the founders' spark, the rejection at Intel, and a deceptively simple insight about making cheap, unreliable flash memory behave like a disk drive. We move to the early-1990s breakthroughs, the world's first solid-state drive, the invention of CompactFlash, and the 1995 IPO. We spend real time on the defining alliance of the company's life, the 25-year manufacturing joint venture with the Japanese conglomerate that invented NAND, today known as キオクシア Kioxia. We walk through the format wars that made SD and microSD universal, the doomed flirtation with becoming a consumer hardware brand, and then the surgical decade of acquisitions that dragged SanDisk from the camera aisle into the data center. We dissect the Western Digital merger and its nine-year, ultimately unhappy integration. And we end with the 2025 spin-off, the S&P 500 re-entry, and the strategic frameworks that explain why this particular franchise is so hard to replicate. Let's begin where every good origin myth begins, with a man who could see a future nobody else believed in.

II. The Founders' Spark: Rejection at Intel & The "System Flash" Vision (1988)

Picture a young physicist in the early 1970s, hunched over a workbench at Hughes Aircraft in Southern California, obsessing over something almost unimaginably thin: a layer of silicon dioxide just a few tens of angstroms thick, so delicate that electrons could quantum-mechanically tunnel straight through it. Dr. Eliyahou "Eli" Harari had come a long way to reach that bench. Born in British Mandate Palestine and raised in Israel, he made his way to Princeton, earned a Ph.D. in solid-state physics in 1973, and went to work in the semiconductor industry at a moment when the entire field was still arguing about what memory should even look like.34 At Hughes, Harari did something that would echo for the next half-century: he invented the first practical thin-oxide EEPROM, an electrically erasable memory cell that could hold a charge on a floating gate, isolated, with no power required, and have that charge selectively added or removed by voltage alone.4

To translate the physics into kitchen English: a flash memory cell is a tiny bucket, and the "floating gate" is a bucket so well sealed that once you pour electric charge into it, the charge just sits there for years with the power off. Putting charge in means the cell reads as a "1"; an empty bucket reads as a "0." Harari's contribution was figuring out how to make that bucket reliably fillable and emptiable through an oxide layer thin enough to tunnel through but robust enough not to wear out immediately. That single transistor, the floating-gate cell, is the direct ancestor of every iPhone photo, every SSD, and every AI training checkpoint written to flash today. Harari grasped the implication early and held onto it with the stubbornness of a true believer: if you could pack enough of these cells together cheaply, solid-state memory could eventually replace the spinning magnetic disk entirely.

In 1979 he took that conviction to the most logical home imaginable: Intel. This was the Intel of Gordon Moore and Andy Grove, the company that had practically invented the commercial memory business before pivoting to microprocessors. Harari pitched a solid-state alternative to the hard drive. And Intel, run by some of the sharpest strategic minds in the industry, said no. The logic was not stupid. Microprocessors carried gross margins that memory could only dream of; every wafer of fab capacity and every engineer poured into a speculative storage product was a wafer and an engineer not poured into the x86 franchise that was about to mint money for two decades. Grove's Intel was in the process of making one of the most celebrated strategic retreats in corporate history, walking away from commodity memory to own the brain of the personal computer. Harari was pitching the opposite bet at exactly the wrong moment for that audience. So in the early 1980s he left to chase a dream that was, by any honest reckoning, a decade or two ahead of its market.

It took until 1988 for the pieces to come together. Harari founded a company he called SunDisk, and he did not build it alone. He recruited Sanjay Mehrotra, a young engineer whose path to Silicon Valley was its own parable of persistence. Mehrotra's U.S. student visa had been rejected multiple times in India before his father's sheer refusal to give up finally got him on a plane. The third co-founder was Jack Yuan, an engineer from Taiwan. An Israeli, an Indian, and a Taiwanese immigrant, three outsiders building the storage layer of the American computing future from a standing start. That immigrant-engineer DNA matters, because the problem they set out to solve was not one a marketing department would have prioritized. It was a deeply physical, deeply unglamorous engineering problem.

Here is the catch that everyone, including Intel, understood and that nobody had cracked commercially: raw NAND flash, the dense, cheap variety of flash that makes mass storage economical, is a terrible-behaving material. Out of the fab, it is slow to write, it wears out after a limited number of write-erase cycles, and individual cells fail more or less randomly. Hand a computer a raw NAND chip and ask it to store your files directly, and you would get corruption within weeks. The bucket analogy again: real buckets leak, some buckets are defective from the factory, and every time you scrub a bucket clean to reuse it, you wear down its walls a little.

SanDisk's foundational invention was not a better bucket. It was the brain that managed the buckets. The company built an embedded flash controller, a small dedicated chip running specialized firmware, that sat between the computer and the raw NAND and performed a kind of relentless behind-the-scenes accounting. It spread writes evenly across all the cells so no single bucket wore out first ("wear leveling"). It quietly retired cells that failed and remapped the data elsewhere. It used error-correcting codes to reconstruct bits that flipped. And crucially, it presented the whole messy, failure-prone array to the host computer as a clean, reliable, perfectly behaved disk drive. They called the concept "System Flash." The competitors of the era were selling memory chips. SanDisk was selling a system that made flash trustworthy. That architectural decision, hardware plus controller plus firmware co-designed as one product, is the seed of nearly everything the company became, and we will see it bloom again and again, in CompactFlash, in SD cards, and decades later in the enterprise SSDs feeding AI clusters. The brilliance was recognizing that the bottleneck to a flash revolution was never just the silicon; it was reliability, and reliability was a systems problem. With that insight in hand, SanDisk now needed something to sell.

III. Establishing the Standard: From the $1,000 SSD to CompactFlash & The IPO (1991–1995)

In 1991, a small team at SanDisk demonstrated something that, in retrospect, reads like science fiction shipping a few decades early: a working solid-state drive in a 2.5-inch form factor, the size of a laptop hard disk, with no moving parts at all.5 The capacity was a heroic 20 megabytes. The price was roughly $1,000.5 Do the math and you arrive at a number that explains why nobody put one in a consumer laptop: about $50 per megabyte, which is to say something on the order of fifty thousand dollars per gigabyte in an era when gigabytes were exotic. This was not a product for the masses. It was a product for IBM's early ruggedized laptops, machines headed into environments where a spinning platter would shatter, vibrate, or die: the field, the cockpit, the factory floor. SanDisk had proven the concept of the SSD a full fifteen years before the technology would become economically sane for ordinary computers. The lesson the company absorbed was about where to sell an expensive new technology first, at the high-value frontier where customers will pay a premium for an attribute, in this case durability, that nothing else can deliver.

But the founders understood that durability for rugged laptops was a niche. The mass market for flash, the thing that would justify a real factory and a real company, was coming from an entirely different direction: photography was about to go digital, and digital cameras needed somewhere to put the pictures. This set up the first great strategic fork in SanDisk's road, and Harari's choice tells you everything about how he thought.

Eastman Kodak, the colossus of film, saw the digital wave coming and wanted in. Kodak approached SanDisk and offered to fund its "digital film" effort, the removable flash storage that would replace the roll of film, in exchange for a three-year exclusive contract. For a tiny, capital-starved company, a fat funding check from the most powerful name in imaging must have been almost irresistible. Harari declined. He bet, against the apparent safety of guaranteed money, that exclusivity was a trap. A proprietary format locked to a single customer would forever be a small business. An open format, standardized and licensed broadly so that every camera maker and every rival memory maker could adopt it, could become an industry, and the company that invented and shepherded that standard could win the largest slice of a vastly bigger pie. It was a counterintuitive call: give away the standard to own the market.

In 1994, SanDisk acted on that conviction and introduced CompactFlash, a small, rugged, self-contained memory card with its System Flash controller baked right in.6 The next year, in 1995, SanDisk co-founded the CompactFlash Association, deliberately opening the specification and licensing it to the very competitors it would have to outsell.6 This is the open-standard playbook in its purest form. By making CompactFlash a neutral standard rather than a SanDisk-only product, the company removed the single biggest objection a camera manufacturer could have, the fear of being locked to one supplier, and in doing so it helped unlock the entire digital-camera market. And because SanDisk was the originator, the patent holder, and the highest-volume, lowest-cost producer, it captured an outsized share of a market it had made safe for everyone. CompactFlash became the dominant removable storage format of the early digital-photography era.

By late 1995 the company was ready for the public markets, and it tidied up one piece of housekeeping first. "SunDisk" sounded uncomfortably close to Sun Microsystems, the workstation powerhouse of the moment, so the company rebranded itself SanDisk. On November 8, 1995, SanDisk went public on the Nasdaq under the ticker SNDK, raising roughly $160 million. That capital mattered enormously, because of how SanDisk had been built. In its early years the company ran what the New York Times memorably profiled in 1994 as a "virtual company," an asset-light design house that owned the intellectual property, the controllers, and the architecture, but outsourced the brutally expensive business of fabricating silicon to foundries, notably Taiwan's UMC.7 This let SanDisk punch far above its weight, conserving capital and avoiding the multi-billion-dollar trap of owning a chip fab during a downturn. It was, in spirit, the fabless model that would later define companies like Nvidia and Qualcomm, applied to memory before it was fashionable.

The virtual model was elegant and it was also, eventually, a ceiling. An asset-light company can design the best flash in the world, but it cannot guarantee that someone else's factory will pump out the volume it needs, at the cost it needs, exactly when demand explodes. And demand was about to explode. To go from a clever design house to a giant of the memory industry, SanDisk would have to do the one thing its founding philosophy was built to avoid: get into the business of owning factories. The question was how to do that without betting the company on a single $3 billion fab. The answer came from Japan.

IV. The Joint Venture Model: The Defining Alliance with キオクシア Kioxia (1999–Present)

There is a delicious irony at the heart of SanDisk's most important relationship, and it is worth savoring before we get to the deal mechanics. NAND flash, the entire category of dense, cheap memory on which SanDisk built its fortune, was not invented at SanDisk. It was invented in Japan, at 東芝 Toshiba, by an engineer named 舛岡富士雄 Fujio Masuoka in the 1980s. Toshiba had the foundational technology and world-class manufacturing, but it had struggled to translate that into dominance of the fast-moving, format-driven consumer market where SanDisk thrived. SanDisk had the systems expertise, the controllers, the consumer formats, and the market access, but lacked the capital and the fab muscle to make its own silicon at scale. Each company had precisely what the other lacked. Today's rivals, in other words, were tomorrow's perfect partners.

The pressure that forced the issue was the late-1990s consumer flash boom. Digital cameras were going mainstream, CompactFlash volumes were soaring, and the "virtual company" model was straining. SanDisk needed massive, guaranteed wafer supply at competitive cost, and it needed it locked in for the long haul. Buying capacity on the open market left it exposed to shortages and price spikes exactly when it most needed to grow. Building its own leading-edge fab alone, a multi-billion-dollar undertaking with a brutal depreciation schedule, would have bet the entire company on a single facility and a single cycle. For a firm that had spent a decade deliberately avoiding that kind of capital risk, going it alone was close to unthinkable.

So in 2000, SanDisk and Toshiba did something that reshaped the economics of the memory industry: they formed a 50-50 manufacturing joint venture, initially branded FlashVision, to jointly build and operate state-of-the-art NAND fabs. The division of labor mapped almost exactly onto each partner's strengths. SanDisk contributed systems-level controller IP and, critically, its design expertise in multi-level cell (MLC) technology, the trick of storing more than one bit in each memory cell to multiply density and slash cost per bit. Toshiba contributed deep process technology and world-class manufacturing scale. Together they poured concrete at Toshiba's sprawling semiconductor complex in 四日市市 Yokkaichi, in Japan's Mie Prefecture, building the fabs, Fab 1, Fab 2, and successors, that would churn out the wafers both companies needed.

The structure deserves a moment of appreciation because it is the strategic crown jewel of the entire SanDisk story. In a shared fab, the two partners split the staggering capital expenditure roughly down the middle. They jointly own and operate the facility, sharing the cost of the equipment, the cleanrooms, and the relentless reinvestment that NAND requires every generation. But, and this is the elegant part, they take their respective shares of the finished wafers and sell them separately, into their own markets, under their own brands, competing with each other downstream. It is co-investment upstream and competition downstream. The effect for SanDisk was transformational: it gained the cost structure and scale of a vertically integrated memory giant, comparable to what a Samsung achieved by spending tens of billions of its own money, while carrying only half the capital risk of any given fab. The virtual company had found a way to own factories without betting the company on them.

What is genuinely remarkable is that this alliance has now endured for more than a quarter-century, surviving ownership changes that would have shattered a weaker partnership. The most dramatic came in 2018, when a financially pressured Toshiba spun off its prized memory unit, selling it to a consortium led by Bain Capital. That carved-out memory business was eventually renamed キオクシア Kioxia, from the Japanese word kioku, meaning "memory."9 The partner's corporate parent changed, its name changed, its ownership changed, and the joint venture rolled on essentially intact. Today SanDisk and Kioxia continue to co-develop and co-manufacture flash, and the relationship has expanded geographically beyond Yokkaichi to a newer, cutting-edge facility in 岩手県 Iwate Prefecture, at the 北上市 Kitakami plant, where the partners run advanced fabs producing their latest-generation 3D NAND, memory built in towering vertical stacks of cell layers reaching into the hundreds of layers and climbing.9

That last phrase, "3D NAND," is worth unpacking because it is where the technology went after planar density hit a wall. For years, engineers shrank flash cells by packing them more tightly on a flat plane, the way a city grows by subdividing lots. Eventually the cells got so close that they interfered with one another, and the shrink stopped working. The breakthrough, which SanDisk and Kioxia pioneered under the BiCS FLASH brand, was to stop building out and start building up, stacking memory cells in vertical layers like floors in a skyscraper. Going from a sprawl of single-story houses to a high-rise multiplies the storage you can fit on the same patch of silicon, and it is the reason flash density and cost-per-bit have kept improving long after planar scaling died.

So what does the Kioxia alliance mean for an investor trying to value SanDisk today? It means the single most important asset on the company's strategic balance sheet is not on its actual balance sheet at all. It is a 25-year-old, jointly-owned manufacturing and co-development partnership that gives SanDisk industry-scale cost economics without sole capital exposure, and that a competitor could not replicate without spending tens of billions of dollars and a decade of accumulated process learning to even approach it. Hold that thought; it becomes the linchpin of the strategic analysis later. For now, with a guaranteed wafer supply finally secured, SanDisk could turn back to the thing it did best: winning format wars.

V. The Removable Storage Revolution: Format Wars, SD, and the Mobile Boom (1999–2005)

If CompactFlash made SanDisk a force in digital photography, the early 2000s presented a richer and more contested prize: the universal memory card. As gadgets multiplied, cameras, camcorders, PDAs, music players, and soon phones, every manufacturer wanted storage, and a vicious standards war broke out over whose card would become the default. Sony, characteristically, pushed its own proprietary Memory Stick, a closed format that worked beautifully inside the Sony ecosystem and nowhere else. Other camps backed SmartMedia, MultiMediaCard, and a confusing alphabet of rivals. The stakes were enormous, because the winning format would be designed into billions of devices and would throw off licensing economics and volume for whoever controlled it.

SanDisk had already learned the lesson that would decide this war: open beats closed when you have the manufacturing muscle to win on volume. In 2000, SanDisk joined forces with Toshiba and Panasonic to launch the Secure Digital format, SD, and to stand up the SD Association at that January's Consumer Electronics Show to govern and license it.8 The "Secure" in Secure Digital was a deliberate nod to the content owners of the era, who wanted digital-rights-management hooks built in, but the strategic genius was the same one Harari had deployed with CompactFlash. By making SD an open, multi-vendor standard backed by three heavyweight manufacturers across the US and Japan, the alliance gave device makers exactly what Sony's Memory Stick could not: a format with multiple competing suppliers, predictable pricing, and no single point of control. Device makers voted with their card slots. SD steadily crushed Memory Stick and the rest, and became the universal removable storage standard it remains today, the small notched card in virtually every camera on earth.

Then SanDisk made the format smaller, and in doing so caught the next, far larger wave. In 2004, the company introduced a memory card shrunk to roughly the size of a fingernail, initially branded TransFlash and soon standardized by the SD Association as microSD.8 The engineering was non-trivial, cramming the same controller-managed flash system into a sliver of plastic and silicon, but the timing was sublime. Mobile phones were about to become pocket computers, and they desperately needed expandable storage in a form factor that would not bloat the device. microSD became the default storage-expansion slot for an entire generation of phones, shipping into billions of handsets worldwide. SanDisk, the arms dealer, was now supplying ammunition to the single fastest-growing consumer-electronics category in history.

Underneath these product wins, a deeper economic tide turned in 2004, and it is the kind of inflection that reshapes whole industries quietly. For years, NAND flash had been more expensive per gigabyte than DRAM, the fast working memory in computers. In 2004, the lines crossed: NAND pricing fell below DRAM on a per-gigabyte basis, the product of relentless density scaling and the very fab investments SanDisk and Toshiba had been making. Suddenly solid-state storage was cheap enough to displace not just film but magnetic tape and optical discs in whole new categories, above all portable music. Flash had crossed the threshold from "exotic" to "economical" for mass storage.

The company that proved it, and in the process consumed staggering quantities of the world's NAND, was Apple. In 2005, Apple shipped the flash-based iPod shuffle and, more importantly, the iPod nano, abandoning the tiny spinning hard drive of the iPod mini for solid-state flash. The nano was a sensation, and Apple's appetite for NAND was so vast that it reshaped the supply-demand balance of the entire memory industry, locking up capacity and sending pricing signals through every fab on the planet. For SanDisk, this was vindication on a grand scale: the solid-state future Harari had pitched to a skeptical Intel in 1979 was now selling tens of millions of units in candy colors. It was also, quietly, a warning. Apple had just demonstrated that the real consumer margin, the brand, the software, the lifestyle, lived in the device, not the memory inside it. SanDisk, flush with cash and confidence, was about to test whether it could climb up the value chain and capture that margin for itself. It would be a painful experiment.

VI. The Sansa Gambit & The Consumer Brand Paradox (2005–2010)

By 2005, SanDisk had a problem that most companies would kill for: too much cash and a front-row seat to a gold rush it was helping supply. It watched Apple sell flash-based iPods at fat margins, margins fattened by SanDisk's own component category, and it drew the conclusion that ambitious component makers have drawn since the dawn of industry: why sell the picks and shovels when you could sell the gold? If flash storage was the heart of the digital music player, and SanDisk made the best, cheapest flash on earth, surely it could build a player of its own and keep the consumer margin instead of handing it to Cupertino.

So SanDisk launched the Sansa line of MP3 players, and for a brief, heady stretch it actually worked. The strategy was to be the feature-rich anti-Apple, the "un-iPod" for buyers who wanted more for less. Where the iPod was famously minimalist and famously closed, the Sansa e200 series, the flagship of the push, threw in color screens, FM radio tuners, voice recording, and, naturally, a microSD slot so users could expand storage with the very cards SanDisk sold. It was a maximalist value proposition aimed squarely at the gap above the cheap no-name players and below Apple's premium. The market responded. By 2006, SanDisk had clawed its way to the number-two position in the U.S. MP3 player market, behind only Apple. For a company that had never sold a finished consumer gadget under its own brand, taking the silver medal in a category Apple was busy turning into a cultural phenomenon was a genuine achievement.

And yet the Sansa hit a wall, and the reason it hit that wall is one of the most instructive episodes in the whole SanDisk story. Hardware features were never Apple's moat. Apple's moat was iTunes, the seamless software that ripped, organized, bought, and synced music without the user ever thinking about file formats or drag-and-drop. Apple's moat was a brand that turned an electronics purchase into an identity statement, white earbuds as a status signal. SanDisk could match Apple spec-for-spec on the hardware, it could even beat Apple on raw features and price, but it had no answer to the ecosystem. There was no SanDisk equivalent of iTunes, no lifestyle marketing apparatus, no developer relationships, no retail-experience choreography. SanDisk was a world-class engineer of silicon and systems trying to win a fight that was being decided in software and brand, two disciplines that lived in a completely different part of the corporate soul.

There was a second, subtler problem, and a sophisticated observer would have flagged it early: channel conflict. SanDisk's most valuable position in the industry was as the trusted component supplier to everyone, including the very companies it would now be competing against on retail shelves. Every hour and dollar spent fighting Apple, Samsung, and Sony for end-consumer MP3 sales was an hour and dollar that strained its relationships with the customers who bought its flash by the truckload. An arms dealer who starts fielding his own army makes his best customers nervous.

So SanDisk did something disciplined, the kind of unsentimental strategic retreat that, like Intel exiting memory a generation earlier, looks wise mainly in hindsight. It wound down the consumer-hardware ambition and pivoted back to its true source of power: being the indispensable arms dealer to the entire consumer-electronics industry, not a combatant in it. The Sansa experiment had cost money and pride, but it bought a permanent and valuable lesson about where SanDisk's edge actually lived, in components, controllers, formats, and manufacturing, and where it did not, in ecosystems and lifestyle brands. With that clarity, the company turned its gaze to where the highest-margin flash demand was heading next. It was not heading to retail shelves. It was heading to the data center.

VII. The Enterprise Pivot: A Surgical Analysis of SanDisk's Acquisition Spree

Around 2010, the center of gravity in the flash business began to shift in a way that would define SanDisk's second decade. The glamorous, high-volume frontier of the 2000s, cameras, MP3 players, phones, was maturing into a commodity grind where pricing power was thin and competition brutal. The new high-margin frontier was emerging in a less photogenic place: the cloud. Hyperscale data centers and enterprise storage arrays were beginning to crave flash for its speed and density, and they would pay real money for drives that were not just fast but reliable, manageable, and enterprise-grade. SanDisk knew flash silicon cold. What it did not yet own was the enterprise systems layer, the controllers, the interfaces, the caching software, the data-center sales channels, that turned raw NAND into products a CIO would trust with a bank's transaction records. So the company went shopping, and it shopped with surgical intent. Over roughly a decade, SanDisk assembled its way into the enterprise, deal by deliberate deal.

The groundwork came early and cheap. In 2005, SanDisk acquired Matrix Semiconductor, a developer of three-dimensional, one-time-programmable memory. Matrix's near-term products were modest, but the acquisition planted intellectual-property seeds in vertical, stacked memory structures, the conceptual ancestor of the 3D NAND that would later become the industry's entire future. It was a small bet on a physical idea, building memory up rather than out, that would pay off enormously a decade later.

The first truly consequential enterprise deal landed in 2006, when SanDisk acquired the Israeli firm M-Systems in an all-stock transaction valued at roughly $1.55 billion.10 M-Systems was no random target; it was the inventor of the USB flash drive, the "DiskOnKey" that put a keychain's worth of storage in everyone's pocket, and it was SanDisk's chief rival in that exact category. On the surface the price looked rich. M-Systems was valued at something like four times trailing sales, a clear premium to the one-and-a-half to two times that traditional hardware businesses fetched. But the strategic logic underneath the multiple was compelling, and it is worth walking through because it is the template SanDisk would reuse. First, the deal consolidated the USB-drive market, removing SanDisk's most direct competitor and giving it the patented TrueFFS flash-management software. Second, and more powerfully, it created a margin engine: SanDisk could now route its own internally-produced, low-cost NAND into M-Systems' higher-margin embedded and enterprise products, capturing the full stack of value instead of selling cheap chips to someone else who captured it. The combination birthed the ubiquitous Cruzer USB line and instantly expanded margins. A "premium" multiple looks very different when you control the cost of the most expensive input.

If M-Systems was about consolidating a consumer category and expanding margin, the next wave of deals was about buying genuine enterprise credibility, and it began in 2011 with Pliant Technology for about $327 million.12 Pliant mattered far more than its modest price suggested. It brought high-performance enterprise SSDs and, crucially, the controller software for SAS and SATA, the interface standards that enterprise storage arrays actually speak. This was the precise hinge moment when SanDisk stopped being a company that packaged raw silicon and became a company that engineered elite enterprise systems. You cannot sell to a data center on density alone; you have to speak its protocols and meet its reliability bar, and Pliant gave SanDisk both.

The company kept stacking complementary capabilities. In 2012 it acquired FlashSoft, a maker of caching software that used flash to accelerate servers, and Schooner Information Technology, which specialized in flash-optimized database engineering. Neither was a blockbuster, but together they signaled an important intellectual maturation: SanDisk now understood that enterprise performance is not a hardware property or a software property but the product of hardware and software co-designed together, the very philosophy that had animated System Flash back in 1988, now aimed at databases instead of cameras. In 2013, SanDisk added SMART Storage Systems for roughly $307 million, bolstering its enterprise SATA portfolio and, just as importantly, its data-center sales channels and OEM relationships.13 Each deal bought a missing piece of the enterprise puzzle: protocols, then software, then channel.

Then came the biggest and most controversial bet of the whole campaign. In 2014, SanDisk agreed to acquire Fusion-io for approximately $1.1 billion in cash.11 Fusion-io was a fallen star. It had been the darling of ultra-fast PCIe flash storage, the company that put flash directly on the high-speed PCIe bus instead of behind a slow disk interface, and it counted marquee names like Apple and Facebook among its customers. At its post-IPO peak Fusion-io had been valued at well over $3 billion. By 2014 it was burning cash and trading at a steep discount to those glory-day highs, and SanDisk picked it up at $11.25 per share, a price that worked out to roughly two and a half times enterprise value to sales.23

That multiple is the whole story, so sit with it. At the time, comparable high-growth cloud-storage and storage-software peers were commanding eight to ten times sales. SanDisk bought elite PCIe architecture and database-acceleration software for a fraction of what the market was paying for similar capabilities elsewhere, precisely because Fusion-io was in operational distress and SanDisk had the discipline to buy a wounded leader rather than a healthy one. The cynic's worry, that SanDisk was catching a falling knife, a cash-burning business in a category that might commoditize, was not unreasonable. But the contrarian's payoff was real: the acquisition vaulted SanDisk past Western Digital into third place globally in enterprise SSD market share and handed it the PCIe expertise that would matter enormously as the industry moved toward NVMe, the protocol that now dominates AI-era storage. SanDisk had used a decade and a series of carefully-priced acquisitions to transform itself from the brand on a camera card into a credible enterprise-storage company. And in doing so, it made itself exactly the kind of asset a struggling hard-drive giant would feel it absolutely had to own.

VIII. The Western Digital Consolidation: The Marriage of HDD & Flash (2015–2024)

To understand why Western Digital paid a fortune for SanDisk, you have to feel the existential dread that was settling over the hard-disk industry in the mid-2010s. Western Digital and Seagate had spent decades perfecting the spinning magnetic hard drive, a marvel of mechanical engineering with read-write heads flying nanometers above platters whirling at thousands of RPM. It was a great business, cash-generative and consolidated. And it was staring down a future in which its core product would be slowly, then quickly, eaten alive by flash. SSDs were getting cheaper and faster every year; in laptops and performance applications they had already won. A hard-drive company with no flash franchise was a buggy-whip maker watching the automobile arrive. Western Digital concluded, correctly, that survival required owning NAND, and you could not credibly build a leading flash position from scratch against Samsung, Toshiba, and SanDisk. You had to buy one.

In October 2015, Western Digital announced a definitive agreement to acquire SanDisk in a cash-and-stock deal valued at roughly $19 billion, or $86.50 per share.14 But the deal had an unusual and fragile dependency baked into it. Part of the financing math relied on a planned $3.775 billion equity investment in Western Digital from Unisplendour, a unit of China's 清華紫光 Tsinghua Unigroup, which would have taken a roughly 15% stake in WD.15 That Chinese investment ran straight into the buzzsaw of U.S. national-security review; once the Committee on Foreign Investment in the United States signaled it would scrutinize the transaction, Unisplendour withdrew.15 Western Digital restructured the deal accordingly, and when the acquisition closed in May 2016 the price had been adjusted downward to roughly $15.8 billion, around $78.50 per share.15 The SNDK ticker went dark. SanDisk, the independent company, ceased to exist, and its founders' creation became a division inside a hard-drive conglomerate.

On paper, the strategic theory was sound, even elegant. Western Digital's leadership, under CEO Steve Milligan and later David Goeckeler, envisioned a unified storage powerhouse that could serve every tier of the market: cheap, high-capacity, cash-generative hard drives for bulk and cold storage, and high-growth, high-margin flash for performance and enterprise. You would milk the mature HDD business for cash and plow it into the high-growth flash business, a portfolio balanced across the storage hierarchy. Customers could be served from a single vendor across their entire storage stack. It was the kind of synergy story that looks irresistible in a banker's deck.

The trouble was that the two businesses, however complementary on a customer's purchase order, were structurally incompatible at the level of how they consumed capital and ran their R&D. NAND flash is a fab business, and a fab business is a treadmill: it demands continuous, enormous, highly cyclical capital reinvestment to move from one process generation to the next, tens of billions of dollars across cycles, much of it flowing through the Kioxia joint venture with all the coordination that entailed. Hard drives, by contrast, are a mature, consolidated manufacturing business with a very different and far less frenetic reinvestment rhythm, longer product cycles, and a duopoly's relative pricing stability. Running both under one roof meant the capital-allocation committee was forever trying to serve two masters with opposite metabolisms. The flash side needed to spend aggressively and ride brutal cyclical swings; the disk side wanted steady harvest. The cultures, the R&D cadences, and the investment cases simply did not rhyme. The "conglomerate" was less a synthesis than an uneasy cohabitation.

By 2022, the market had noticed the friction, and so had one of the most feared investors on Wall Street. Elliott Investment Management disclosed a stake of nearly $1 billion in Western Digital, roughly 6% of the company, and sent the board a pointed letter arguing that the SanDisk acquisition was not working and that the two businesses would be worth dramatically more apart than together.16 Elliott went so far as to offer over $1 billion of fresh equity capital toward separating the flash unit, pegging the flash business at an enterprise value of $17 to $20 billion on its own.16 The core of Elliott's argument was a phrase every conglomerate fears: the conglomerate discount. By stapling a cyclical, capital-hungry flash business to a mature hard-drive business, Western Digital had created a hybrid that neither flash investors nor disk investors wanted to own at full value, and the market was pricing the combination below the sum of its parts. Unlocking that gap meant doing the thing that, six years and one painful integration earlier, had seemed like the path to safety: pulling the two businesses back apart. The arms dealer was about to get its independence back.

IX. SanDisk Reborn: The 2025 Spin-off, S&P 500 Re-entry, & The New Era

The separation became official on February 24, 2025, when SanDisk shares began trading again on the Nasdaq under the resurrected ticker SNDK.[^3]2 The mechanics were a classic tax-efficient spin-off: Western Digital distributed about 80% of SanDisk's shares to its existing stockholders, with each WD holder receiving roughly one-third of a SanDisk share for every WD share owned, while WD retained a passive stake of just under 20% to be monetized over time.[^3] Western Digital kept the hard-drive business and its name; the flash memory and SSD franchise, the controllers, the brand, the Kioxia joint venture, walked out the door as an independent company once more. After nine years inside a larger organism, the founders' creation was free-standing again, this time led by David Goeckeler, who stepped from the top of Western Digital into the CEO chair of the new SanDisk.

What happened next was not in anyone's banker model. SanDisk re-entered public markets at a relatively modest valuation, a spin-off that the market initially treated as a sleepy carve-out of a commoditized business. Then the ground shifted beneath the entire memory industry. The generative-AI build-out, which through 2023 and 2024 had been overwhelmingly a story about GPUs and the high-bandwidth DRAM stacked next to them, began to reveal its voracious appetite for the other kind of memory: NAND flash, the storage layer where the colossal datasets, model checkpoints, and inference caches of AI actually live. AI servers, it turned out, demand vastly more solid-state storage than conventional servers, and the hyperscalers building them were racing to lock up capacity. A NAND industry that had spent 2023 in a punishing down-cycle, with pricing collapsed and margins near zero, swung violently into shortage and pricing power.20

SanDisk, freshly independent and suddenly a pure-play bet on exactly this dynamic, caught the full force of the upswing. The stock that had debuted as an afterthought climbed relentlessly through 2025 as investors woke up to what they were looking at: one of only a handful of companies on earth that physically manufactures NAND at leading-edge scale, newly unshackled from a hard-drive parent, riding a once-in-a-decade demand supercycle. By the time S&P Dow Jones Indices announced on November 24, 2025 that SanDisk would join the S&P 500, the shares had risen more than 500% from their February debut, and the inclusion itself, effective before the open on November 28, triggered another double-digit pop as index funds were forced to buy.[^1]1 Nine months from spin-off to S&P 500 membership is a velocity that index committees almost never witness; inclusion is typically a lagging honor, and SanDisk had earned it at a sprint.

The financial reality underneath the share-price fireworks was genuine, not merely a momentum story. When SanDisk reported its fiscal first quarter of 2026 in November 2025, for the quarter ended October 3, 2025, revenue came in at about $2.31 billion, up 21% sequentially and roughly 23% higher than the year-ago period, with data-center revenue up 26% sequentially as multiple hyperscale customers moved through qualification of SanDisk's enterprise drives.19 The growth was being driven by exabytes, the sheer volume of storage capacity shipped, expanding even faster than dollar revenue, the signature of a business where demand is outrunning the industry's ability to supply bits. Independent execution had, in the most literal sense, unleashed a franchise that had spent nine years as a line item inside someone else's segment reporting. The question for investors was no longer whether SanDisk could stand on its own. It was how durable the moat around this suddenly-precious franchise really was. To answer that, we need to put it through the strategic wringer.

X. The Strategic Engine: Hamilton's 7 Powers & Porter's 5 Forces Applied

Strip away the AI excitement and the index-inclusion drama, and the durable question is the one every long-term investor must ask: what, exactly, protects SanDisk's profits from being competed away? Memory has a fearsome reputation as a commodity business, a place where capacity gets overbuilt, prices crater, and returns evaporate on a brutal cycle. So is there real, defensible power here, or just a well-timed ride on a wave? Hamilton Helmer's 7 Powers framework and Michael Porter's Five Forces give us two complementary lenses, and applied honestly they reveal both a genuinely formidable moat and the precise places where the moat has gaps.

Start with the single most important source of power, and it maps onto what Helmer calls a Cornered Resource: the Kioxia joint venture. We have already walked through its mechanics, so the point here is simply its strategic weight. A 25-year-old, deeply integrated, jointly-owned manufacturing and co-development alliance, with shared fabs in Yokkaichi and Kitakami and a quarter-century of co-engineered process technology, is not something a competitor can buy or build on any reasonable timeline. To replicate it, a rival would need not only tens of billions of dollars for leading-edge fabs but also a willing world-class partner and a decade of accumulated joint learning. It is, in the most literal Helmer sense, a resource that competitors cannot access on equal terms. This is the crown jewel, and it is why a "commodity" business can sustain a structural cost and capability advantage.

Layered on top is Process Power, the accumulated, hard-to-imitate know-how embedded in decades of manufacturing learning curves. SanDisk and Kioxia's BiCS FLASH 3D NAND, and especially the newer CBA architecture, in which the CMOS logic circuitry is fabricated separately and then directly bonded to the memory array rather than built beneath it, represents the kind of deep process innovation that cannot be reverse-engineered from a datasheet. Yields, layer counts, and bonding techniques are refined through years of iterative production, and that tacit knowledge compounds. Process Power is why being early and staying in the game matters so much in memory: the learning curve is a moat that deepens with every wafer.

Helmer's Scale Economies show up here too, though with an important nuance: SanDisk achieves its scale through the Kioxia alliance rather than alone. The shared fabs let the partnership manufacture at a unit cost per bit competitive with the largest standalone players, Samsung and SK Hynix, despite neither SanDisk nor Kioxia individually matching those giants' balance sheets. The fixed costs of a fab, and the staggering cost of each process transition, are spread across the combined volume of two companies' demand. Scale in memory is everything, because cost-per-bit determines who survives the downturns, and the JV manufactures scale that neither partner could afford solo.

Finally, in the consumer arena, SanDisk retains real Brand power, the one piece of consumer equity that survived and even justified the Sansa retreat. Walk into any electronics retailer and the SanDisk name on an SD card or portable SSD still signals reliability to ordinary buyers in a way that commodity competitors cannot match, and that trust supports premium retail pricing on otherwise-similar silicon. It is a modest power compared to the JV, but it is a genuine one, and it throws off stable, higher-margin consumer cash flow that helps cushion the brutal cyclicality of the wholesale bit business.

Now turn to Porter, which is less about SanDisk's individual powers and more about the structure of the industry it competes in, and here the picture is a study in contrasts. Rivalry among existing competitors is extremely high, because NAND is a consolidated oligopoly of a handful of titans slugging it out. Samsung (삼성전자 Samsung Electronics) sits at the top with something like 30-33% of the market; SK Hynix (SK하이닉스 SK Hynix) holds roughly 20-22%; Micron carries around 10-12%; and Kioxia (キオクシア Kioxia) together with SanDisk command somewhere in the 25-30% range through their alliance.[^22] When a handful of players with massive fixed costs all want to keep their fabs full, the temptation to overbuild and discount in a downturn is intense, which is exactly what produced the savage 2023 trough. Rivalry is the force most likely to punish shareholders, and it is the structural reason memory has historically been a cyclical heartbreaker.

But the same consolidation that intensifies rivalry also produces a near-impregnable barrier on the next force: the threat of new entrants is very low, arguably as low as in any industry on earth. A modern leading-edge NAND fab costs well over $10 billion, and the bulk of that outlay, the lion's share, flows to a tiny number of equipment makers like ASML and Applied Materials whose machines are themselves scarce and backordered. On top of the capital wall sits a geopolitical one: U.S. national-security rules and trade restrictions aimed at China's 长江存储 Yangtze Memory Technologies (YMTC) have specifically constrained the one category of player, state-subsidized Chinese fabs, that could otherwise flood the market with below-cost bits. The capital barrier alone would deter almost anyone; the policy environment slams the door. This is the force most favorable to incumbents, and it is a large part of why the AI-driven up-cycle has been allowed to run rather than being instantly competed away by new supply.

On the bargaining power of buyers, the answer is "moderate to high, and pulling in two directions at once." The buyers that matter most now are the hyperscale cloud providers, Amazon, Microsoft, Google, and their peers, who purchase storage in such colossal quantities that they negotiate ferociously and can play suppliers against one another. In a normal market that power would compress SanDisk's margins. But these same buyers are, at the present moment, desperately capacity-constrained: their AI clusters cannot function without vast quantities of high-performance flash, and there is not enough leading-edge NAND in the world to satisfy everyone at once. Acute scarcity temporarily flips the leverage, which is why suppliers have been able to push through price increases that would have been unthinkable in 2023.20 The structural power of buyers is high; the cyclical reality, for now, hands pricing power back to the sellers. That tension, powerful buyers versus scarce supply, is the crux of the entire bull-bear debate, which is where we turn next.

XI. The Investment Case: Key KPIs, Bull vs. Bear, and Current Management

The person now steering this newly-independent franchise is a deliberate departure from the engineer-founders who created it, and understanding David Goeckeler is essential to understanding the company's current posture. SanDisk was built by physicists and memory architects, people who fell in love with floating-gate transistors. Goeckeler is not that. Before he ran Western Digital, he spent years at the top of Cisco, leading its roughly $34 billion networking and security business, the beating heart of the company.16 He is, in other words, a strategy-and-operations executive steeped in selling complex systems to enterprises, not a man who came up designing memory cells. That background is telling, because SanDisk's future profit pool sits precisely where Goeckeler's instincts run: in enterprise systems sold to data centers, not in commodity cards sold at retail.

His incentives are sharply aligned with the thing public shareholders care about. Having presided over the separation, Goeckeler's compensation as SanDisk's CEO leans heavily on performance-based equity tied to concrete SNDK targets, hitting a 20% operating margin, generating $1.2 billion of free cash flow, and successfully executing the technology migrations to the next BiCS generations, BiCS 8, 9, and 10, that keep SanDisk on the cost-per-bit treadmill.22 When a CEO's payout is bolted to margin, cash generation, and process-node execution rather than to revenue or empire-building, it tends to concentrate the mind on exactly the levers that matter in a capital-intensive cyclical business. The extraordinary share performance since the spin-off has, not coincidentally, made that alignment lucrative.

Where is the value actually being created inside the company? The honest answer is that the future investment case rests disproportionately on one segment: enterprise SSD. The consumer business, the SD cards, the microSD, the retail portable drives, remains a stable, brand-supported, cash-generative foundation, but it is not where the growth lives. The growth, and the high-margin profitability, lives in the enterprise SSDs going into AI training clusters and cloud data centers, a segment expanding at a triple-digit year-over-year clip and increasingly driving the company's profit mix. This is the part of SanDisk that the market is really paying for, and it is the part that justifies the re-rating from "commodity carve-out" to "AI infrastructure play." An investor who wants to understand SanDisk's trajectory should watch this segment above all others.

Which points to the small handful of metrics that actually matter for tracking this business over time. Resist the temptation to drown in the dozens of figures memory companies report, and zero in on three. The first is bit-shipment growth, the company's exabytes shipped, watched against the growth of total global NAND capacity; this is the cleanest read on whether SanDisk is holding or gaining share of the bits the world consumes, and it strips out the noise of swinging prices. The second is the gross-margin trajectory, which in memory is the truest proxy for the combination of pricing power and manufacturing yield; SanDisk's gross margin swung from a catastrophic single-digit level in the depths of the 2023 downturn to the mid-30s and far beyond as the up-cycle and AI demand took hold, and the direction of that line tells you almost everything about where the company sits in the cycle.19 The third is the enterprise-SSD revenue mix, the share of revenue coming from cloud and data center versus consumer retail; a rising mix signals SanDisk is successfully shifting its weight toward the structurally higher-margin, faster-growing part of the market. Three numbers: how many bits, at what margin, and how much of it is enterprise. Track those and you understand the story.

Now the debate, because a franchise priced for a supercycle deserves both barrels. The bull case is straightforward and, at the moment, powerful. The AI build-out is a genuine demand-side regime change, not a fad: AI servers can require several times the SSD capacity of conventional servers, and the hyperscalers are nowhere near done building. Meanwhile, the supply side has grown more disciplined than in past cycles, with the major players showing restraint on capacity additions, which tames the historical boom-bust whiplash and lets pricing hold. A meaningful slice of SanDisk's production is increasingly covered by longer-term contracts, smoothing the revenue line. And the Kioxia cornered resource, the very low cost-per-bit, and the entrenched enterprise relationships mean that when the industry makes money, SanDisk makes a lot of it. In a tight market with high barriers to new supply, a low-cost incumbent with elite enterprise products is exactly where you want to be positioned.

The bear case is equally serious and should not be waved away by the share chart. This is, at bottom, still a memory business, and memory has broken the hearts of investors for forty years through its remorseless cyclicality. The same supercycle that drove gross margins from single digits to stratospheric levels in roughly two years is a reminder of how violently the pendulum swings; demand can soften, the hyperscalers can digest their build-outs, and a glut can return as fast as the shortage arrived. The capital intensity is unforgiving, every process transition demands billions in reinvestment just to stand still on cost, and a company that under-invests at the wrong moment falls off the cost curve permanently. And the entire manufacturing base sits in a concentrated geography, the fabs in Japan's Iwate Prefecture and the broader East Asian supply chain, including Taiwan-linked foundry and equipment dependencies, exposing the franchise to geopolitical shocks that no operational excellence can fully hedge. The bull and the bear are, in a sense, describing the same facts, a high-fixed-cost, high-barrier oligopoly riding a demand surge, and simply disagreeing about how long the surge lasts and how disciplined the players remain when it fades.

What is not in dispute is that the separation accomplished its core purpose: it let the market see and value the flash franchise on its own terms, for better and worse, instead of burying it inside a hard-drive conglomerate. Which brings us, finally, back to where we started, and to what this whole improbable arc means.

XII. Epilogue: The AI Storage Supercycle and Final Reflections

Trace the line all the way back and it runs to a workbench in the 1970s and a layer of silicon dioxide a few atoms thick. The floating-gate EEPROM cell that Eli Harari coaxed into working at Hughes Aircraft, the tiny sealed bucket that could hold a charge for years without power, is the direct technological ancestor of every photograph stored on every phone, every file on every laptop SSD, and every model checkpoint and training dataset written to flash inside the AI clusters being built today.421 Harari was awarded the National Medal of Technology and Innovation for that lineage of work, a fitting recognition that the thing he could see in 1979, and that Intel could not yet bring itself to fund, became the physical substrate of the digital age.21 The man pitched a solid-state future decades before the market was ready, was told no by the smartest company in the industry, and built it anyway. That is the founding myth, and unusually for founding myths, it is basically true.

The deeper lesson of the SanDisk story, though, is structural rather than personal, and it is one long-term investors would do well to internalize. Some businesses are built to be independent, and forcing them into a conglomerate destroys rather than creates value. The marriage of hard drives and flash made perfect sense on a customer's purchase order and almost no sense on a capital-allocation committee, because the two businesses consume capital, reinvest, and cycle on fundamentally different rhythms. For nine years that mismatch suppressed the value of a world-class flash franchise. Pulling it back apart, the same flash business, the same Kioxia joint venture, the same engineers, unlocked tens of billions of dollars of enterprise value almost overnight, not because anything operational changed in the first instant, but because the market could finally price the asset for what it was. The spin-off did not build a better company; it revealed one.

And so the ticker that went dark in 2016 trades again, attached to a company that is somehow both one of the oldest pioneers in digital storage and one of the freshest names in the AI-infrastructure trade. SanDisk defined the formats of the digital-camera and smartphone eras, briefly overreached as a consumer brand, surgically bought its way into the enterprise, was absorbed by a giant fighting for its own survival, and then rose back out with its name, its alliance, and its purpose intact, now positioned at the center of the largest computing build-out in a generation. Whether the supercycle endures for years or gives way to the next memory winter, the survival story itself is the remarkable part: a Silicon Valley pioneer that defined an industry, died as an independent entity, and was reborn to help power the next century of computing.

References

-

SanDisk Shares Pop as S&P 500 Inclusion Becomes Effective Today — Investing.com, 2025-11-28 ↩↩↩

-

Western Digital, Sandisk begin separate trading after split — Blocks & Files, 2025-02-25 ↩

-

1991: Solid State Drive module demonstrated — Computer History Museum, The Storage Engine ↩↩

-

Flash Memory History: How CompactFlash Changed Computing — Tedium, 2017-11-23 ↩↩

-

Profile: A Virtual Company Shows It's For Real — New York Times, 1994-06-12 ↩

-

Kioxia and SanDisk joint venture production and technology announcements — Kioxia Investor Relations, 2025-03-15 ↩↩

-

Sandisk to acquire M-Systems for $1.6 billion — InfoWorld, 2006-07-30 ↩

-

SanDisk to buy Fusion-io for $1.1 billion — CNBC, 2014-06-16 ↩

-

SanDisk Acquires Flash Disk Maker Pliant Technology For $327M Plus Earn-out — TechCrunch, 2011-05-16 ↩

-

Sandisk acquires SMART Storage Systems — TweakTown, 2013-07-01 ↩

-

Western Digital to Acquire SanDisk for $19 Billion — Wall Street Journal, 2015-10-21 ↩

-

Western Digital, SanDisk and the China factor — Fortune, 2015-10-22 ↩↩↩

-

Activist Firm Elliott Pushes Western Digital to Split Its Businesses — U.S. News / Reuters, 2022-05-03 ↩↩↩

-

Western Digital to Spin Off Flash Memory Business — Reuters, 2023-10-30 ↩

-

Western Digital to Split Into Two Public Companies — Bloomberg, 2023-10-30 ↩

-

Sandisk Reports Fiscal First Quarter 2026 Financial Results — Sandisk Investor Relations, 2025-11-06 ↩↩

-

Micron and Competitors Announce NAND Price Increases — Bloomberg, 2025-03-10 ↩↩

-

Eli Harari — National Medal of Technology and Innovation, National Science and Technology Medals Foundation, 2014-11-20 ↩↩

-

SanDisk's second act: An AI boom, a $160 billion valuation, and a deep Israeli thread — Calcalist (CTech) ↩

-

SanDisk Signs Definitive Agreement to Acquire Fusion-io — Business Wire, 2014-06-16 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube